In partnership with

Weekly Newsletter

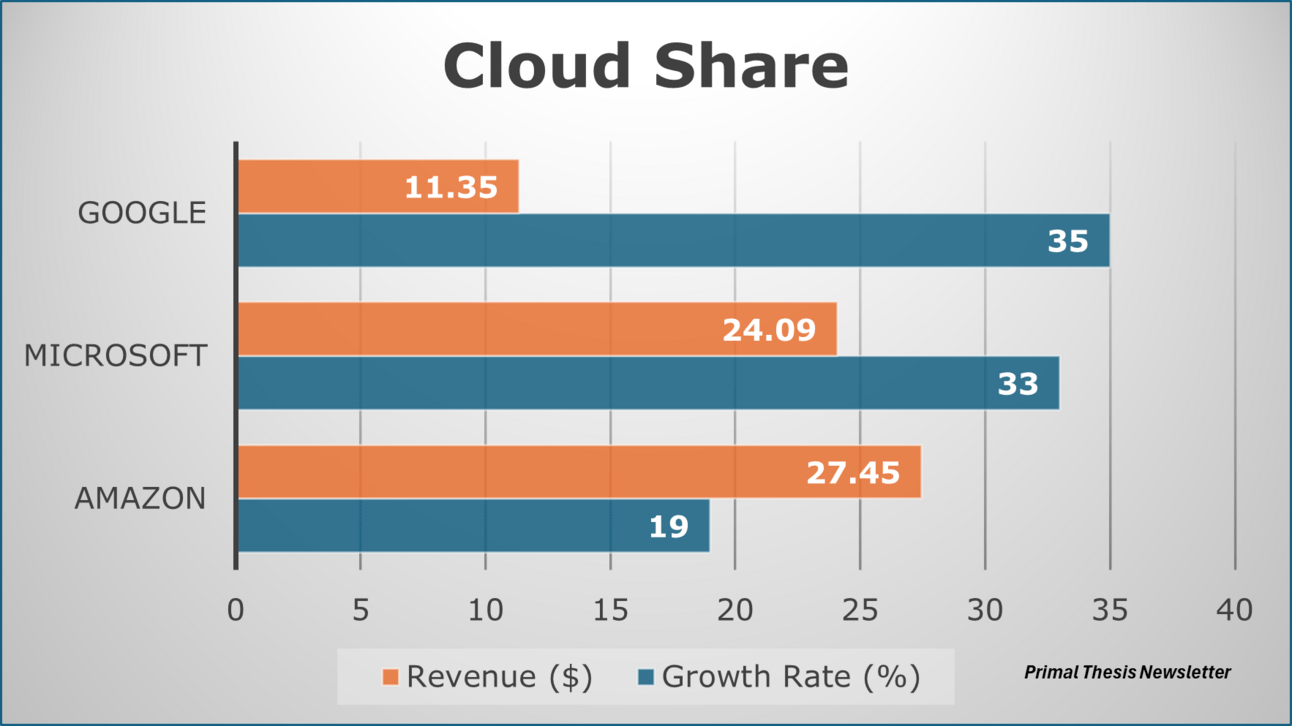

Cloud Growth Among Tech Giants

Inflation Close to The Fed Target

Netflix Wins The Streaming Race

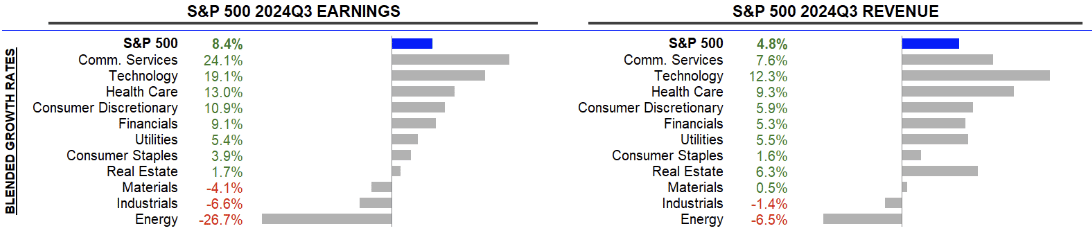

Q324 Earning Recap

Sweep vs. Split Election. What’s good for the markets?

