In partnership with

Weekly Newsletter

💫 Circular Spending In AI

💥 $2 Trillion Wiped Out From Stocks On Friday

🤖 OpenAI’s SORA Hit 1 Million Downloads In 5 Days

📊 Key Points From FOMC Meeting Minutes

📈 Small Caps Outperformance In Q2

💼 Earnings Season Kicks-Off Next Week

QUOTE OF THE WEEK:

“Why would we stay with the US then? Well, because we think the fundamentals are better here. We think growth improves next year. And while interest rates are falling, that's not a usual combination—to see growth improving while interest rates fall. Usually, you see rates rise. So that's a really great combination for mergers and acquisitions. It could help business development companies. It could help any number of alternative investments as well.” - Paul Christopher, Wells Fargo Investment Institute head of global investment strategy.

KEY US ECONOMIC EVENTS NEXT WEEK:

MARKET CLOSE:

CNBC EOD Oct. 10th

WEEKLY MARKET WRAP:

Good Afternoon. Down week for the markets, thanks to Friday’s sell-off after President Trump’s post, which wiped out $2 trillion in market value. All major indices dropped ~2.5% for the week, though the markets were in positive territory for the week until Friday morning.

Below are the key things to note this week:

Trump vs. China: President Trump announced an additional 100% tariff on China on Friday. Trump announced this after China tightened its control over the rare earths market, which it dominates with a 70% global share. Beijing now requires export licenses for nearly all rare earth products and will deny those tied to military use, with applications reviewed individually. This is the reason the market sold off on Friday.

Q3 Earnings Kick Off: The New earnings season kicks off next week with major banks scheduled to report. The Friday panic may last for a couple more days, but the earnings will take over the narrative from Tuesday and can prompt a recovery. Banks are expected to report strong earnings, and overall, this can be another good earnings season considering the robust economy and other macro data till now.

