In partnership with

Weekly Newsletter

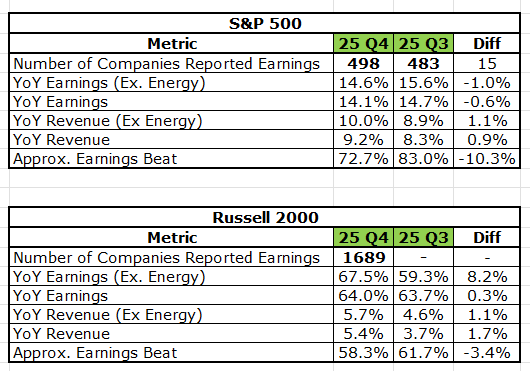

📊 Q425 Earnings Recap

📉 Nasdaq Enters Correction

🏛️ Weak Two-Year Auction

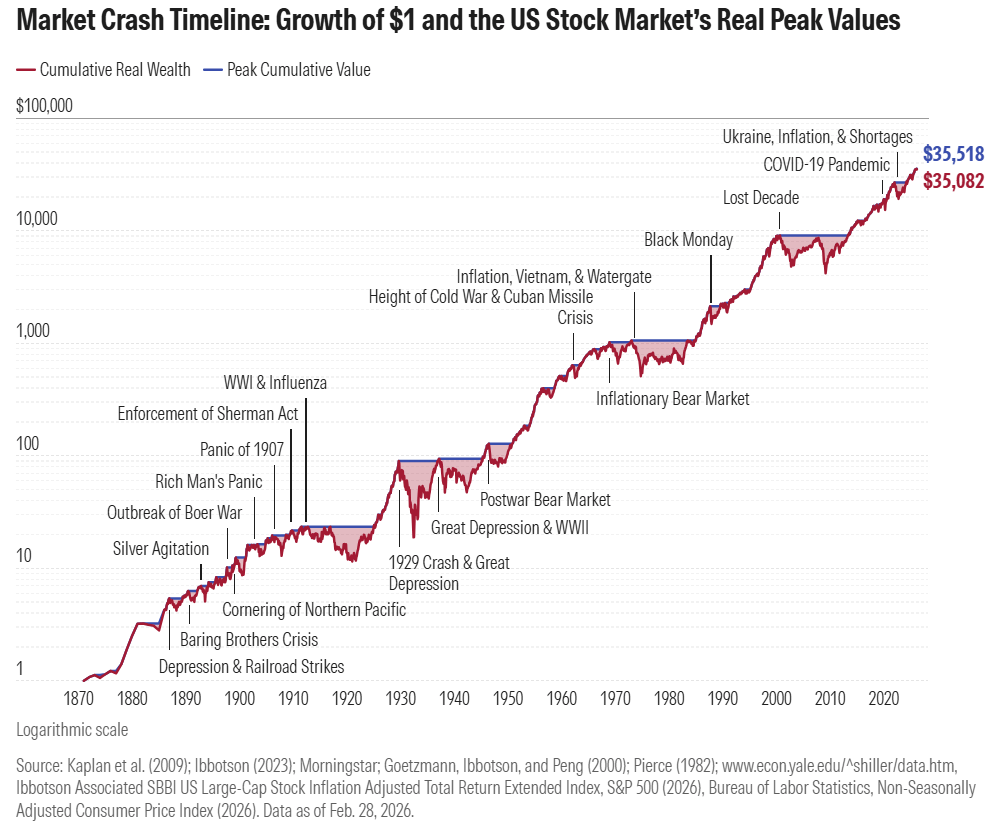

📚 150 Years Markets History

🛢️ The Velocity Of Depletion And Structural Risks In Oil

🤖 OpenAI Shuts Sora, ARM Launches First In-House Chip

🏠 Mortgage Rates Hit Six-Month High

QUOTE OF THE WEEK:

“The Persian Gulf situation that we've been modeling out for risk managers, and I was one for a long time. We're always gaming out what would happen if there were a closure of the Strait of Hormuz. The gaming was $150 to $200 barrel of oil and a minimum 10% correction in the S&P 500.” - Steve Sosnick, Interactive Brokers chief strategist

KEY US ECONOMIC EVENTS NEXT WEEK:

MARKET CLOSE:

CNBC - EOD 3/27

WEEKLY MARKET WRAP:

Good Afternoon. The market sold off for the 5th straight week with all major indices reporting losses. The uncertainty due to the Iran war is putting pressure on all risk assets and valuations, especially for growth tech stocks, which have come down significantly - forward PE of 21x vs 28k at the peak. A prolonged war beyond 2-3 more weeks will be terrible for Oil prices and, by extension, equities. More on this in the curated insights section.

