In partnership with

Weekly Newsletter

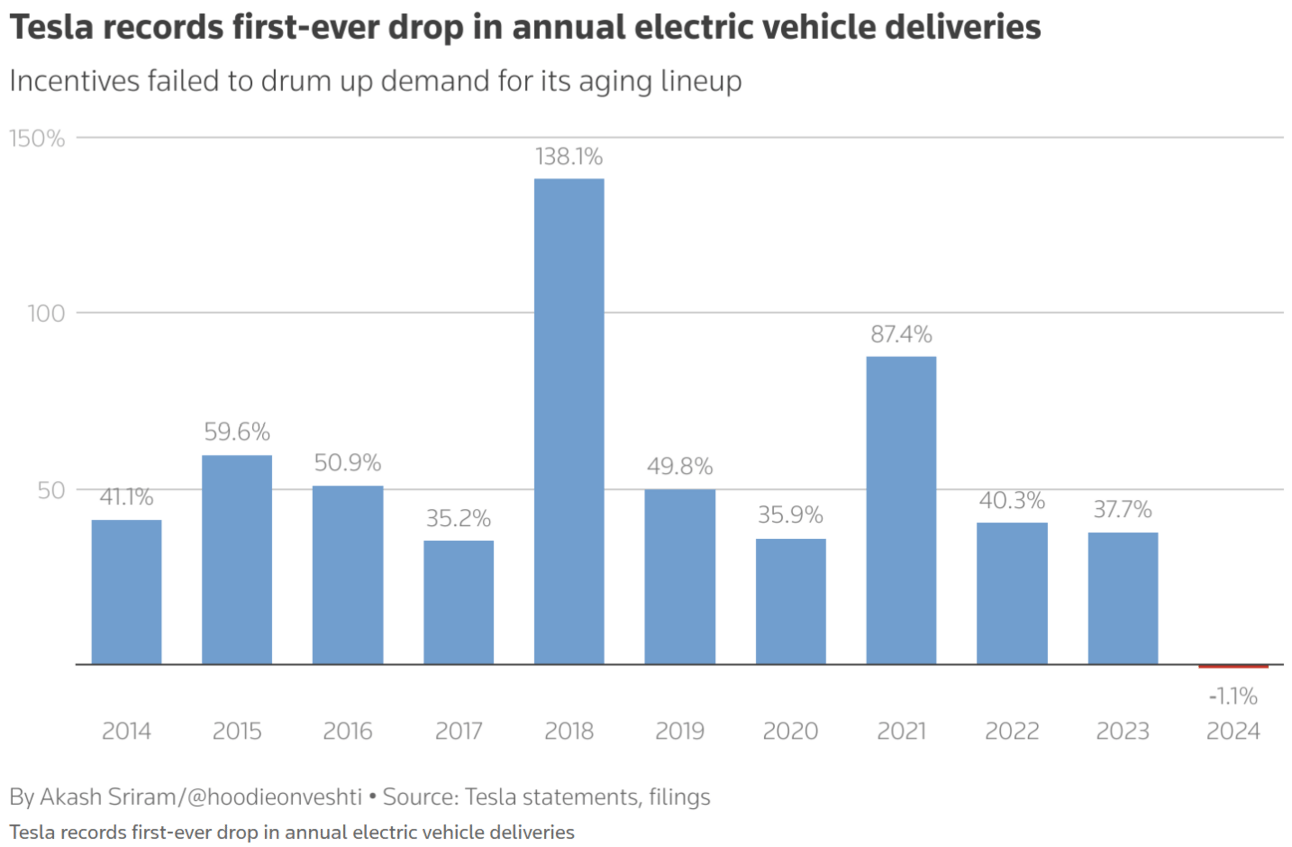

Tesla Miss Annual Delivery Forecast For The First Time

Bitcoin’s 16th Anniversary

Better Than Expected Unemployment Claims Data

Positive News On Manufacturing

Dollar Soares

New Features On My Blog Website

QUOTE OF THE WEEK:

“I think we are seeing it's a stable situation, that the labor market is resilient, that the labor market has rebalanced. We want to keep it at that level. That's what we want. And we feel it's the same resilience; the unemployment rate is not increasing rapidly like it has increased in prior recessions.” Fed Governor Adriana Kugler

KEY US ECONOMIC EVENTS NEXT WEEK:

MARKET CLOSE:

Good Afternoon. Key indices ended the week in the Red by ~0.50%. Markets rallied on Friday after better-than-expected unemployment claims data helped reduce the week's drop. Significant highlights for the week are:

The unemployment claims number shows that the labor market is still doing fine.

Sixteen years ago, on Jan 3rd, 2009, Satoshi Nakamoto first mined Bitcoin for the first time. Since its launch, Bitcoin has appreciated by ~2,000,000%.

Tesla missed the annual delivery forecast (by a small margin) for the first time. At the same time, Ford and GM reported the best annual sales since 2019.

The dollar rallied after Thursday’s good unemployment claims data.

For the week:

The S&P 500 is down 0.50%, the Nasdaq is down 0.50%, and the Dow 30 is down 0.60%.

