In partnership with

Weekly Newsletter

Bitcoin Cross $100k Milestone

Another Good Week Propel Markets To Record Levels

Factors Influencing Markets

Improved Manufacturing Outlook

In-Line Payroll Data

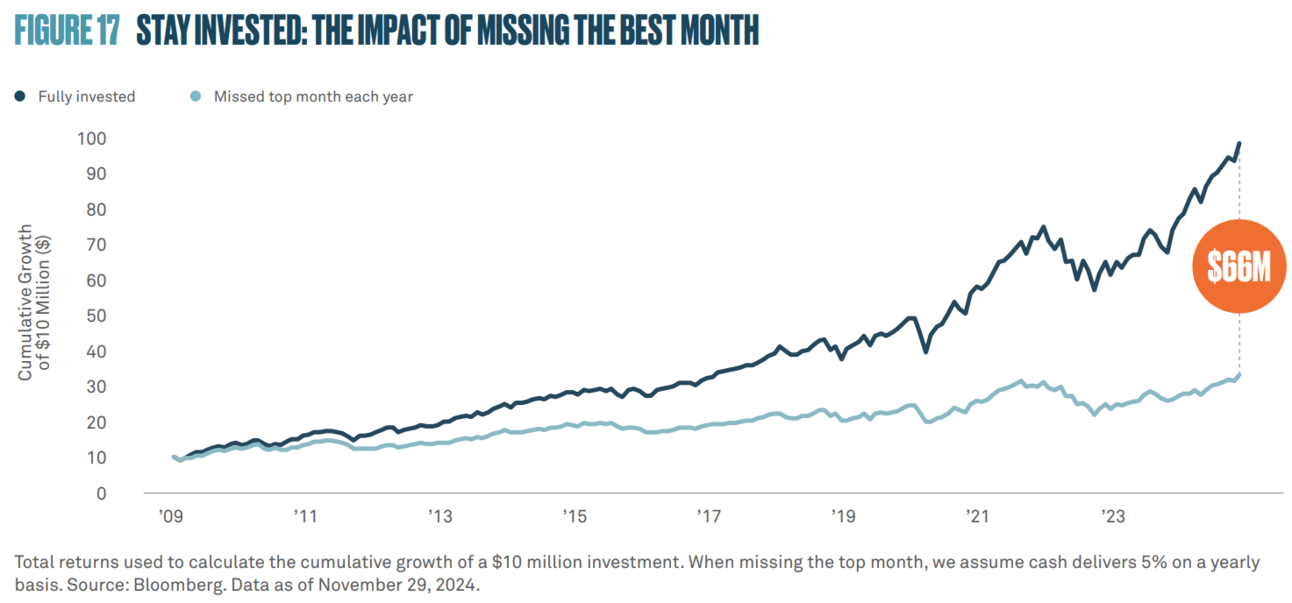

Importance Of Staying Invested

Key Insights From The Financial Stability Report

QUOTE OF THE WEEK:

“It's not that I don't believe in fighting climate change. We can talk about that being the existential problem at the moment. I just don't think ESG works. I've described it as an empty acronym, born in sanctimony, nurtured with hypocrisy, and sold with sop history. Basically, you know, when you see the way it's been applied, and you look at the results you get for all the money that's been spent, you say, Why did we do this? What is it exactly we've accomplished after 15 years of ESG?” - Aswath Damodaran, Professor - New York University.

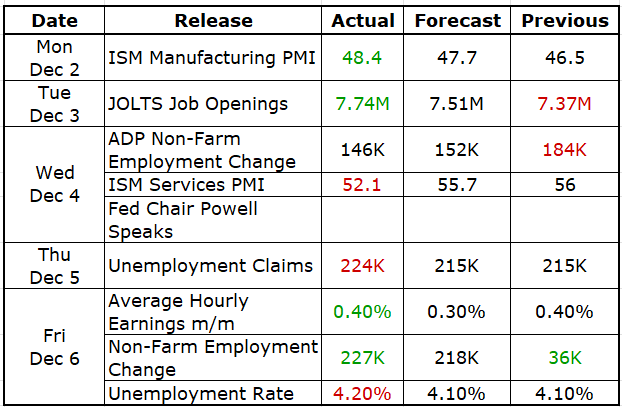

KEY US ECONOMIC EVENTS NEXT WEEK:

MARKET CLOSE:

Good Afternoon. The S&P 500 and Nasdaq Composite reached new record highs on Friday, buoyed by November jobs data that modestly exceeded expectations. The labor report struck a balanced tone—strong enough to signal economic stability but not overly robust enough to discourage the Fed from cutting rates in the next meeting. CME Group’s Fed funds futures now suggest an 85% probability of another rate cut in two weeks. It appears to be euphoric for the short-term markets as Bitcoin crossed the $100k milestone this week, a roaring kitty tweet added action in meme stocks, and VIX is sitting at very low levels around ~12.7.