Below are the key things to note this week:Nasdaq enters correction:

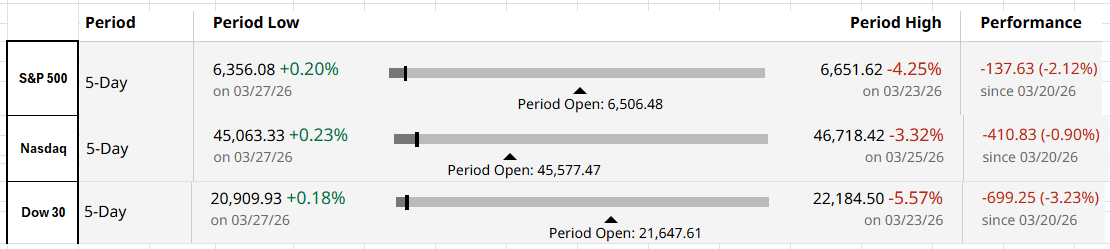

Nasdaq 100 has entered correction territory, down ~11% from its October peak as the index declined to 23,335. The move marks the first correction since the April 2025 tariff-led selloff, driven by rising Iran-related geopolitical risk and growing skepticism around AI monetization timelines, shifting market sentiment from leadership-driven optimism to caution.

Selloff has been led by mega-cap tech. Microsoft (-34%) and Meta (-29%) have been key drags, with Meta also facing legal pressures. NVIDIA is down ~19% as the durability of AI-driven demand is questioned, while enterprise software names like Workday and Atlassian have fallen >40%, reflecting concerns around AI disruption.

Despite near-term weakness, the earnings outlook remains resilient. The Magnificent Seven are expected to deliver ~19% profit growth in 2026, vs. ~16% for the broader S&P 500. Valuations have reset to ~21x forward earnings from ~28x at the peak, now slightly below historical averages.

Weak 2-Year Auction Reflects Soft Demand:

The U.S. Treasury’s $69B 2-year note auction cleared at 3.936% with a 2.44 bid-to-cover ratio, a result that pointed to softer demand than markets were looking for. A key sign of weakness was primary dealers taking 24.1% of the issue, well above recent norms, indicating that end-investor participation was light and that dealers had to absorb more supply. The weak auction pushed 2-year yields higher, reinforcing concern that sticky inflation and oil-driven macro risks could keep expectations of Fed easing under pressure.For the week:

The S&P 500 is down 2.12%, the Nasdaq is down 0.90%, and the Dow 30 is down 3.23%.

Barchart

CNN's Fear & Greed Index now stands at 10 (Extreme Fear) out of 100, down 5 points from last week. Details here

The top five trending stocks on Reddit are SPY, Microsoft, META, Micron, and QQQ. Read More

Liquidity:

Banking Reserves + ON RRP: Banking reserves remain at approximately $3.03 trillion. ON RRP balance remains immaterial.

Standing Repo Operations: The New York Fed’s standing repo operation (primarily reflecting SRF take-up) as of March 27th is zero.

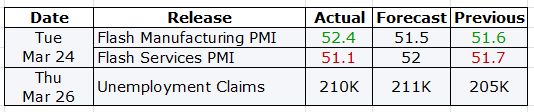

Here is a summary of this week’s key economic releases:

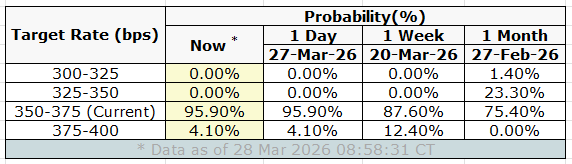

Target Rate Probabilities for April 29th FOMC Meeting:

CME Fedwatch

CURATED INSIGHTS & ANALYSIS:

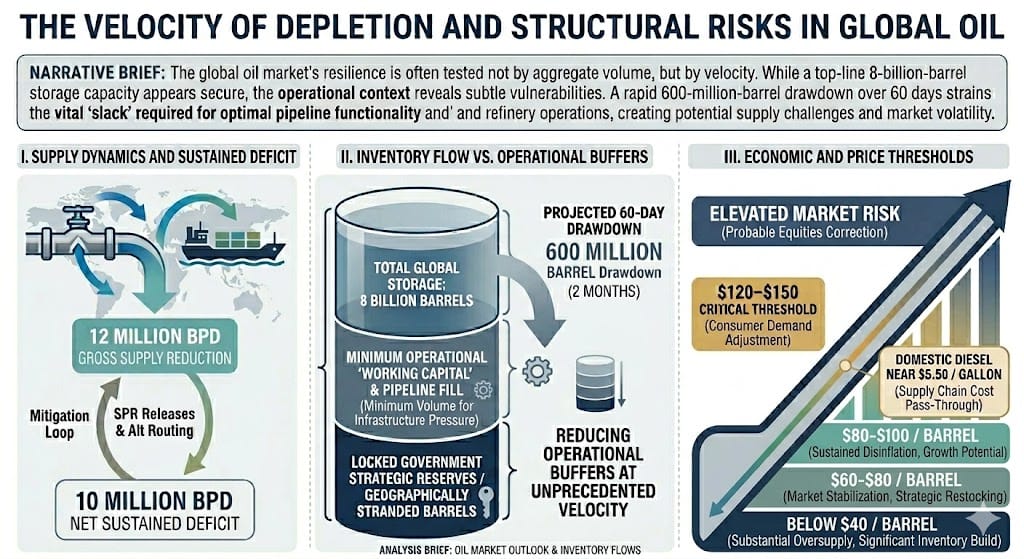

The Velocity of Depletion and Structural Risks in Oil:

Primal Thesis

The global oil market doesn't break on volume — it breaks on velocity. Even with 8 billion barrels in global storage, draining 600 million barrels in 60 days wipes out the critical slack that keeps pipelines pressurized and refineries functional.

Roughly 12 million barrels per day of energy supply have been taken offline. Even accounting for strategic reserve releases and alternative pipeline routing, a persistent deficit of 10 million barrels per day remains. At this run rate, global storage faces a 600-million-barrel drawdown over just a two-month window.

Relying on the 8-billion-barrel top-line figure as a comfort metric masks severe structural vulnerabilities. A significant portion of that capacity is strictly working capital — the minimum volume required to keep pipelines pressurized and global refinery plumbing operational. Millions of additional barrels are either locked in government strategic reserves or geographically stranded in regions facing acute shortages. When the operational slack disappears, the supply chain physically breaks down. Even minor logistical delays begin triggering panic buying and extreme price spikes.

A prolonged disruption of two to four more weeks is projected to push crude to the critical $120–$150 threshold — the range where aggressive demand destruction sets in. Compounded by domestic diesel prices approaching $5.50 a gallon, cost pass-through across the truck-dependent domestic supply chain becomes unavoidable, and broader equities face a high-probability path into bear market territory.

Morningstar analysis of 150 years of market history:

Crashes are recurring, not exceptional; over 150 years, markets fell hard repeatedly but always recovered to new highs.

The edge is not timing the bottom; it is staying positioned through the drawdown.

Diversification usually worked: Morningstar finds the 60/40 portfolio suffered 45% less pain than all equities across historical crashes.

The exception was 2022–25, when stocks and bonds fell together, delaying the 60/40 recovery until June 2025.

History’s message is simple: drawdowns are inevitable, recovery timing is unknowable, and discipline matters more than prediction.

Morningstar

Q425 Earnings Recap:

Primal Thesis

The Q4 earnings season drew a clear line between rebound and quality. Small caps posted the stronger headline earnings growth, but large caps still led where it matters more: revenue strength, beat consistency, and sector quality.

Small caps are recovering; large caps are executing better. The Russell 2000 story still looks more recovery- and margin-driven, while the S&P 500 appears supported by stronger underlying demand and a cleaner top-line profile.

The beat profile still favors large caps. The broader takeaway from the quarter is that S&P 500 results were not just better to look at, but also more dependable and consistent across companies.

Technology remains the S&P 500’s structural advantage. Large-cap leadership remains anchored in sectors with stronger revenue conversion, better execution, and more durable earnings power, which gives the index a higher-quality foundation.

The Russell 2000 rebound still looks less durable. Beneath the headline growth, the small-cap improvement appears more tied to cyclical normalization and margin recovery than to broad-based expansion.

Valuation makes that distinction more important. Small caps still need broader, more durable top-line growth to fully justify their premium and the optimism embedded in forward expectations.

Bottom line: The S&P 500 remains the higher-quality earnings story, while the Russell 2000 remains the higher-beta recovery story.