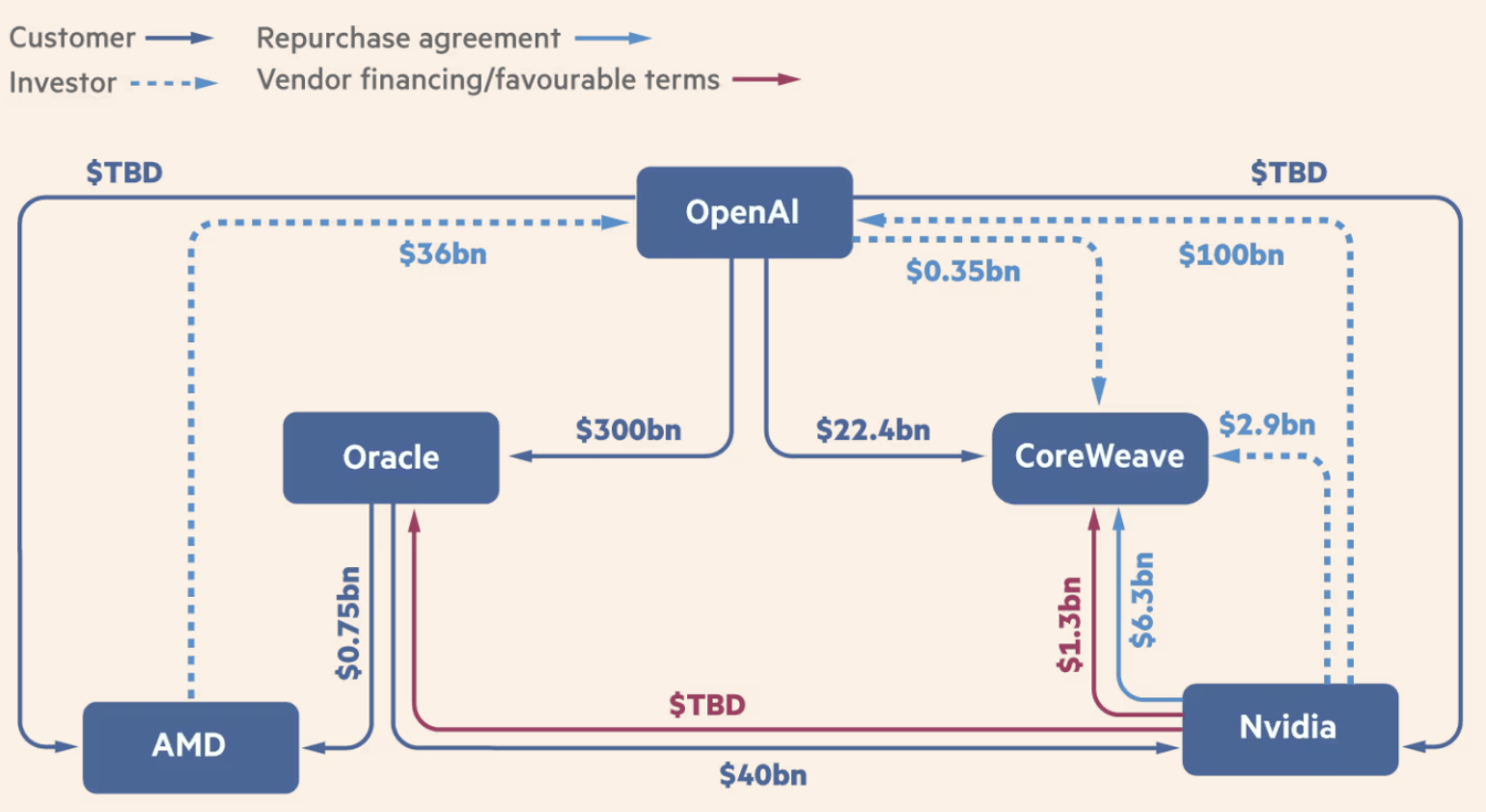

Circular Spending in AI:

In the last two weeks, multiple deals were announced, primarily by OpenAI and Nvidia, prompting a debate about circular spending in the AI space, where companies are investing in each other. I don’t think it’s a significant concern, as these are early-stage coordination among firms building the AI backbone. The capital remains “circular” because the ecosystem is still concentrated, but it’s producing tangible assets — such as chips, servers, and data centers — that anchor long-term productivity.

Source: FT, Morgan Stanley Research

Key Circular Deals:OpenAI ↔ Nvidia: Nvidia plans to invest up to $100 billion in OpenAI, while OpenAI spends heavily on Nvidia GPUs.

OpenAI ↔ AMD: OpenAI signs a multi-billion chip deal and gets equity warrants in AMD, creating a mutual exposure loop.

OpenAI ↔ Oracle (Stargate): Massive multiyear cloud deal—OpenAI rents compute from Oracle while Oracle gains from OpenAI’s expansion and valuation surge.

OpenAI ↔ CoreWeave: Expanded partnership worth about $22 billion; CoreWeave provides compute, partly financed by investors like Nvidia and Microsoft—both also OpenAI partners.

Microsoft ↔ CoreWeave/Nebius: Microsoft invests billions in AI cloud startups that, in turn, sell back capacity to Microsoft’s own Azure ecosystem.

For the week:

The S&P 500 is down 2.43%, the Nasdaq is down 2.53%, and the Dow 30 is down 2.73%.

Barchart

CNN's Fear & Greed Index now stands at 29 (Fear) out of 100, down 33 points from last week. Details here

The top five trending stocks on Reddit are SPY, AMD, Nvidia, DTE Energy, and 374Water. Read More

Here is a summary of this week’s key economic releases:

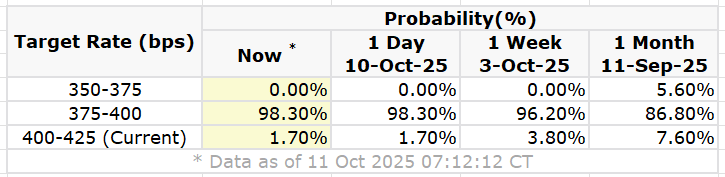

Target Rate Probabilities for October 29th FOMC Meeting:

CME FedWatch

CURATED INSIGHTS & ANALYSIS:

Key Points From FOMC Minutes:

Inflation rose modestly and stayed above target; tariff effects were smaller than expected, offset partly by productivity gains and slower wage growth.

