In partnership with

Weekly Newsletter

📈 Biggest Weekly Jump In Treasury Yields Since 2001

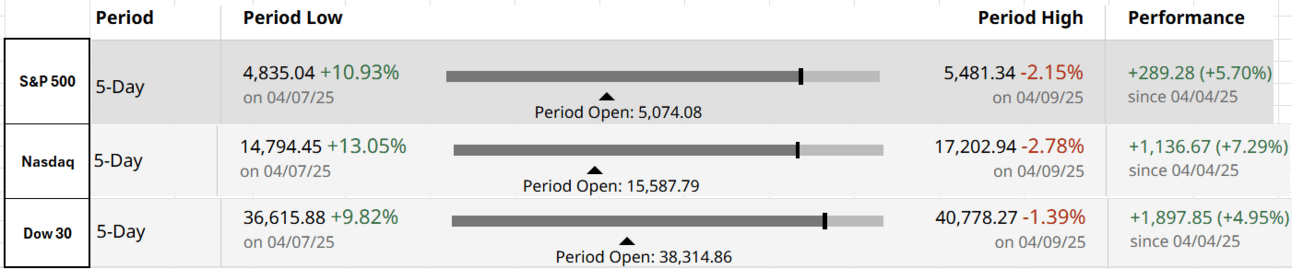

📊 Best Week for S&P 500 Since Nov 2023

🥇 Gold Records Best Week In Five Years

🧊 Lowest CPI Reading Since March 2021

🏦 Earning Season Kickoff: Market Volatility Boosts Banks

⚖️ Supplemental Leverage Ratio In Focus Amid Treasury Market Turmoil

📝 Key Points: Jamie Dimon’s Letter to Shareholders

QUOTE OF THE WEEK:

“We think the supplementary leverage ratio is an ill-advised ratio. Maybe it was born out of the financial crisis at a time when there was a lot of anti-bank sentiment, which was understandable at the time. But the people who pay the price today are market participants. The Treasury market is less well supported because of the existence of that ratio, in our opinion.” - Robin Vince, Bank of New York Mellon CEO

KEY US ECONOMIC EVENTS NEXT WEEK:

MARKET CLOSE:

CNBC: EOD April 12th

Good Afternoon. This was another busy week with a lot of action. Last week, I wrote that based on my analysis, it is premature to assume we will have a trade war. The selloff in treasuries forced this administration to announce a 90-day pause on all reciprocal tariffs except China. These positive developments helped stocks reverse half their losses from liberation day.

In addition, yesterday, smartphones, PCs, and other tech devices were exempted from all reciprocal tariffs, which gave massive relief to China. Approx. 25% of imports from China fall in this category. This is excellent news for the Mag 7s and the overall tech sector.

Weekly Gains:

Treasuries Sell-off:

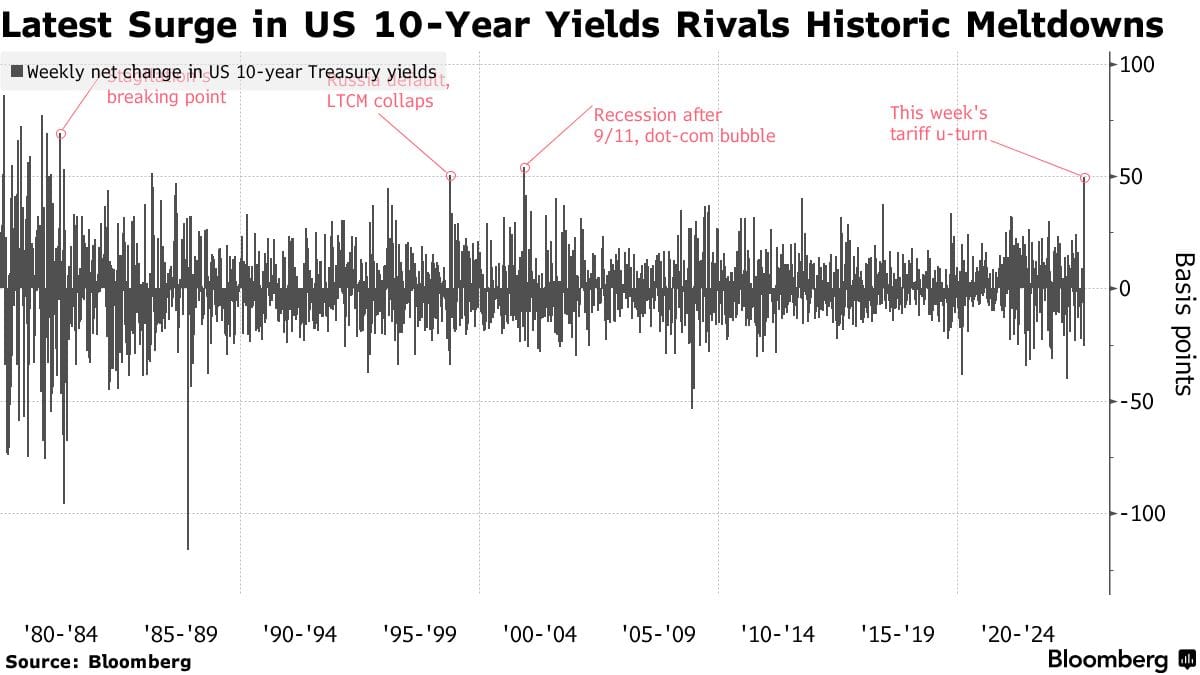

The main reason for the course correction was rising bond yields (bond yields go up when the price goes down). The tariff-related uncertainty has created massive volatility for all markets and, at least in the short term, lowered investor confidence in the US. This was reflected in a ~ 50 basis point surge in the US Treasury yields this week due to a lack of demand (and maybe basis trade unwinding), the highest in two decades. This shows that the global investors have lost confidence in the US due to recent policy uncertainty. This also impacted the US Dollar, which continued to depreciate against major currencies this week.A spike in bond yields from 3.8% to 4.12% in just four days forced a policy rethink. On April 8, weak demand for a $58 billion, 3-year Treasury note auction left banks to absorb 20.7% of the supply—the most since Dec 2023—signaling market stress and fading investor appetite.

The Bloomberg chart below shows the yield spike in 10-year USTs since the 1980s:

Dollar Depreciates:

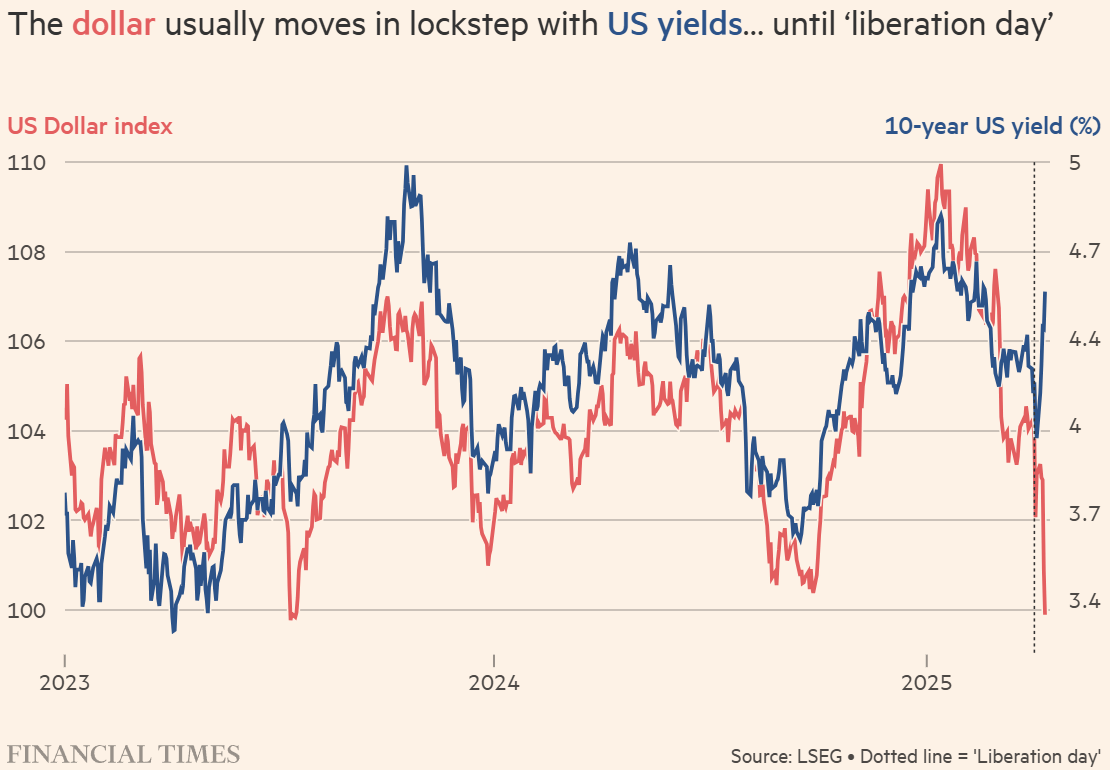

The US dollar hit a three-year low against the Euro on Friday, extending losses from last week after President Trump unveiled steep “reciprocal” tariffs on US trading partners. Generally, USD has historically appreciated during stress due to a flight to safety, but that did not occur this time. The chart below shows that the USD and 10-year bond yields have no longer been correlated since liberation day. During stress periods, investors used to rush to safe US Treasury assets, driving the demand for dollars (as to purchase US Treasuries, foreign investors need to convert their currencies into USD, driving demand for USD). These developments doubt the Dollar’s status as the world’s reserve currency. Investors/Central Banks have been moving towards Gold for safety in the past few years, and that trend is continuing, with Gold recording its best weekly gain in five years.

Uncertainty Will Persist:

Even though this week brought a lot of good news for stocks, uncertainty is not unusual with Trump. The current pause is for 90 days. The future depends on the negotiations with other countries. 10% base tariffs are still in place for all countries, making US tariffs higher than at the start of the year.Lesson: Markets clawed back half of this week's losses from liberation day. This again highlights that timing the market is impossible. Selling in panic on bad days will prove terrible, as one might miss the sharp reversals by remaining on the sidelines. It’s always best to sell in strength and buy during weakness—easier said than done.

Roth Conversion Option:

Not financial advice, but if you have stocks in your traditional IRAs that have dropped in value a lot, this is a good opportunity to move them into a Roth IRA through the backdoor. So that you limit your tax bill, when these stocks recover in the Roth IRA, the gains are tax-free for the long term. I just wanted to note this so you can discuss this with your financial advisor and make an appropriate decision according to your specific situation.

