Weekly Newsletter

🧭 Key Points from FOMC Press Conference

📈 Still Not The Perfect Time for Small Caps

🏦 OCC Approves Digital Asset Banks

🚀 SpaceX Plans Largest IPO in 2026

💻 Broadcom’s ASIC Flywheel Drives Strong Earnings

QUOTE OF THE WEEK:

“In the larger scheme of things, in our view, earnings are very strong, the monetary and fiscal tailwinds are very much there, and we think the capital markets have further to go, and all that drives the upside in 2026.” - Julian Emanuel, Senior Managing Director, Evercore ISI.

KEY US ECONOMIC EVENTS NEXT WEEK:

MARKET CLOSE:

CNBC EOD 12/23

WEEKLY MARKET WRAP:

Good Afternoon. It's a down week for growth stocks as AI bubble fears continue to weigh on markets. As expected, the FOMC delivered a 25-bps rate cut, but also delivered more than just the rate cut. More details on the same below.

Below are the key things to note this week:The FOMC Decisions:

Anything to keep ample reserves: In addition to cut rates, which were on the expected lines, the Fed chair made a couple of announcements in the FOCM press conference - 1. The Fed will begin with $40 billion in purchases this month and intends to taper the pace gradually sometime next year. The Fed is taking this action as a precaution to avoid funding stress in the overnight money markets. 2. The Fed chair also announced that it is removing the $500 billion borrowing limit for the Secured Repurchase Facility (SRF) which banks may use during the stress situation to borrow against the eligible collateral.

Both of these preventive steps demonstrate the Fed’s commitment to maintaining ample reserves in the system and to doing whatever it takes. This indicates that the Fed has learned a great deal from past stress events and does not want to repeat them. This is very good for the markets, as it materially reduces the risk of banking stress events observed in March 2023 or Sept. 2019.