Long-term inflation expectations stayed anchored, though near-term risks persisted.

Labor market softened—job gains slowed, unemployment rose to 4.3%, and revised data showed weaker underlying trends.

Participants cited lower immigration, an aging workforce, and sector-specific hiring as signs of reduced labor dynamism.

Real private domestic final purchases (PDFP)—a better gauge of underlying demand—expanded modestly, indicating moderate but steady growth.

Consumer spending firmed in Q3 after a soft first half, led by high-income households, while housing remained weak.

Business investment stayed solid, driven by high-tech and software; agriculture faced input cost pressures.

Treasury and funding markets stayed orderly; repo rates rose amid TGA rebuild and reserve decline, triggering limited SRF use.

Balance-sheet runoff continued smoothly; reserves are projected to be near $2.8 trillion by Q1 2026.

The Committee cut rates by 25 bps to 4–4¼%, reflecting a shift toward balance as inflation risks eased and employment risks rose.

Most supported further easing later this year if inflation moderates; a minority preferred holding steady to guard credibility.

Members stressed a balanced approach—avoiding both premature easing and excessive restraint.

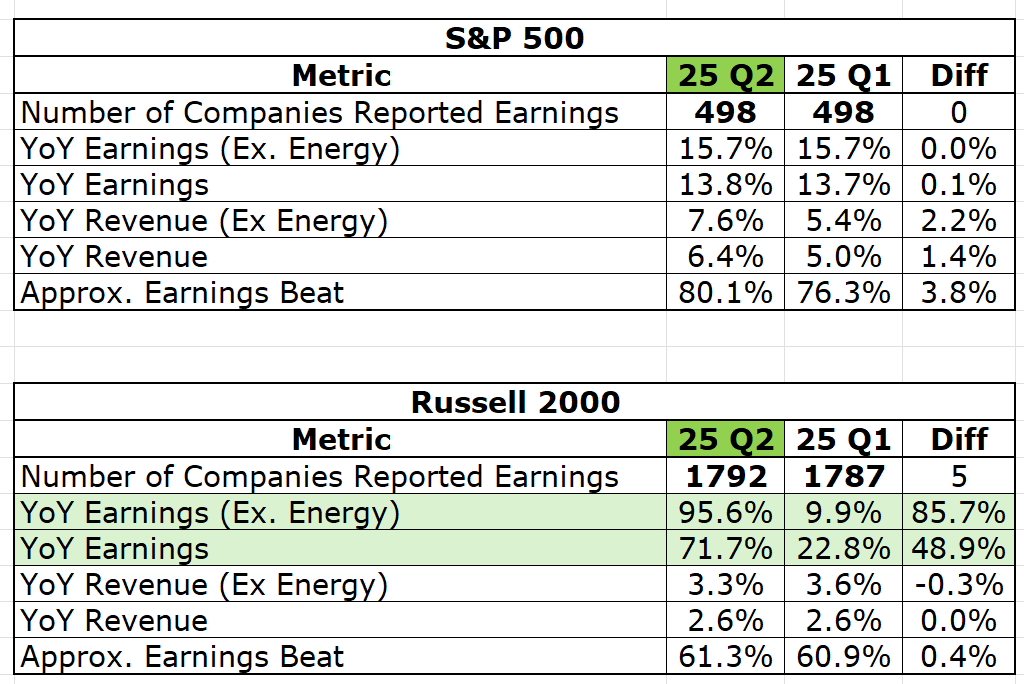

Small Cap Shines in Q2:

Q2-25 earnings season concluded this week with stellar performance overall by the US companies, contrary to the fears of tariff impact causing earnings recession at the start of earnings season. Small caps performed exceptionally well after a long time, and below is the QovQ comparison, which shows the magnitude of outperformance by the small-cap Russell 2000 stocks. As the Fed is expected to cut a few more times, this should benefit small caps in the next few quarters -

LSEG

FRONT PAGES:

New Tax Brackets: The IRS has raised federal tax brackets for 2026 to reflect inflation. The standard deduction will rise to $32,200 for joint filers and $16,100 for singles, alongside adjustments to capital gains brackets, estate tax exemption, and child tax credit eligibility. Read