Insights From The Autumn Alger Capital Markets Report

Key Takeaways from the BCBS Progress Report on Bank Turmoil

QUOTE OF THE WEEK:

“The end of financial repression, of zero interest rates and zero inflation, that era is over. Interest rates will be higher, will be challenged around the world. And the end of ‘the end of history’ — geopolitics are back and will be part of the challenge for decades to come,” Ted Pick - CEO, Morgan Stanley

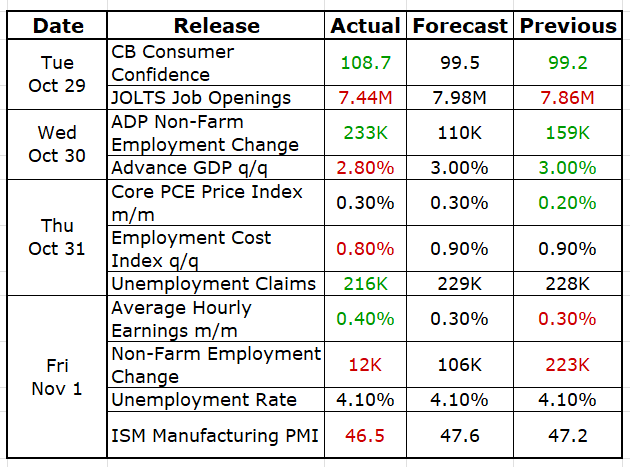

KEY US ECONOMIC EVENTS NEXT WEEK:

Source: Forex Factory

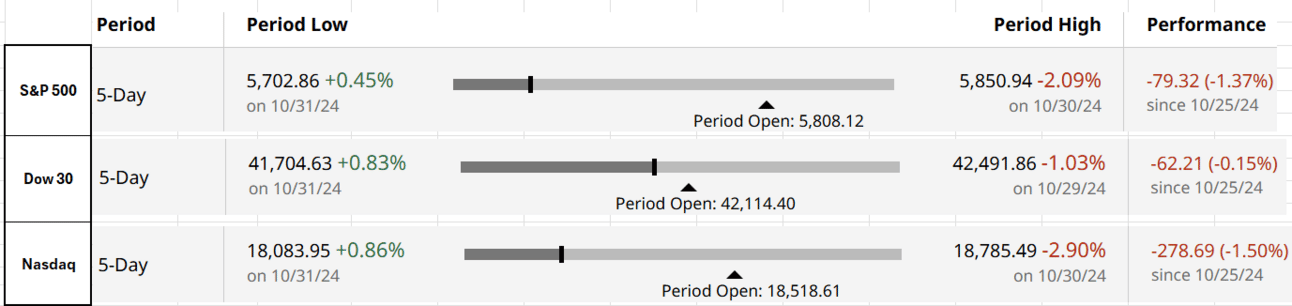

MARKET CLOSE:

CNBC - EOD Nov. 1st

Good Afternoon. This week was packed with earnings and macro data. To date, ~70% of S&P 500 companies have reported earnings. The curated insights section has more stats about earnings. The most crucial macro news is that the PCE inflation dropped to 2.1% from 2.3% last month. PCE is the Fed’s favored measure for its 2% inflation target, which it seems it has almost achieved now. The core PCE (PCE excluding volatile food and energy), however, increased to 2.7% from 2.4% last month. As this aligns with the Fed’s expectations, the Fed will cut the rate by 25bp next week. Market expectations per CME Fed watch also show a ~99% probability of a 25bp cut. The next week is crucial, with the results of the US elections on Tuesday and the Fed rate cut decision on Thursday.

For the week:

The S&P 500 is down 1.37%, the Nasdaq is up 1.50%, and the Dow 30 is down 0.15%.

Source: barchart

CNN's Fear & Greed Index now stands at 49 (Neutral) out of 100, down 10 points from last week. Details here

The top five trending stocks on Reddit are NVDA, SMCI, SPY, AMZN, and DJT. Read More

Here is a summary of this week’s key economic releases:

The Boeing strike and the hurricanes impacted the employment data released this week. Henne, the nonfarm payroll change of just 12000 can't be trusted, and we need to wait to see the future readings. In general, inflation is moving in the right direction (though the core PCE slightly increased), and the labor market is cooling.

Target Rate Probabilities for Nov 7th FOMC Meeting:

CME Fed watch: * Data as of 2 Nov 2024 03:32:39 CT

FRONT PAGES:

Nvidia is set to replace Intel in the Dow Jones Industrial Average, marking a significant shift in the semiconductor landscape. Nvidia shares have surged over 170% this year, contrasting with Intel’s loss of more than half its value. This is the first change to the index since February when Amazon joined the Dow. Read More

Berkshire Hathaway’s cash reserves surpassed $300 billion in the third quarter, as Warren Buffett ramped up his stock sales and paused share buybacks. According to Saturday's earnings report, the Omaha-based conglomerate’s cash holdings reached a record $325.2 billion by the end of September, up from $276.9 billion in the previous quarter. Read More

Google's cloud business grew 35% in the latest quarter, outpacing larger rivals Amazon and Microsoft. Its operating margin was 17%, lower compared to its main rivals. Amazon Web Services continues to rake in profit, recording an operating margin of 38% in the quarter. Amazon and Microsoft said demand for artificial intelligence services is outstripping their supply. Read More

JPMorgan Chase has agreed to pay $151 million to settle SEC charges, alleging that two of its units violated securities laws by failing to act in shareholders' best interests. The SEC stated that the bank’s violations included misleading disclosures to investors and restrictions on joint transactions and principal trades. Read More