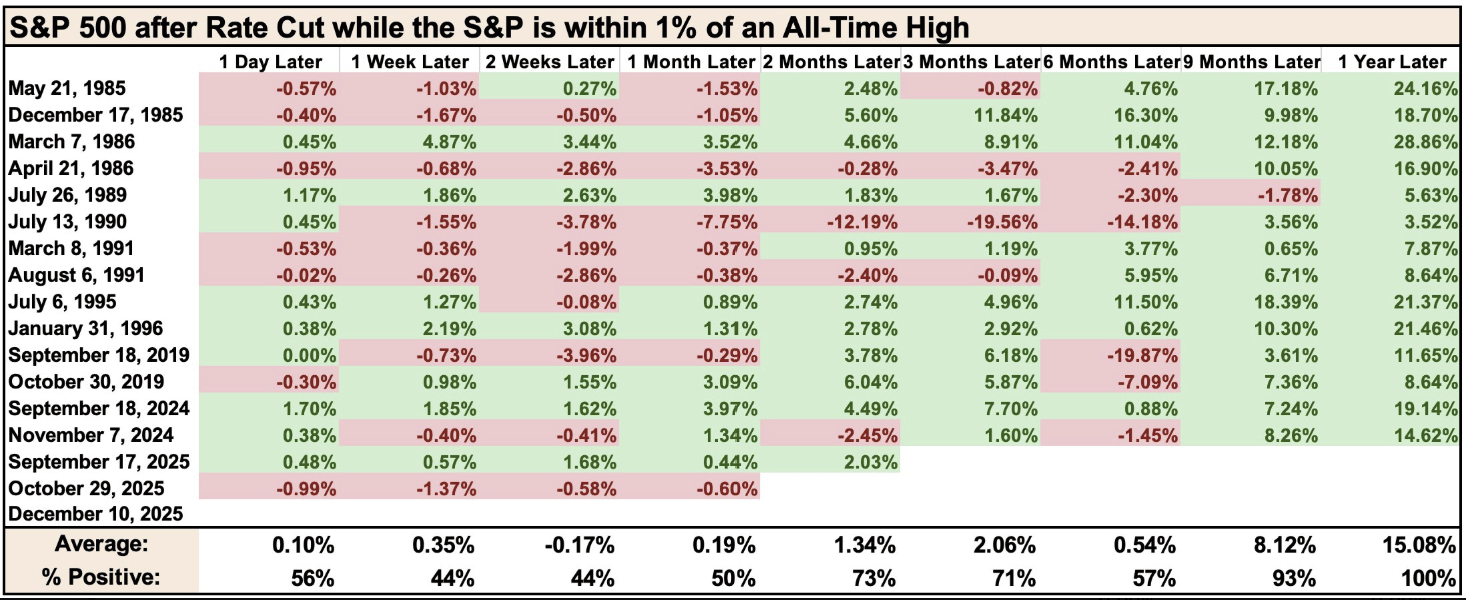

The Fed has cut rates when the S&P is near an all-time high. Below is the S&P 500's historical performance in this scenario. The index is up 100% of the time after one year. Historical performance is not guaranteed, but this is still an impressive datapoint:

Source: Subutrade.com

For the week:

The S&P 500 is down 0.63%, the Nasdaq is down 1.62%, and the Dow 30 is up 1.05%.

Barchart

CNN's Fear & Greed Index now stands at 42(Fear) out of 100, up 2 points from last week. Details here

The top five trending stocks on Reddit are SPY, Broadcom, Nvidia, Tesla, and Oracle. Read More

Liquidity:

Banking Reserves + ON RRP: Banking reserves remain at approximately $2.9 trillion. ON RRP balance remains immaterial.

Standing Repo Facility (SRF): The SRF balance as of Dec 12 is almost zero.

Here is a summary of this week’s key economic releases:

Target Rate Probabilities for January 26th FOMC Meeting:

CME FedWatch

CURATED INSIGHTS & ANALYSIS:

Key points from the FOMC press conference:

The Fed cut rates by 25 bps to 3½–3¾%, citing rising downside risks to employment even as inflation remains above target.

Inflation has eased significantly from 2022 highs but remains elevated at 2.8% PCE; recent firmness reflects tariff-driven goods inflation, while services inflation continues to cool.

The Fed views tariff inflation as essentially a one-time price-level shift, with goods inflation expected to peak around Q1 2026 if no new tariffs are introduced.

Labor market conditions are cooling: unemployment rose to 4.4%, hiring slowed sharply, and the Fed believes payroll data overstate job growth by roughly 60k per month.

Powell emphasized that downside risks to employment have increased, while inflation and labor risks are now elevated simultaneously, creating a difficult policy trade-off.

Policy rates are now within a broad range of estimates of neutral, positioning the Fed to pause and reassess incoming data on a meeting-by-meeting basis.

The growth outlook was revised higher, supported by resilient consumer spending, fiscal support, and sustained AI-related investment.

Productivity growth appears structurally higher, potentially enabling stronger growth without proportional job gains; AI may be contributing, though the impact remains uncertain.

The Fed announced $40bn per month in short-term Treasury purchases to maintain ample reserves amid rising money-market pressures.

Standing Repo Facility limits were removed, reinforcing the Fed’s rate-control framework in an ample-reserves regime.

Committee divisions widened as members debated how to balance persistent inflation risks against a softening labor market.

Powell stressed that policy is not on a preset path and that upcoming decisions will depend on data distorted by the effects of the recent government shutdown.

Broadcom’s ASIC Flywheel:

Custom AI accelerators (ASICs/XPUs) are now the primary growth driver for Broadcom, with management disclosing a ~$73B secured AI backlog over the next ~18 months, of which roughly ~$ 50 B is tied to XPUs and system-level deployments rather than networking alone.

XPUs are evolving from standalone chips to full-system (rack) sales, enabling Broadcom to capture more value per deployment as hyperscalers scale their training and inference infrastructure.

ASIC demand is proving durable and repeatable, with large follow-on orders and a growing customer base, reinforcing that custom silicon is a multi-year strategic commitment rather than a one-off experiment.

The broader AI implication is efficiency at scale: ASICs deliver materially better performance per watt and lower cost per token than general-purpose GPUs, especially as inference and reasoning workloads expand.

AI compute is fragmenting by workload, with customers designing multiple accelerator variants for training, inference, and reasoning—something best achieved through hardware specialization rather than software alone.

