Weekly Newsletter

📊 Valuations of Major Equity Indices

🏦 Key Takeaways from Bank Results

🎬 Bellwether Netflix

🛍️ Retailers are Cutting Discounts

🌍 Tariff Headache for Major Central Banks

⚠️ Why Leveraged ETFs Are Only For Traders

QUOTE OF THE WEEK:

“People tell us, money can’t buy you happiness, and don’t worry about money. I truly believe that before you become a philosopher, before you start saying things like money can’t buy you happiness, you can become a philosopher after you become rich. But you can’t be a philosopher before that.” - Shahrukh Khan, Bollywood Actor.

KEY US ECONOMIC EVENTS NEXT WEEK:

MARKET CLOSE:

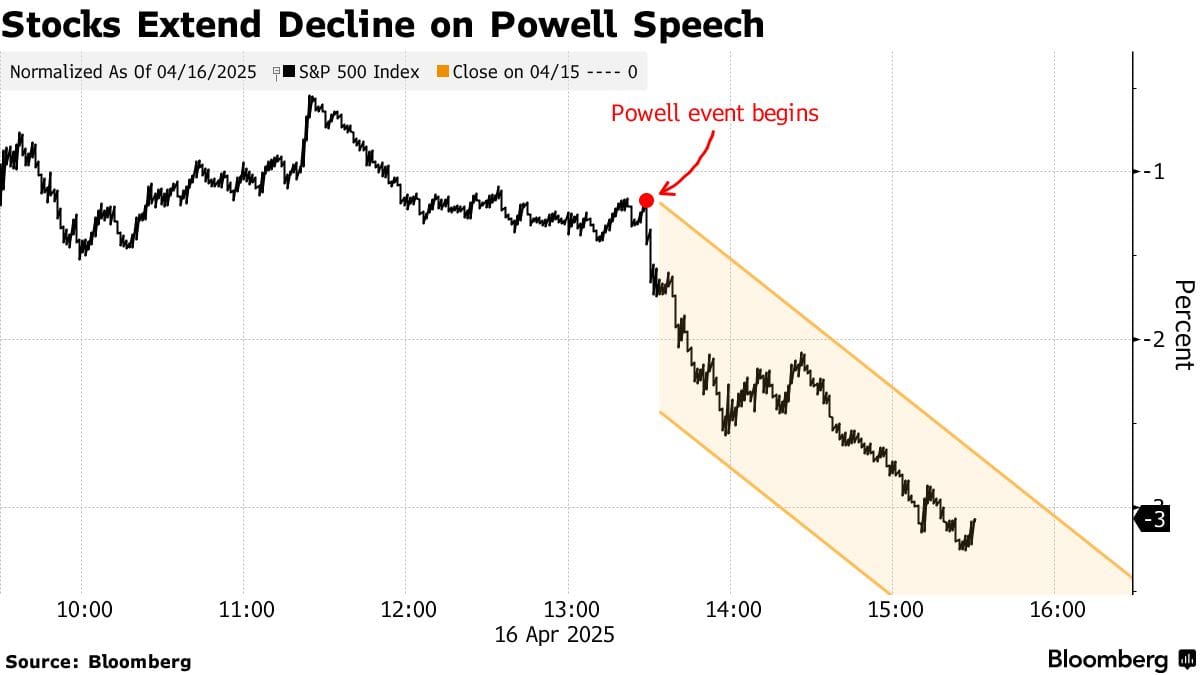

Good Afternoon. All major indices closed in the Red for the week. Fed Chair Jerome Powell’s speech was the main reason stocks gave away all their gains on Wednesday, which weighed heavily on the week’s performance. After Powell reaffirmed the Fed’s aggressive stance on inflation in his speech, markets turned volatile. In addition, the chip stocks sell off after Nvidia and AMD both announced earnings were hit due to China restrictions, and poor results from UnitedHealthcare put pressure on the markets overall.