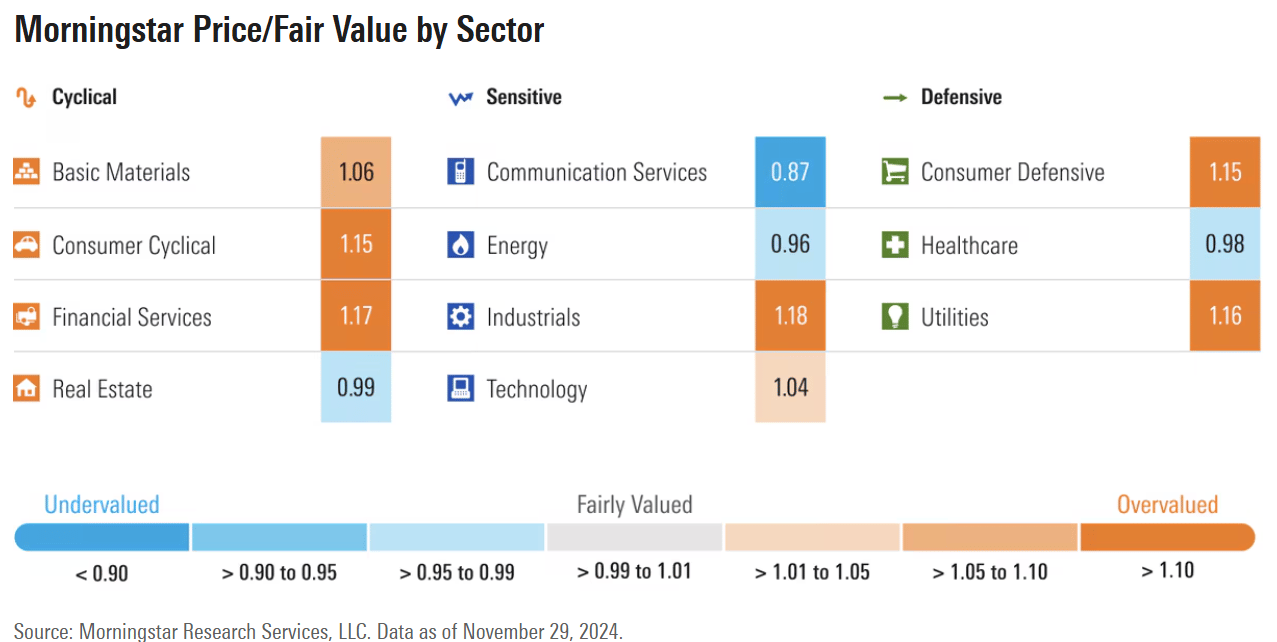

A few key points to note:Tech stocks keep rising, with the Nasdaq recording 3.34% weekly gains. Tech stocks may look overvalued if we consider this year's gains; however, robust earnings growth justifies and supports most of these gains. As per the Morningstar fair value estimates, Technology is not the most overvalued sector, even after substantial gains this year. So I won’t be surprised if the likes of Mag 7’s keep going up and close the year even at higher levels from here -

Small Caps and Value stocks are undervalued and are expected to do better with the rate-cutting cycle.