While system sales and memory pass-through dilute gross margins, Broadcom expects operating income dollars to keep rising on volume and operating leverage, underscoring the quality of AI-driven growth.

Small Caps are still not the best bet:

When the Fed began rate cuts last year, the hope was that they would help small caps outperform, as these companies rely on floating-rate debt. Rate cuts were also expected to spur economic activity, benefiting these businesses. However, small caps continue to underperform, and investors are better off betting on high-quality large-cap US companies with strong earnings. The earnings comparison for the last two quarters I provided shows a material improvement in small-cap performance. However, sticky inflation from tariffs affects small companies more than larger peers with bellwether balance sheets, and this appears to continue to dampen small-cap performance until the one-time tariff impact on inflation fades in the second half of 2026.

Apollo

FRONT PAGES:

The Fed re-appoints presidents: The Federal Reserve’s Board of Governors voted unanimously to reappoint 11 Reserve Bank presidents for new five-year terms starting March 1, 2026, the central bank said Thursday. Reserve Bank presidents are selected by their local boards—typically composed of business and nonprofit leaders—but must obtain approval from the Washington-based governors, with all 12 presidencies reviewed simultaneously every five years. Read

The Fed addresses funding market pressure: The Federal Reserve signaled a renewed balance-sheet expansion by purchasing short-term Treasury securities to preempt stress in overnight funding markets critical to financial stability. The Fed will begin with $40 billion in purchases this month and intends to taper the pace gradually sometime next year. Read

SpaceX IPO: SpaceX is advancing an insider share sale that values the rocket and satellite company at roughly $800 billion, positioning it for what could be the largest initial public offering in history. Read

OCC approves crypto banks: The Office of the Comptroller of the Currency conditionally approved five digital-asset firms, including Circle, Ripple, and Paxos, for de novo national trust bank charters, the regulator announced Friday. Read

EARNINGS UPDATE:

Adobe Beat: FQ4 non-GAAP EPS of $5.50 beat expectations by $0.10. Revenue of $6.19B, up 10.3% Y/Y, exceeded estimates by $80M. The company surpassed its FY2025 Digital Media ending ARR target and guided to over 10% growth in FY2026 total ending ARR. FY2025 operating cash flow reached a record level, exceeding $10B.

Oracle Mixed: For the period ending Nov. 30, Oracle reported adjusted EPS of $2.26 as revenue rose 14% Y/Y to $16.06B, versus expectations of $1.64 on $16.19B. Cloud revenue totaled $8.0B (+34% Y/Y), slightly below estimates. Infrastructure revenue surged 66% (cc) to $4.1B, applications rose 11% to $3.9B, Fusion Cloud ERP grew 18% to $1.1B, and remaining performance obligations jumped 438% to $523B.

Broadcom Beat: Q4 non-GAAP EPS came in at $1.95, exceeding expectations by $0.08. Revenue reached $18.02B, up 28.2% Y/Y, beating estimates by $560M. Adjusted EBITDA totaled $12.2B, representing 68% of revenue. Operating cash flow was $7.7B; after $237M in capex, free cash flow was $7.5B, or 41% of revenue. The quarterly dividend was raised 10% to $0.65 per share.

Costco Beat: Costco reported November net sales of $23.64 billion for the four weeks ended November 30, up 8.1% year over year. First-quarter net sales for the twelve weeks ended November 23 totaled $65.98 billion, an 8.2% increase. Net sales for the first thirteen weeks reached $71.97 billion, also up 8.2% year over year.

EARNINGS PREVIEW:

Date | Symbol | Name | Time |

17-Dec | MU | Micron Technology | After Close |

18-Dec | ACN | Accenture Plc | Before Open |

18-Dec | CTAS | Cintas Corp | Before Open |

18-Dec | NKE | Nike Inc | After Close |

VIDEO’s OF THE WEEK:

Please Share This Newsletter With Your Friends.

Also, check my blog here.

This newsletter's content is for informational and educational purposes only and should not be considered trading or investment recommendations. All the opinions in this newsletter are personal and do not belong to any organization.