Fifth Third to Buy Comerica: Fifth Third agreed to acquire Comerica in an all-stock deal worth $10.9 billion, creating the nation’s ninth-largest lender—the biggest U.S. bank merger of the year as dealmaking accelerates under a Trump administration focused on faster approvals. Read

OpenAI Invests in AMD: OpenAI will acquire up to a 10% stake in AMD through a deal tied to deploying 6 gigawatts of Instinct GPUs over several years, starting with 1 gigawatt in 2026. AMD granted OpenAI a warrant for up to 160 million shares, vesting with deployment and price milestones. Read

More China Tariffs: Trump announced a 100% tariff on Chinese imports effective Nov. 1, alongside export controls on all critical software. The move retaliates against China’s new export limits on rare earth minerals, which supply about 70% of global demand and are vital for autos, defense, and semiconductors. Read

Apple’s AI Acquisition: Apple is close to acquiring engineers and technology from Prompt AI, a computer vision startup founded by UC Berkeley researcher Tete Xiao and BAIR co-founder Trevor Darrell. Read

AI Video App: OpenAI’s Sora, the short-form AI video app, crossed 1 million downloads within five days of launch. It lets users create short videos from text prompts for free, but has drawn backlash from the Motion Picture Association over copyright concerns. Read

EARNINGS UPDATE:

Primal Thesis

Constellation Brands Beat: Constellation Brands reported adjusted earnings of $3.63 per share, down 16% year over year but above estimates. Net profit rose to $2.65 from a loss of $6.59 last year, while operating margin narrowed 210 bps to 35.7% amid higher costs. Sales fell 15% to $2.48B, less than expected, as beer volumes declined 7% and wine and spirits dropped 19%. Beer depletions fell 2.7%, led by weakness in Modelo and Corona, partly offset by Pacifico and Victoria.

Pepsico Beat: Revenue rose 2.7% to $23.9 billion, with organic sales up 1.3%, below the 2.1% consensus. Growth was led by a 5.5% gain in Europe, the Middle East, and Africa, offset by a 3% decline in North American Foods. Total volume for food and beverages fell 1%. Operating profit dropped 11%, weighed down by double-digit declines in North American Beverages and LatAm Foods—Non-GAAP EPS of $2.29 beat estimates by $0.03.

Delta Beat: Delta Air Lines projected a stronger-than-expected close to 2025 and a solid start to next year, supported by higher fares and resilient premium travel demand. The airline expects Q4 adjusted earnings between $1.60 and $1.90 per share, versus $1.65 expected, with revenue growth of up to 4%, ahead of Wall Street’s 1.7% forecast.

EARNINGS PREVIEW:

Date | Symbol | Name | Time |

14-Oct | BLK | Blackrock Inc | Before Open |

14-Oct | C | Citigroup Inc | Before Open |

14-Oct | GS | Goldman Sachs Group | Before Open |

14-Oct | JNJ | Johnson & Johnson | Before Open |

14-Oct | JPM | JP Morgan Chase & Company | Before Open |

14-Oct | WFC | Wells Fargo & Company | Before Open |

15-Oct | ABT | Abbott Laboratories | Before Open |

15-Oct | ASML | Asml Holdings NY Reg ADR | Before Open |

15-Oct | BAC | Bank of America Corp | Before Open |

15-Oct | MS | Morgan Stanley | Before Open |

16-Oct | ISRG | Intuitive Surg Inc | -- |

16-Oct | SCHW | The Charles Schwab Corp | Before Open |

16-Oct | TSM | Taiwan Semiconductor ADR | Before Open |

17-Oct | AXP | American Express Company | Before Open |

VIDEO’s OF THE WEEK:

Trusted by millions. Actually enjoyed by them too.

Most business news feels like homework. Morning Brew feels like a cheat sheet. Quick hits on business, tech, and finance—sharp enough to make sense, snappy enough to make you smile.

Try the newsletter for free and see why it’s the go-to for over 4 million professionals every morning.

Please Share This Newsletter With Your Friends.

Also, check my blog here.

This newsletter's content is for informational and educational purposes only and should not be considered trading or investment recommendations. All the opinions in this newsletter are personal and do not belong to any organization.