Weekly Newsletter

📈 S&P 500 Climbs To New Record

🏦 FOMC Decision Next Week

💻 Key Tech Earnings Due Next Week

💪 Strong Earnings Momentum Continues

🧩 Fed Plans Overhaul Of Banking Stress

💹 Fundamentals Behind Market Returns Since Pandemic

QUOTE OF THE WEEK:

“When we look at the beginning of 2025, we were trading around 22 times on PE on the market, and we're around that level still. So yes, the market is elevated, but when you look at the MAG 7—the biggest-weighted names in the S&P 500 —that's where the earnings are. We think that right now the MAG7 earnings could be up about 15% this quarter, year-over-year. But when you look at the last quarter, they were expected to be up about 14–15% and they were up about 26%. So you've got to follow the earnings. Yes, we're trading at an elevated PE, but the market can trade at an elevated PE for a prolonged period of time.” - Brooke May, Managing Partner at Evans May Wealth.

KEY US ECONOMIC EVENTS NEXT WEEK:

MARKET CLOSE:

CNBC EOD 10/24

WEEKLY MARKET WRAP:

Good Afternoon. Positive week for the markets with the S&P 500 hitting an all-time high, powered by better-than-expected CPI numbers and continued strong earnings.

Below are the key things to note this week:

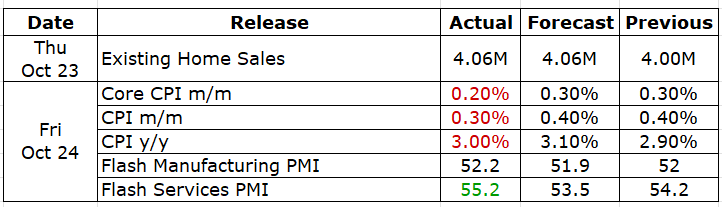

Better CPI: The CPI inflation numbers came in better than expected, with Headline CPI rising 0.3% in September, bringing annual inflation to 3%, slightly below forecasts of 0.4% and 3.1%. This seals the rate at next week’s FOMC meeting and another later in the year. The Fed’s preferred PCE inflation measure is expected next Friday, but it is not certain if it will be released due to the Government shutdown. Based on the CPI data, institutions project the core PCE to be 2.8% and the headline to be 2.7%, which is good.

The Fed Announces Stress Test Proposal: The Federal Reserve proposed greater transparency in its annual stress testing framework, including disclosing the underlying models and the proposed 2026 scenario for public comment. It also outlined a new process to gather feedback on future scenarios and model changes, invited input on the scenario design framework, and introduced more objective standards—particularly for the global market shock component.

Strong Flash PMI: U.S. business activity accelerated in October, marking the second-fastest pace this year, driven by substantial gains in new orders across both manufacturing and services. Price pressures cooled, with output prices rising at the slowest rate since April, even as input costs stayed elevated.For the week:

The S&P 500 is up 1.92%, the Nasdaq is up 2.31% and the Dow 30 is up 2.20%.

Barchart

CNN's Fear & Greed Index now stands at 33 (Fear) out of 100, up 6 points from last week. Details here

The top five trending stocks on Reddit are Beyond Meat, SPY, Dragonfly Energy, Vivakor, and AMD. Read More

Here is a summary of this week’s key economic releases:

Target Rate Probabilities for October 29th FOMC Meeting:

CME FedWatch

CURATED INSIGHTS & ANALYSIS:

This Time It’s Really Different:

The S&P 500 hit an all-time high this week, and many keep wondering why the market keeps going higher. There is still a lot of capital on the sidelines waiting for a pullback, which is not coming. There may be some correction, but it doesn’t look like a significant drawdown like we saw in April is possible unless there is a major black swan event. There are multiple reasons for the continued US stock market surge, which I have covered multiple times in this newsletter. Below is some recent analysis on this topic from McKinsey and the Financial Times -

All Time High Global Economic Profits:

As per the analysis by McKinsey & Company, Global economic profit among the world’s 4,000 largest nonfinancial companies has surged to roughly $1.2 trillion annually between 2020 and 2024—about 50% higher than in 2005–2009—even after adjusting for inflation. Despite the pandemic shock, this marks an apparent reversal from the prior 15 years, when aggregate economic profit—earnings above the cost of capital—had stagnated mainly.