FRONT PAGES:

Musk Weighs Large Retail Slice for SpaceX IPO: Elon Musk is considering allocating up to 30% of SpaceX’s IPO to individual investors, roughly three times the typical retail share, to build a loyal shareholder base and support trading after listing. The structure would mark a clear break from the usual Wall Street IPO model. Read

Mortgage Rates Hit Six-Month High: Rising oil prices tied to the prolonged Middle East war have revived inflation concerns, pushing the average 30-year fixed mortgage rate to 6.38% from 6.22% last week, according to Freddie Mac. The fourth straight weekly increase threatens home sales during the key spring season and further pressures housing affordability. Read

Arm’s Strategic Shift: Arm is moving beyond licensing for the first time with the launch of its in-house AGI CPU for data centers, marking a major shift in strategy as it begins competing directly with its own customers. Meta is the first buyer, aligning with its multi-gigawatt AI data center buildout and up to $135 billion in planned capex this year. Read

OpenAI Shuts Sora, Ends Disney Deal: OpenAI has discontinued its AI video-generation app Sora, less than 2 years after its high-profile debut, and will also wind down its $1 billion content partnership with Disney, marking a strategic shift toward robotics and physical-world applications. Read

EARNINGS UPDATE:

Primal Thesis

Gamestop Mixed: Q2 FY2026 delivered record revenue, gross margin, EPS, and free cash flow. Revenue rose to $23.86B from $8.05B a year ago and $13.64B in the prior quarter. GAAP gross margin was 74.4% and operating margin 67.6%. Operating cash flow reached $11.90B, with adjusted free cash flow at $6.90B. The board approved a 30% dividend increase to $0.15 per share. Strong AI demand and tight supply support another record Q3.

Cintas Beat: Revenue rose 8.9% YoY to $2.84B, with 8.2% organic growth. Gross margin reached a record 51.0%, up 40 bps. Diluted EPS increased 9.7% to $1.24, and net income was $502.5M. The company paid a $180.0M quarterly dividend on March 13, 2026, raised FY2026 guidance to $11.21B–$11.24B in revenue and $4.86–$4.90 in adjusted diluted EPS, and announced a deal to acquire UniFirst on March 10, 2026.

Karman Mixed: Q4 revenue rose 47.4% YoY to a record $134.5M. GAAP EPS was $0.06, and non-GAAP EPS was $0.11, in line with consensus. Adjusted EBITDA increased 59% to $42.0M, with a margin at 31.2%. Backlog reached $801.1M, up 38.2% YoY. FY2026 guidance was raised to $715–$730M in revenue and $207–$218M in adjusted EBITDA.

Paychex Mixed: Revenue rose 20% YoY to $1.81B, with operating income up 14% to $792M and adjusted operating income up 22% to $863.2M. Diluted EPS increased 9% to $1.56, while adjusted EPS rose 15% to $1.71. Management Solutions grew 23% to $1.35B, and PEO & Insurance rose 9% to $397.5M. Interest expense climbed to $68.1M on acquisition debt. The company returned over $1.5B to shareholders for the fiscal YTD.

Carnival Beat: Adjusted EPS rose 50% YoY to $0.20, while GAAP diluted EPS was $0.19. Revenue hit a record $6.2B, with gross margin yields up nearly 10% and net yields up 2.7% in constant currency. Bookings reached a record, 2026 bookings are up double digits with ~85% already booked, and fuel consumption per ALBD fell 4.7%. Management also introduced 2029 PROPEL targets and announced an initial $2.5B share buyback.

EARNINGS PREVIEW:

Date | Symbol | Name | Time |

31-Mar | NKE | Nike | After Close |

VIDEO’s OF THE WEEK:

The $66 Billion Opportunity in Weddings

Fact: People will spend for love.

Americans spent $66 billion on weddings last year. And, as always, flowers were a non-negotiable part of that spend. This highlights a unique market opportunity for The Bouqs Co. right now.

Famous for cutting the time it takes flowers to travel farm-to-door by 3x, The Bouqs Co. is already one of the country’s largest floral subscription services. But their latest expansion to 70+ brick-and-mortar stores could unlock more high-margin events, like weddings.

They already have 100% YoY growth in counties where stores have opened, with more than $1.2m in revenue per store.

You can join this chapter as they capture more of the $100b global floral market. Become an early shareholder in The Bouqs Co.

This is a paid advertisement for The Bouq’s Regulation CF offering. Please read the offering circular at https://invest.bouqs.com/

Please Share This Newsletter With Your Friends.

Also, check my blog here.

This newsletter's content is for informational and educational purposes only and should not be considered trading or investment recommendations. All the opinions in this newsletter are personal and do not belong to any organization.