IMF Sees Global Slowdown, No Recession:

IMF chief warned of a global slowdown driven by the US-led trade “reboot,” citing rising protectionism under Trump’s tariff threats as a key drag on productivity and growth. Recession is not in the forecast. The IMF is scheduled to release its World Economic Outlook on Tuesday, which I will cover in next week’s newsletter.Bellwether Netflix:

Netflix reported another strong quarter this week. With the cheapest plan starting at $7.99, Netflix is well-positioned to serve its largest customer base during the potential downturn. On the earnings call, the company mentioned that they haven’t noticed any significant changes in customer behavior due to the current uncertainty. Rather, the company did not even use the word “Tariff” in its prepared remarks. Netflix is uniquely positioned and a great business, which makes this one of my top picks for the long term.Hard Data Still Strong:

Hard macro data is still strong. Both retail sales and unemployment claims came in better than expected this week. Consumers have rushed to make purchases before the tariffs kick in, and this is seen in the retail sales numbers.Powell was Right:

In the last FOMC press conference, Jerome Powell referenced how inflation increased during the last tariff escalation for all products, not just those affected by the tariffs. For example, he mentioned that washers were tariffed, so the washer prices were expected to go up. However, retailers took the opportunity to raise dryer prices and take advantage of the sentiment. I had firsthand experience of retailers using tariffs as an excuse for not giving discounts. Yesterday I went to purchase a kids’ bike for my son. Last time when I purchased two adult bikes of a reputed brand, I got a 15%-20% discount without even me proactively asking. This time, though, the young boy at the bike shop explained how tariffs are making it difficult to give any discount. Finally, he gave me a 5% discount for my son’s 20” bike priced over $600. This shows that the retailers will use tariffs as an excuse to cut down on discounts, at least if they don’t raise item prices.For the week:

The S&P 500 is down 1.50%, the Nasdaq is down 0.62%, and the Dow 30 is down 1.14%.

Source: Barchart

CNN's Fear & Greed Index now stands at 21 (Extreme Fear) out of 100, up 8 points from last week. Details here

The top five trending stocks on Reddit are SPY, Tesla, EU, Nvidia, and UnitedHealth. Read More

Here is a summary of this week’s key economic releases:

Target Rate Probabilities for May 7th FOMC Meeting:

CME FedWatch

CURATED INSIGHTS & ANALYSIS:

Dangers of Leveraged ETFs:

Financial Times recently reported that investors lost more than $25 billion in leveraged ETFs after the April 2nd Tariff sell-off. I wanted to highlight the danger of holding leveraged ETFs for the long term. These securities are best for trading and take advantage of market volatility; however, considering the risk-reward, holding them for the long term doesn’t make sense.

The table below is self-explanatory. It shows that any major market drawdown can wipe out all the gains from these leveraged bets. Even though the five-year returns beat the underlying QQQ returns, they are still far less than the 3X risk investors are taking, and these can also be wiped out in a short time if markets fall slightly from current levels. In short, leveraged ETFs are only for Traders.

Source: Barchart, Primal Thesis

The market’s obsession with leveraged ETFs is not dying down, and hence, retail investors must understand the risk associated with these securities.

Source: Bloomberg

Key Takeaways from Bank Earnings:

Macro Indicators:Consumer spending remained strong:

Amex U.S. card spending rose 7% YoY; Millennials and Gen Z up 14%.

BofA reported $1.1T in Q1 consumer payments, up 4% YoY.

Commercial credit demand mixed:

JPMorgan and BofA saw loan growth (+2–4% YoY); Wells Fargo reported a 2% YoY decline.

Deposit levels are broadly stable:

Deposits up slightly YoY at JPM (+2%) and BofA (+3%), but flat or down at others like Wells Fargo (-2%).

Rising credit costs suggest early signs of consumer strain:

Citi card charge-offs rose to 4.7%; JPM and BofA also reported elevated provisions.

Investment activity and capital markets rebounded:

GS, JPM, Citi, and MS reported stronger trading and investment banking revenues, aided by higher market volatility.

Banking System Health:

Capital remains robust across all major banks:

CET1 ratios well above regulatory minimums: JPM (15.4%), Citi (13.4%), BofA (11.8%), WFC (11.1%), BNY (11.5%).

Liquidity metrics are solid:

LCRs above 110% across the board: JPM (113%), WFC (125%), BNY (116%).

Profitability remains strong:

JPM (ROE 18%, ROTCE 21%), GS (ROE 16.9%), Citi (RoTCE 9.1%), BofA (ROE 10.4%).

Positive operating leverage and cost discipline across most banks, especially Citi and GS.