Cashflow Return on Investments:FT reported that UBS’s preferred measure of returns—the CFROI for tech companies—has risen sharply in recent years. Now will the trend reverse? Doesn’t look like it in the short term, considering the tangible AI efficiency improvements and continued investments in this space.

UBS, FT

Same With Return On Equity:

Since the Pandemic, the return on equity of S&P 500 companies has improved far better than the previous 15-year history.

In summary, the continued stock market outperformance since the pandemic is due to strong fundamentals, and it’s not a bubble as of now. During the dot-com era, most new companies were not profitable, but this time, it's highly profitable, cash flow-positive large-cap tech stocks in the US are driving the markets.

FRONT PAGES:

Refinance Demand Surge: Mortgage rates fell to a one-month low, spurring a 4% rise in refinance applications, now 81% higher than a year ago. The average 30-year fixed rate for conforming loans ($806,500 or less) slipped to 6.37% from 6.42%, with points down to 0.59 from 0.61 for 20% down payments. Homebuyer demand, however, remained muted. Read

Cooler CPI: Headline CPI rose 0.3% in September, bringing annual inflation to 3%, slightly below forecasts of 0.4% and 3.1%. Core CPI, excluding food and energy, increased 0.2% on the month and 3% year-over-year, also under expectations. The annual CPI ticked up 0.1ppt from August while core inflation eased from prior months. Read

Tether’s Profit: Tether expects nearly $15B in profit this year, per CEO Paolo Ardoino. It’s in talks to raise up to $20B for a 3% stake, valuing the firm near $500B. With $183B of USDT in circulation—about 60% of the stablecoin market—Tether operates at a staggering 99% profit margin. Read

Big Banks Stablecoins Push: Zelle announced plans to enable cross-border money transfers for users across its network, though details and timing remain unclear. The move marks a significant expansion beyond its U.S.-only model. Unlike domestic payments, the service will use stablecoins—digital tokens pegged to fiat currencies—now under new federal oversight after Trump’s July bill. Read

EARNINGS UPDATE:

GE Beat: GE raised its 2025 operating profit outlook to $8.65–$8.85 billion from $8.5 billion and now expects free cash flow of $7.1–$7.3 billion, up from $6.9 billion. Third-quarter adjusted revenue rose 26% to $11.3 billion, with earnings of $1.66 per share, reflecting strong execution and major aerospace wins, including over 400 engines for Qatar Airways.

Coca-Cola Beat: Q3 non-GAAP EPS rose to $0.82, beating estimates by $0.04, on revenue of $12.5B, up 5% year over year. Global unit case volume grew 1%, while organic revenue increased 6%. Comparable operating margin improved to 31.9% from 30.7% a year earlier. The company projects organic revenue growth of 5–6% in the near term.

Netflix Miss: Q3 revenue rose 17% to $11.51B, in line with estimates, while GAAP EPS of $5.87 missed by $1.10. Q4 revenue is expected at $11.96B, matching consensus, with adjusted EPS of $5.45. Full-year revenue guidance of $45.1B implies 16% growth (17% ex-FX), consistent with prior expectations. The 2025 operating margin forecast is trimmed to 29% from 30%.

Phillip Morris: Q3 adjusted EPS rose 17% to $2.24, beating estimates by $0.14, on revenue of $10.85B, up 9.5% and $190M above consensus. The smoke-free segment led growth, with shipments up 16.6%, net revenue up 17.7%, and gross profit up 19.5%. Combustible volumes fell 3.2%, but revenue and profit rose 4.3% and 7.7%. The company raised full-year EPS guidance to $7.46–$7.56, assuming 6–8% revenue growth versus 7.7% expected.

RTX Beat: The parent company of Pratt & Whitney and Raytheon Missiles & Defense raised its 2025 adjusted profit forecast to $6.10–$6.20 per share, surpassing earlier guidance and analyst expectations. Third-quarter earnings of $1.70 per share also exceeded estimates, driven by broad-based sales and profit growth, reflecting a strong rebound in commercial aviation and steady defense demand.

Texas Instruments Beat: The company reported mixed Q3 results with softer guidance ahead. EPS was $1.48, while revenue rose 14% year-over-year to $4.74B. Analog sales rebounded 16% to $3.73B, exceeding estimates, while embedded processing rose 8.6% to $709M, below expectations. Other segment revenue increased 11% to $304M.