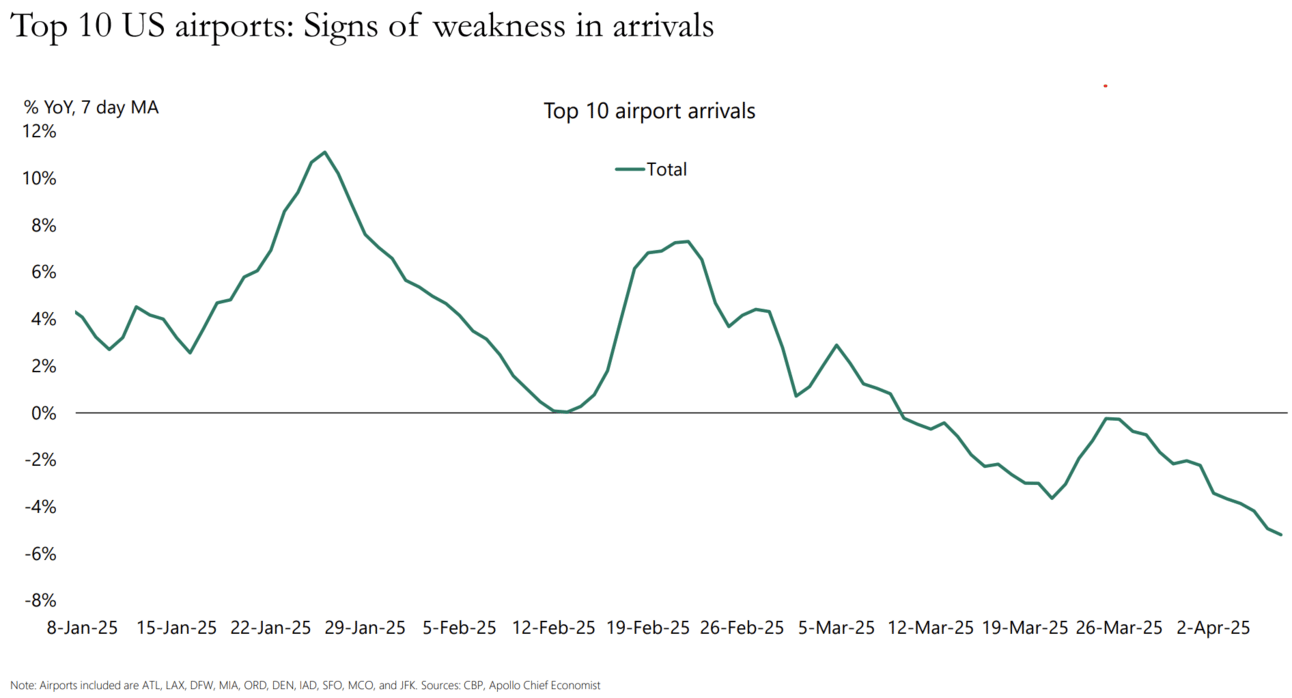

Local Vacation Will Be Cheaper This Summer:

Multiple reports indicate a steep decline in foreigners traveling to the US or cancelling their plans due to the ongoing trade war and the strict enforcement of immigration rules and checks at the airports. European and Canadian travellers are avoiding the US, which is bad for the hospitality and travel industry and is expected to make the local vacation cheaper this summer.

Source: Apollo

For the week:

The S&P 500 is up 5.70%, the Nasdaq is up 7.29%, and the Dow 30 is up 4.95%.

CNN's Fear & Greed Index now stands at 13 (Extreme Fear) out of 100, up 9 points from last week. Details here

The top five trending stocks on Reddit are SPY, Tesla, enCore Energy, MAGA, and Nvidia. Read More

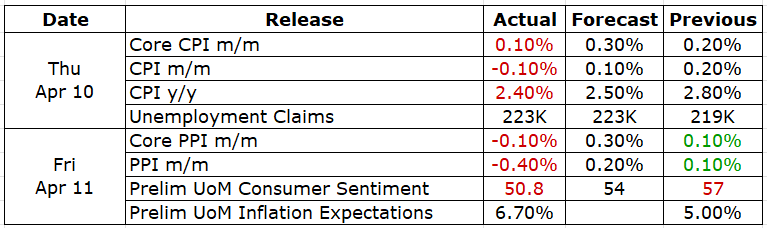

Here is a summary of this week’s key economic releases:

Better Than Expected CPI:

CPI declined 0.1% in March, led by a 6.3% drop in gasoline, pulling headline inflation down to 2.4% YoY from 2.8% in February. Food prices continued to rise (+0.4% m/m), and core inflation (ex. food and energy) edged up 0.1% on the month, bringing its annual rate to 2.8%, the slowest since March 2021. Falling prices in used cars, airfares, and insurance offset gains in personal care, education, and new vehicle purchases. Based on this, the end-of-month PCE release should be good. The Cleveland Fed March PCE forecast is at 2.2%.

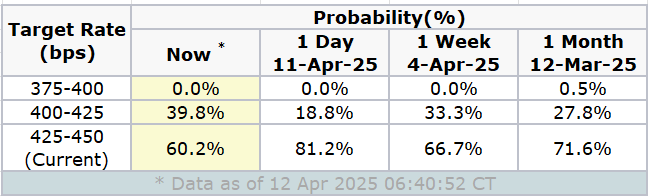

Target Rate Probabilities for May 7th FOMC Meeting:

CME FedWatch

CURATED INSIGHTS & ANALYSIS:

Key Points - The FOMC Minutes:

The core indicators to assess maximum employment are: unemployment rate, job vacancies, the employment-to-population (EPOP) ratio, and the labor force participation rate (LFPR).

Over the intermeeting period, Treasury yields declined, equity prices fell, credit spreads widened, and the dollar depreciated.

Some indicators suggested that conditions in money markets continue to tighten.

The ON RRP facility is nearly depleted, and repo market conditions have tightened. Portfolio runoff (Fed balance sheet reduction) will likely result in lower bank reserves. Slowing portfolio runoff will be effective.

The majority of foreign central banks eased policy during the intermediate period. They were increasingly noting the elevated uncertainty about trade policy.

Short-term funding markets stayed orderly. Secured rates initially rose, reversing December’s ON RRP dip, then eased later.

The labor market is not seen as a major inflation source, and there are concerns that core inflation may be more persistent. Participants emphasized keeping longer-run inflation expectations anchored.

Most participants see the policy well-positioned to wait for clarity amid elevated uncertainty.