CNN's Fear & Greed Index now stands at 32 (Fear) out of 100, down 2 points from last week. Details here

The top five trending stocks on Reddit are VOO, Nvidia, SPY, Microstrategy, and Tesla . Read More

Here is a summary of this week’s key economic releases:

US initial unemployment claims ended 2024 at an eight-month low, underscoring the labor market's resilience amid minimal job cuts. Continuing applications dropped by 9,000 to 211,000 for the week ending Dec. 28, beating most Bloomberg estimates, while continuing claims fell to a three-month low of 1.84 million for the week ending Dec. 21, per Labor Department data.

The December US ISM Manufacturing Index exceeded expectations, climbing to 49.3 from November’s 48.4, against a consensus of 48.2. The uptick was primarily driven by a rebound in the production component to 50.3 from 46.8, likely supported by the resumption of work by Boeing employees after a strike, marking the first reading above 50 since May.

Target Rate Probabilities for Jan 29th FOMC Meeting:

CME Fed Watch: * Data as of 4 Jan 2025 10:11:17 CT

FRONT PAGES:

Credit Delinquencies Sore: US credit card loan defaults have reached their highest since the 2008 financial crisis, reflecting the strain on lower-income consumers amid prolonged inflationary pressures. Lenders charged off $46 billion in seriously delinquent credit card loans in the first nine months of 2024—a 50% surge compared to the same period last year and the highest figure in 14 years, according to BankRegData. These write-offs, a key indicator of severe loan distress, signal growing concerns over borrowers' ability to repay debts. Read

Tesla Miss Delivery Forecast: Tesla reported global deliveries of 495,930 vehicles for the quarter, missing Bloomberg's analyst estimate of 510,400. However, this marks an increase from the 463,000 vehicles delivered in the previous quarter and the 484,500 delivered in the same period last year. For 2024, Tesla's total deliveries reached 1.78 million vehicles, falling short of the 1.8 million analyst estimate and slightly below the 1.8 million delivered in 2023. Read

Source: Yahoo Finance

GM and FORD Beat Deliveries: On Friday, General Motors and Ford Motor reported their most substantial annual U.S. new vehicle sales since 2019. Read

Hindenburg Shorts Carvana: Hindenburg Research accused Carvana Co. of impropriety, claiming the auto retailer's subprime loan portfolio poses significant risks and that its growth trajectory is unsustainable. Read

Mortgage Rates Up: US mortgage rates edged closer to 7%, adding pressure on prospective homebuyers. The 30-year average rose to 6.91% on Jan. 2, up from 6.85% the prior week, per Freddie Mac. Meanwhile, the Mortgage Bankers Association reported a rise to 6.97%, marking a near six-month peak as of Dec. 27. Read

Dollar Strengthens: The dollar soared to a two-year high against the euro and an eight-month high against the sterling on Thursday, driven by strong U.S. jobs data that reinforced investor confidence in the resilience of the world's largest economy. Read

Source: FT, Bloomberg

EARNINGS UPDATE:

No significant earnings were reported this week. I covered a detailed analysis of this earnings season on Dec 15th, when more than 99% of S&P 500 companies had reported earnings.

EARNINGS PREVIEW:

Date | Symbol | Name | Time |

6-Jan | BHP | Bhp Billiton Ltd ADR | -- |

7-Jan | RPM | RPM International Inc | Before Open |

8-Jan | ACI | Albertsons Companies Inc Cl A | Before Open |

8-Jan | JEF | Jefferies Financial Group Inc | After Close |

9-Jan | INFY | Infosys Ltd ADR | -- |

9-Jan | STZ | Constellation Brands Inc | Before Open |

10-Jan | BAC | Bank of America Corp | -- |

10-Jan | BLK | Blackrock Inc | -- |

10-Jan | DAL | Delta Air Lines Inc | Before Open |

10-Jan | WFC | Wells Fargo & Company | -- |

10-Jan | WIT | Wipro Ltd ADR | -- |

CURATED INSIGHTS:

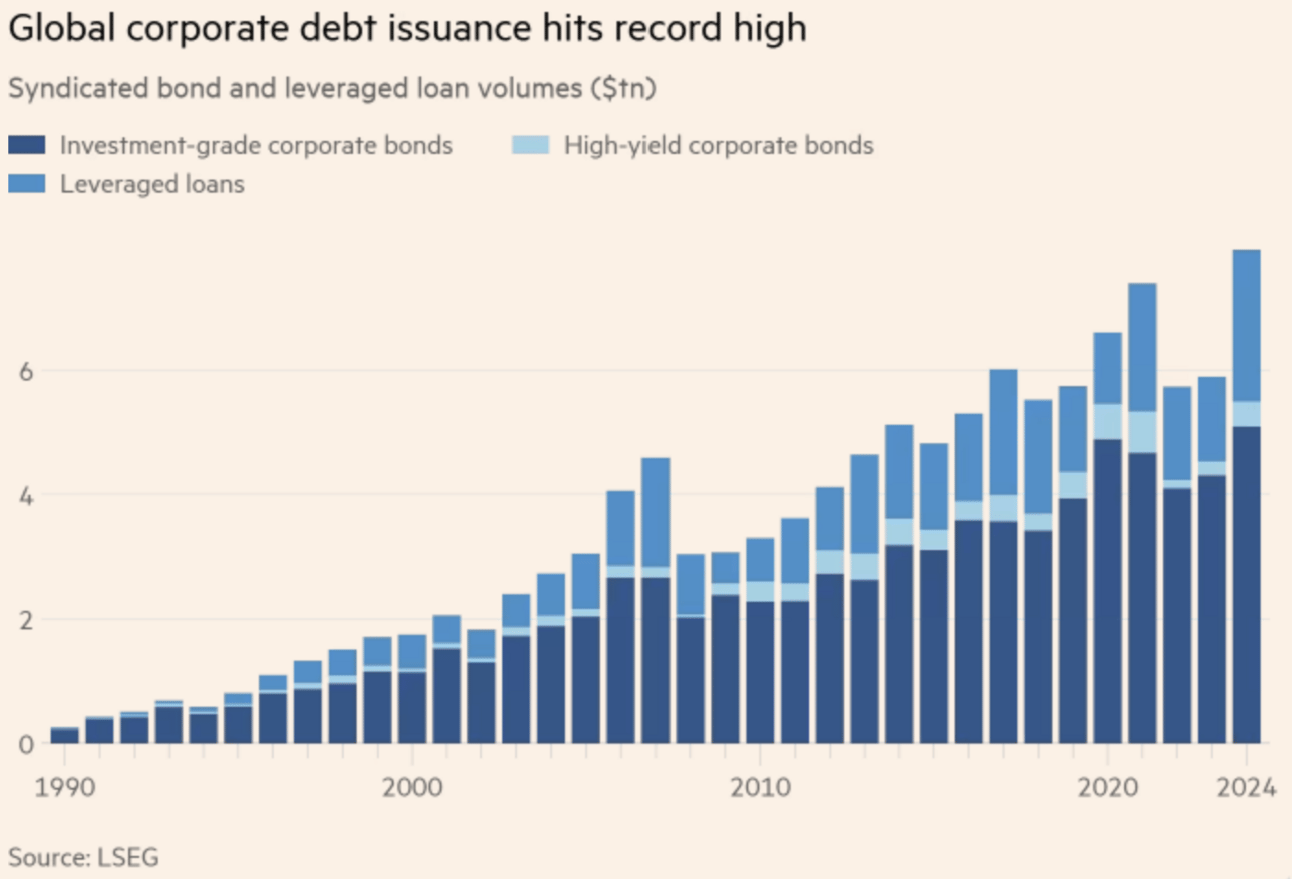

Global Corporate Debt Issuances Hit Record: The Financial Times reported that Global corporate debt issuances jumped to ~$8 Trillion from under $6 Trillion in 2023. We note below that there is a decent rise in all debt issuances, including investment-grade corporate debt. Companies such as Home Depot and Abbvie raised significant amounts via debt sales. If we think logically, the investment-grade companies raised ~1 Trillion more than in 2023. The yields on investment-grade corporate debt are higher now, i.e., 5.4%, due to higher treasury yields. Considering that good companies raise a trillion dollars extra at a higher rate, these well-managed profit-making corporations expect good times ahead or have confidence that they can put the new capital to better use and generate returns than they paid. There is a sharp rise in high-yield debt issuances, but I would prefer to focus on what investment-grade corporations do to infer general mood as they have better management and track records.

New Features On My Blog Website: I wanted to share a few new features that have been added to my blog website. I am working on refining them further, and there may be some changes to fix minor issues. These features will be super helpful for anyone interested in financial markets and general educational topics, and they will provide all essential curated news media and feeds in one place.

News Media Tab: This tab contains all the critical financial news/analysis-related videos. The videos are divided into four categories - 1. Financial News. 2. Influences, 3. Institutions and Agencies, and 4. Podcasts. The main tab shows 15 videos of each category, and as you scroll down, the next category will show up after 15 videos. You can select the category and channel from the drop-down to view more than 15 videos for that particular category. You can even select a specific channel you are interested in.

News Feed Tab: This tab is similar to the news media tab but just for news articles. I added similar categories for further selection.

Top Clips: I will develop this tab over time. I am going to share my favorite educational and motivational videos here.

VIDEO’s OF THE WEEK:

AI's NEXT Magnificent Seven

The Original Magnificent Seven Produced 16,894% Average Returns Over 20 Years. $1,000 in each turned into $1.18 million! But the Man Who Called Nvidia at $1.10 Says "AI's Next Magnificent Seven Could Do It Even Faster." He says $1,000 in these seven stocks could turn into $1 million+ in less than six years. The first company on his list just signed a MAJOR deal with Apple, and its tech is going to be included in the iPhone and iMac until 2040! See his breakdown of the seven stocks you should own.

Please Share This Newsletter With Your Friends.

Also, check my blog here.

This newsletter's content is for informational and educational purposes only and should not be considered trading or investment recommendations. All the opinions in this newsletter are personal and do not belong to any organization.