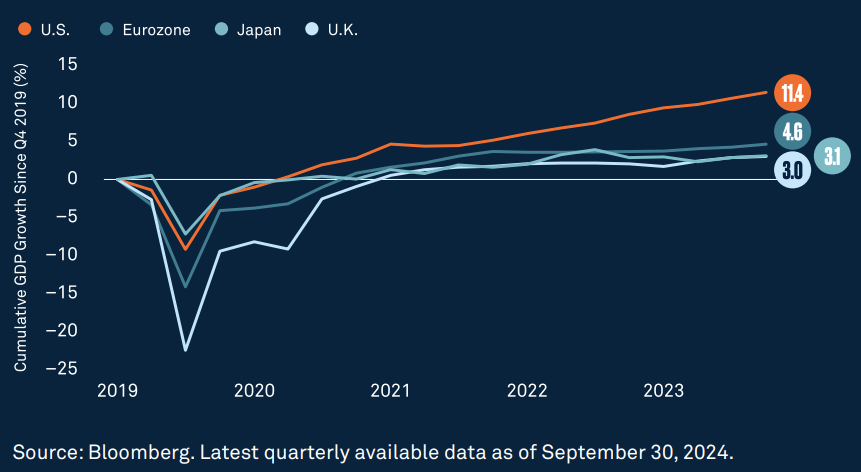

In general, the rest of the world is not doing good, so the US markets are the only option for the money to flow. China continues facing issues, and India’s recent GDP numbers were underwhelming.

Source: Bloomberg

Synopsys results this week show the potential effects of trade restrictions with China and the Trump administration are not even in place yet. So companies with significant Chinese exposure may have issues due to expected tariffs/trade war.

So, in summary,The rise in Tech stocks is justified

Other parts of the market are fairly valued or undervalued

The economy is doing well, with inflation and labor market conditions in balance.

The Fed is expected to cut rates one more time this year and maybe three more times next year.

The rest of the world is not doing great and

The Trump administration is expected to be pro-market, except for companies with significant exposure in China.

All this points to the stock market's continued good performance for the medium term.

Since 1928, December has given positive returns ~74%+ times higher than any other month. So even if no one can predict the short term, history points to a positive month. Bullish sentiments are still powerful.

Source: Bloomberg

For the week:

The S&P 500 is up 0.96%, the Nasdaq is up 3.34%, and the Dow 30 is down 0.60%.

CNN's Fear & Greed Index now stands at 53 (Neutral) out of 100, down 13 points from last week. Details here

The top five trending stocks on Reddit are Palantir, Nvidia, Tesla, Archer Aviation, and SPY. Read More

Here is a summary of this week’s key economic releases:

Manufacturing Improving: The ISM Manufacturing PMI came better than expected, which points to positive sentiments. This is the first beat since April this year. The service sector has been driven by growth recently, and the manufacturing sector is underperforming. It seems the rate cuts are helping manufacturing, which is also reflected in the regional Fed outlooks.

The labor market is doing Well. The unemployment rate ticked slightly (by 0.1%) to 4.2% this month. It is still well below the historical average of 5.7%. The MoM nonfarm payroll and the hourly earnings rate came better than expected. The hurricane and boring strike impacted last month's numbers, but this week's data release confirmed that those issues were short-term.

Target Rate Probabilities for Dec 18th FOMC Meeting:

CME FedWatch:* Data as of 7 Dec 2024 01:26:42 CT

FRONT PAGES:

Bank of China Gold Buying: China's central bank resumed gold purchases in November after a six-month hiatus, signaling a renewed interest in diversifying reserves. Read

Scotia’s Potential Risk Transfer Deal: According to sources, the Bank of Nova Scotia is exploring a $350 million risk-transfer deal tied to a $5 billion portfolio of U.S. dollar corporate loans. The transaction, representing about 7% of the loan book, remains confidential as discussions are ongoing. Read

Credit Card Balances Surge: US consumer borrowing surged in October, led by the biggest credit-card balance increase since mid-2022. Total credit rose $19.2 billion, far exceeding the $10 billion forecast, after a revised $3.2 billion gain in September. Read

Increasing Product Returns: The National Retail Federation and Happy Returns project that product returns will account for 17% of all goods sold in 2024, amounting to $890 billion. This marks an increase from 15% in 2023. Read

Broadcom Unveils New Tech: Broadcom announced its custom chip unit has developed technology to boost semiconductor speeds, addressing growing demand for generative AI infrastructure. Read

Apple Plans Modem Rollout: After over half a decade of development, Apple is set to unveil its in-house modem system next spring, marking a significant milestone in its quest for hardware self-reliance. Sources familiar with the matter indicate this move will reduce Apple's dependence on third-party suppliers like Qualcomm, potentially reshaping its supply chain dynamics. Read