IBM Beat: IBM reported Q3 revenue of $16.33B, up 9.1% year-over-year, with earnings of $2.65 per share. Software brought in $7.21B, consulting $5.32B, infrastructure $3.56B, financing $200M, and other revenue $38M. Free cash flow rose 15% from a year earlier to $2.37B.

AT&T Mixed: AT&T reported adjusted EPS of $0.54, in line with estimates. Revenue rose 1.7% to $30.71B, missing forecasts by about $200M. For 2025, it expects low single-digit consolidated service revenue growth, adjusted EPS toward the upper end of $1.97–$2.07 (midpoint $2.02 vs. $2.06 consensus), and adjusted EBITDA growth of 3% or more. Mobility revenue is projected to grow 3%+, with fiber broadband up in the mid-to-high teens.

Themo Fisher Beat: The Waltham-based healthcare firm reported adjusted EPS of $5.79 on $11.1B in revenue, up ~10% and ~5% YoY, beating estimates by $0.29 and $210M. Lab products & services rose ~4% to $5.97B, life sciences and analytical instruments grew ~8% and ~5% to $2.59B and $1.89B, and specialty diagnostics added $1.17B, all above forecasts. Operating margin improved 100 bps to 23.3%, while GAAP EPS held steady at $4.27.

Tesla Beat: Revenue rose 11.6% YoY to $28.1B, while EPS of $0.50 missed both consensus ($0.56) and last year’s $0.62. GAAP net income was $1.4B, and non-GAAP net income $1.8B. Operating margin declined to 5.8% from 10.8% last year but improved sequentially. Gross margin stood at 18.0% vs. 19.8% a year ago. Operating income fell 40% YoY to $1.62B. Adjusted EBITDA dropped to $4.23B with a 15.0% margin, while free cash flow surged to $3.99B vs. $1.25B expected.

Intel Beat: Intel posted a solid double beat, with Q3 non-GAAP EPS at $0.23—$0.22 above estimates, and revenue of $13.7B, up 3.2% Y/Y and over $560M ahead of expectations. Net income swung sharply to $4.1B from a $16.6B loss a year ago.

T Mobile Mixed: Q3 GAAP EPS came in at $2.41, slightly above estimates, with revenue of $21.96 B, up 8.9% year-over-year. The company posted record 2.3 M total postpaid net adds—the best in the industry. Postpaid phone net adds reached 1 M, the strongest Q3 in over a decade, while postpaid account adds rose 26% to 396 K, both marking industry-leading highs.

Procter & Gamble Beat: Q1 Non-GAAP EPS was $1.99, exceeding estimates by $0.09, with revenue up 3% year-over-year to $22.39B. The company reaffirmed FY26 EPS growth guidance of 3%–9% versus FY25’s $6.51 and core EPS growth of flat to +4% versus $6.83, implying a range of $6.83–$7.09 per share (midpoint $6.96), roughly a 2% increase.

EARNINGS PREVIEW:

Date | Symbol | Name | Time |

28-Oct | BKNG | Booking Holdings Inc | After Close |

28-Oct | NEE | Nextera Energy | Before Open |

28-Oct | NVS | Novartis Ag ADR | Before Open |

28-Oct | UNH | UnitedHealth Group Inc | Before Open |

28-Oct | V | Visa Inc | After Close |

29-Oct | CAT | Caterpillar Inc | Before Open |

29-Oct | GOOG | Alphabet Cl C | After Close |

29-Oct | GOOGL | Alphabet Cl A | After Close |

29-Oct | META | Meta Platforms Inc | After Close |

29-Oct | MSFT | Microsoft Corp | After Close |

30-Oct | AAPL | Apple Inc | After Close |

30-Oct | AMZN | Amazon.com Inc | After Close |

30-Oct | LLY | Eli Lilly and Company | Before Open |

30-Oct | MA | Mastercard Inc | Before Open |

30-Oct | MRK | Merck & Company | Before Open |

30-Oct | SHEL | Shell Plc ADR | -- |

31-Oct | ABBV | Abbvie Inc | Before Open |

31-Oct | CVX | Chevron Corp | Before Open |

31-Oct | LIN | Linde Plc | Before Open |

31-Oct | XOM | Exxon Mobil Corp | Before Open |

VIDEO’s OF THE WEEK:

Please Share This Newsletter With Your Friends.

Also, check my blog here.

This newsletter's content is for informational and educational purposes only and should not be considered trading or investment recommendations. All the opinions in this newsletter are personal and do not belong to any organization.