Supplemental Leverage Ratio (SLR):

From JP Morgan to BNY Mellon, multiple bank CEOs openly criticized the SLR this week, so I thought of covering this at a high level. Criticism of SLR is not new, and Jay Powell, in multiple interactions, has mentioned that the FRB is working on revising these rules. Below are the high-level details:

The Supplementary Leverage Ratio (SLR) measures a bank’s Tier 1 capital against total leverage exposure, which includes all on-balance-sheet assets (like Treasuries and reserves) and some off-balance-sheet exposures:SLR = Tier 1 Capital / Total Leverage Exposure

The SLR treats Treasuries and reserves the same as risky assets, penalizing balance sheet expansion and discouraging banks from holding Treasuries or providing repo financing, especially in volatile markets. The Fed temporarily exempted treasuries and reserves from the SLR scope after March 2020, post-COVID stress. That relief ended in March 2021.

With issuance surging and no exemption, the SLR is blamed as a binding constraint for some banks. It reduces their balance sheet capacity, thereby restricting market participation and the ability to provide liquidity when needed the most.

Key Points - Jamie Dimon Letter to Shareholders:

The letter is full of philosophy and wisdom, but I list only the key points and my take in some cases (in italic). Some of his comments on the trade deficit are spot on in the context of events in the last two weeks:Despite the unsettling landscape, the US economy remains resilient, with consumers still spending and businesses still healthy.

There are many ways to fix unfair trade, but this needs to be done correctly or not at all. The trade deficits, by their nature, are not good or bad. The US trade deficit over the last 20 years is $12T, which is probably large, but this has led to foreign investments in the US.

The other side of the trade deficit is an investment surplus, which has resulted in foreign investors owning $30T of US securities. In contrast, the US investors own only $ 16T of foreign securities.

The US needs to be broadly trusted and reliable to protect its status as the world's reserve currency. This week's dollar depreciation highlights the importance of this point.

The CCAR stress tests are flawed, and the numbers are inaccurate. They unfairly misled the public about the bank's true strength.

The Supplemental Leverage Ratio and G-SIB surcharge treats US Treasury securities and repurchase agreements as far riskier than they are. This is covered above in detail.

The Liquidity Coverage Ratio treats all other securities and loans as riskier than they are. I don't wholly agree with Jaime Dimon on this point. The LCR is a standard rule for all banks; hence, it has standard haircuts, inflows, and outflows rates. Maybe Jamie finds them more stringent (especially for loans) for JP Morgan as it's a well-run bank with sophisticated risk management infrastructure. However, considering the broader applicability of the rule, some conservatism makes sense. Data from the recent few stress periods shows that all other securities (outside US Treasuries), especially off-the-run bonds, can see sharp haircut widening.

Before the Great Financial Crisis, banks used to have 15% of their assets held as liquid assets, and they now hold 30%. As per Jamie, this additional capital and liquidity, sitting idle, could be put to better use. I am not sure how Jamie can say this confidently that excess liquidity can be deployed without increasing the risk. It’s a very high-level generic statement. The liquid assets in banks have gone up mainly due to the Liquidity Coverage Ratio requirements. The banking stress of March 2023 proved that the smaller institutions subjected to the lenient US LCR standard due to the tailoring rules suffered. It's a highly complex topic, and I am not sure this statement makes sense without specifics.

The biggest risk for JP Morgan is Geopolitical Risk, e.g., Cyber attack, energy disturbance, etc.

The US deficit remains large, at 6.6% of GDP, and it’s not sustainable. We can’t say whether it will create a real problem in six months or six years - the sooner we deal with it, the better.

It costs $225 to maintain a consumer checking account. Out of which, $150 is fixed. If we add litigation costs and cost of capital, we will have to add another $25, i.e., the total cost to maintain a checking account is $250. Consumers pay for these accounts by the bank retaining net interest, around 2.25% or ~$275 per account. However, for the lower balance accounts, which are the majority, this is $25. Banks also receive certain fees on these accounts, which are ~$100. For the lower balance accounts, our cost to maintain and operate them is far more than what we make from them.

Complacency, arrogance, bureaucracy, and BS kill companies.