Palantir’s and Anduril Announce Partnership: Palantir Technologies and Anduril Industries have joined forces to leverage defense data for artificial intelligence (AI) training, marking a significant collaboration in defense technology. This announcement follows Anduril's partnership with OpenAI, signaling a broader strategic push to integrate cutting-edge AI capabilities into national security operations. Read

Record ETF Inflows: Wall Street's optimism has driven investors to pour a record $1 trillion into US ETFs in 2024, marking a new industry milestone. Read

Source: Bloomberg

EARNINGS UPDATE:

Salesforce Beat: Salesforce surpassed quarterly sales expectations and issued an optimistic forecast for its new AI-integrated offerings. The company relies on Agentforce to drive growth, capitalizing on the increasing demand among tech firms for AI agents capable of autonomously completing tasks. Read

Synopsys Miss: Synopsys has forecasted fiscal 2025 revenue below Wall Street expectations, citing a decline in China sales driven by tighter U.S. export controls on chip technology. The primary revenue challenge stems from weakening demand in China, exacerbated by newly expanded restrictions on chip technology exports. The growing list of barred Chinese customers and lingering uncertainties over chip manufacturing capabilities have led remaining clients to delay new projects. Read

EARNINGS PREVIEW:

Date | Symbol | Name | Time |

9-Dec | BHP | Bhp Billiton Ltd ADR | -- |

9-Dec | ORCL | Oracle Corp | After Close |

11-Dec | ADBE | Adobe Systems Inc | After Close |

12-Dec | AVGO | Broadcom Ltd | After Close |

12-Dec | COST | Costco Wholesale | After Close |

CURATED INSIGHTS:

Bank of New York Mellon’s 2025 Outlook: I came across this BNY report this week, which highlights some of the key points I mentioned in this newsletter recently. Mainly that US stocks are not overvalued. I won’t care much about the S&P 500 target BNY gave for the end of 2025, as I don’t believe these targets matter. So let me highlight key points:

Easing Cycle Phase: In 2025, the Fed's easing, U.S. economic resilience, and pro-growth policies are set to support moderate growth. Lower interest rates will boost spending and activity, creating opportunities for investors. U.S. equities are likely to outperform as strong earnings and AI-driven efficiency enhance profit margins.

Resilient US:

Robust Labor Marlet: The unemployment rate is still historically low (4.1% vs. 5.7% average).

Aggregate Consumer Demand Remains Intact.

US Continues to Lead Global Growth:

US Outperformance Is Justified: The figure below shows the long-term profit margins of the S&P 500. So, US companies are improving margins and, as I noted in the first section, showing robust earnings growth.

Importance of Staying Invested: This is the most important insight in this report. No one can time the market. Staying invested and dollar cost averaging are the best strategies.

Financial Stability Report: Below are the key insights from last month's Financial Stability Report.

The nominal Treasury term premium, reflecting investor compensation for holding long-term Treasuries, is near its highest since 2010. Option-implied interest rate volatility remains historically elevated.

Treasury market liquidity is crucial due to these securities' central role in the financial system. Metrics like market depth indicate persistently low liquidity, particularly in the on-the-run segment. Please check my blog, “Treasury Market Resilience: Key Developments and Future Outlook” for more details on this topic and the importance of the treasury market.

The net issuance of institutional leveraged loans, which had been weak since late 2022, turned moderately positive in Q3. Meanwhile, private credit, now 7% of total nonfinancial corporate debt, has grown rapidly, diverging from traditional business credit trends.

Fair value losses in fixed-rate assets remained sizable, and the sensitivity of the values of those assets to interest rates remained high.

During the March 2023 banking turmoil, heavy reliance on uninsured deposits was a key vulnerability for affected banks, including those that failed. Since then, banks have reduced uninsured deposits. However, many replaced this funding with short-term non-deposit sources or brokered and reciprocal deposits, which, despite being insured, may prove less stable than traditional core deposits during stress.

VIDEO’s OF THE WEEK:

We put your money to work

Betterment’s financial experts and automated investing technology are working behind the scenes to make your money hustle while you do whatever you want.

Please Share This Newsletter With Your Friends.

Also, check my blog here.

This newsletter's content is for informational and educational purposes only and should not be considered trading or investment recommendations. All the opinions in this newsletter are personal and do not belong to any organization.