Reserves are stable or increasing slightly, reflecting a cautious macro outlook. There are no signs of systemic credit stress.

Valuation Discount of All Major Indices:

The graph below shows the current valuation of all major indices compared to their 10-year average. The leading S&P 500 index still trades at its historic average.

Source: Factset, Edward Jones

Central Banks’ Dilemma:

Reuters published an analysis this week of the tariff impact on all major economies and how the uncertainty makes the job of central banks difficult.

Source: LSEG, Reuters

Source: Reuters, Primal Thesis

FRONT PAGES:

Possible China Trade Deal: Trump said he was hesitant to escalate tariffs on China, warning it could stall trade. He claimed Beijing had made repeated overtures to strike a deal. Read

Trump vs. Powell: White House adviser Kevin Hassett said Trump and his team are exploring the option of firing Fed Chair Jerome Powell. This action would carry profound implications for central bank independence and global markets. Read

Discover Cap One Merger: The Fed and OCC have formally cleared Capital One’s $35.3B all-stock acquisition of Discover. Read

Bad News for Google: Google’s antitrust troubles continue to grow as it pivots to an AI-driven future. A federal judge ruled it held illegal monopolies in online ads, marking its second major antitrust setback in less than a year. Read

Nvidia Takes A Hit: Nvidia will take a quarterly charge linked to halted H20 chip exports, after the US imposed new licensing rules on shipments to China and select nations. Read

Trump’s Approval Ratings Fall: President Trump is seeing his lowest economic approval ratings, driven by rising discontent over tariffs, inflation, and fiscal policy, per the latest CNBC All-America Economic Survey. Read

EARNINGS UPDATE:

Goldman Sachs Beat: Goldman Sachs beat Q1 estimates as equities trading surged, lifting profit 15% to $4.74B ($14.12/share) on 6% revenue growth. Trading gains offset a slight dip in asset and wealth management revenue. Read

Bank of America Beat: Bank of America beat Q1 estimates as profit rose 11% to $7.4B and revenue grew 5.9% to $27.5B, driven by stronger net interest income and trading. NII hit $14.6B, topping forecasts. Read

Charles Schwab Beat: Charles Schwab reported a 37% jump in Q1 profit, driven by strong trading and asset management. Market volatility from tariff-related uncertainty led investors to reshuffle portfolios, boosting Schwab’s wealth and trading segments. Read

American Express Beat: American Express beat Q1 profit estimates as affluent customers kept spending on travel and entertainment. It reaffirmed its 2025 outlook even as others pulled guidance amid trade policy uncertainty. Read

Netflix Beat: Netflix reaffirmed its revenue outlook and expressed confidence in navigating Trump’s unpredictable tariff moves. Co-CEO Greg Peters noted no major change in consumer behavior, easing concerns about potential pullbacks in streaming spend. Read

United Healthcare Miss: UnitedHealth shares tumbled 22% after it cut its annual profit forecast, citing a surge in medical service demand from older patients that was “far above” expectations. Read

EARNINGS PREVIEW:

Date | Symbol | Name | Time |

22-Apr | DHR | Danaher Corp | Before Open |

22-Apr | GE | GE Aerospace | Before Open |

22-Apr | ISRG | Intuitive Surg Inc | After Close |

22-Apr | RTX | Rtx Corp | Before Open |

22-Apr | TSLA | Tesla Inc | After Close |

22-Apr | VZ | Verizon Communications Inc | Before Open |

23-Apr | IBM | International Business Machines | After Close |

23-Apr | PM | Philip Morris International Inc | Before Open |

24-Apr | GOOG | Alphabet | After Close |

24-Apr | PG | Procter & Gamble Company | Before Open |

24-Apr | TMUS | T-Mobile US | After Close |

25-Apr | ABBV | Abbvie Inc | Before Open |

29-Apr | AMZN | Amazon.com Inc | -- |

29-Apr | KO | Coca-Cola Company | Before Open |

29-Apr | V | Visa Inc | After Close |

VIDEO’s OF THE WEEK:

Please Share This Newsletter With Your Friends.

Also, check my blog here.

This newsletter's content is for informational and educational purposes only and should not be considered trading or investment recommendations. All the opinions in this newsletter are personal and do not belong to any organization.