FRONT PAGES:

Tariff Exemptions: Smartphones and computers will be excluded from Trump’s 145% China tariffs announced earlier this month. The guidance also exempts semiconductors, solar cells, flat panel displays, flash drives, memory cards, and SSDs used in tech hardware. Read

Bond Selloff: Trump’s trade war triggered a bond selloff, pushing 10-year yields to their biggest weekly jump in 20+ years as investors retreated. Excluding one-offs, the firm posted $11.30 per share, beating the $10.08 estimate. Read

Dollar Slump: The dollar slumped in early European trade, hitting multiyear lows against the euro and Swiss franc, extending overnight losses as Trump’s tariff war weighed on sentiment. Read

Stablecoins & 20 Yr Bond in Focus: The U.S. Treasury seeks input from primary dealers on stablecoins and potential tweaks to the 20-year bond auction schedule, including a shorter when-issued period. Read

Trade Deals: The U.S. is reviewing tariff offers from 15 countries and nearing deals with several, said White House adviser Kevin Hassett after Trump unexpectedly rolled back some duties. Read

Gold Keeps Surging: Gold surged past $3,200 on Friday as a weakening dollar and rising U.S.-China trade tensions fueled recession fears, driving investors to safe-haven assets. Read

EARNINGS UPDATE:

Morgan Stanley Beat: Morgan Stanley beat Q1 estimates as stock trading revenue jumped 45%, driven by strong client activity amid global volatility, especially in Asia and hedge fund operations. Read

JP Morgan Chase Beat: JPMorgan beat Q1 profit estimates on record equities trading and strong investment banking fees, but stayed cautious on recession risks. CEO Jamie Dimon reiterated concerns over trade wars as firms adapt to Trump’s tariffs. Read

BNY Mellon Beat: BNY Mellon posted a 17% jump in Q1 profit, fueled by strong asset growth and new client inflows despite tough market conditions. Read

Wells Fargo Beat: Wells Fargo beat earnings expectations, but CEO Charlie Scharf warned of a likely economic slowdown this year, citing concerns over growth-impacting Trump-era tariffs. Read

Blackrock Beat: BlackRock’s Q1 net income slipped 4% to $1.51B due to acquisition-related costs, while revenue rose 12%. AUM hit a record $11.584T. Excluding one-time items, EPS came in at $11.30 vs. $10.08 expected. Read

EARNINGS PREVIEW:

Date | Symbol | Name | Time |

14-Apr | GS | Goldman Sachs Group | Before Open |

15-Apr | BAC | Bank of America Corp | Before Open |

15-Apr | JNJ | Johnson & Johnson | Before Open |

16-Apr | ABT | Abbott Laboratories | Before Open |

16-Apr | ASML | Asml Holdings NY Reg ADR | Before Open |

17-Apr | AXP | American Express Company | Before Open |

17-Apr | NFLX | Netflix Inc | After Close |

17-Apr | SCHW | The Charles Schwab Corp | Before Open |

17-Apr | TSM | Taiwan Semiconductor ADR | Before Open |

17-Apr | UNH | UnitedHealth Group Inc | Before Open |

22-Apr | DHR | Danaher Corp | Before Open |

22-Apr | GE | GE Aerospace | Before Open |

22-Apr | ISRG | Intuitive Surg Inc | After Close |

22-Apr | RTX | Rtx Corp | Before Open |

22-Apr | TSLA | Tesla Inc | After Close |

22-Apr | VZ | Verizon Communications Inc | Before Open |

VIDEOs OF THE WEEK:

The Supply Chain Crisis Is Escalating — But This Tech Startup Keeps Winning

Global supply chain chaos is intensifying. Major retailers warn of holiday shortages, and tech giants are slashing forecasts as parts dry up.

But while others scramble, one smart home innovator is thriving.

Their strategic move to manufacturing outside China has kept production running smoothly — driving 200% year-over-year growth, even as the industry stalls.

This foresight is no accident. The same leadership team that saw the supply chain storm coming has already expanded into over 120 BestBuy locations, with talks underway to add Walmart and Home Depot.

At just $1.90 per share, this resilient tech startup offers rare stability in uncertain times. As investors flee vulnerable companies, this window is closing fast.

Past performance is not indicative of future results. Email may contain forward-looking statements. See US Offering for details. Informational purposes only.

Please Share This Newsletter With Your Friends.

Also, check my blog here.

This newsletter's content is for informational and educational purposes only and should not be considered trading or investment recommendations. All the opinions in this newsletter are personal and do not belong to any organization.