Netflix has won the streaming war. Since implementing its password-sharing crackdown in May 2023, the streamer has gained over 50 million paying subscribers. Full-year operating margins are projected to reach 27%, with management suggesting the potential to eventually achieve margins comparable to broadcast networks, traditionally between 40% and 50%. Read More

Over 25% of all new code at Google is now generated by AI, says CEO Sundar Pichai. Read More

EARNINGS UPDATE:

AMD reported third-quarter results on Tuesday, meeting earnings forecasts and slightly exceeding revenue expectations. AMD’s gross margin expanded to 54%, the company said, due to higher data center revenue. Read More

Alphabet, Google's parent company, posted third-quarter earnings that exceeded expectations on both revenue and profit, driven by solid growth in its cloud division. Google’s search business contributed $49.4 billion in revenue, reflecting a 12.3% increase year-over-year. Read More

Microsoft’s strong earnings report couldn’t stop the stock from experiencing its sharpest drop in two years, as investors zeroed in on its cautious outlook for the current period. Read More

In its third-quarter earnings report on Wednesday, Meta reported user numbers below expectations and cautioned about a sharp rise in infrastructure costs for 2025. Read More

Amazon shares jumped in extended trading as the company posted earnings and revenue that surpassed expectations, driven by solid growth in its cloud and advertising units. Read More

Mastercard reported third-quarter profits above expectations on Thursday, as economic stability drove customers to increase their spending. Read More

Visa exceeded Wall Street expectations for fourth-quarter profit on Tuesday, with consumers brushing off economic concerns to spend on travel and dining. Read More

Eli Lilly's high-profile weight-loss and diabetes drugs missed Wall Street sales estimates on Wednesday, with inventory piling up in warehouses—a stark shift for the company after struggling to keep up with soaring demand. Read More

McDonald's exceeded third-quarter expectations, even as the company continues to address an ongoing E. coli outbreak investigation. Read More

EARNINGS PREVIEW:

Date | Symbol | Name | Time |

|---|---|---|---|

4-Nov | VRTX | Vertex Pharmaceutic | After Close |

6-Nov | ARM | Arm Holdings Plc ADR | After Close |

6-Nov | NVO | Novo Nordisk A/S ADR | Before Open |

6-Nov | QCOM | Qualcomm Inc | After Close |

7-Nov | ANET | Arista Networks Inc | After Close |

CURATED INSIGHTS:

Q3 Earnings:

S&P 500: Up till now, 349 companies from the S&P 500 have reported Q3 earnings, i.e., ~70%. Overall, the S&P 500 earnings have slowed compared to Q2, but it’s not material. This shows that the economy is doing well, and the Fed rate cuts will continue to help corporate earnings.

Source: LSEG

The table below compares Q3 S&P 500 earnings growth against Q2 earnings around the same point in Q2.

As of Nov. 1st

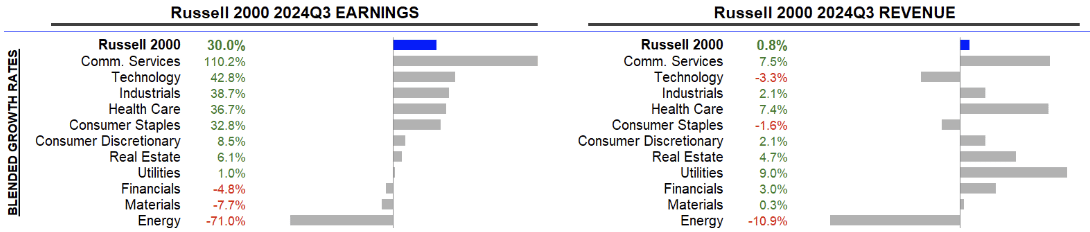

Russell 2000:

Source: LSEG

Below is a similar comparison for the Russell 2000. Until now, 605 Russell 2000 companies have reported earnings, i.e., ~30%. As most Russell 2000 companies are yet to report earnings, it will be too early to conclude, but compared to larger peer SP500, small caps are showing positive growth in both earnings and revenue. This also highlights that the smaller companies are late reporting results compared to larger companies. Q1 25 will be the first full quarter after the rate cuts, and hence, the late Q1 25 earnings (May/June) will confirm if the small caps are benefiting from the rate cuts or operating leverage due to the growing economy.

As of Nov. 1st

Insights from the Alger Autumn Report: The Autumn Alger Capital Markets Report has a lot of good information, but below are some of the crucial points according to me:

Split Congress is good for stocks as US equity returns are average 7.6% (sweep) vs. 12% (Split).

Small and mid-caps appear undervalued compared to the historical averages, especially in the backdrop of Fed cuts.

Historically, when the U.S. Federal Reserve cuts interest rates, corporate profit growth has accelerated to strong levels in the following quarters.

Allocation to alternative/private investments is expected to grow at the rate of 12% for the next 8-10 years. Check the second video below, which also talks about this topic. The privately held companies have gone sixfold in the last 25 years, so the trend is unsurprising.

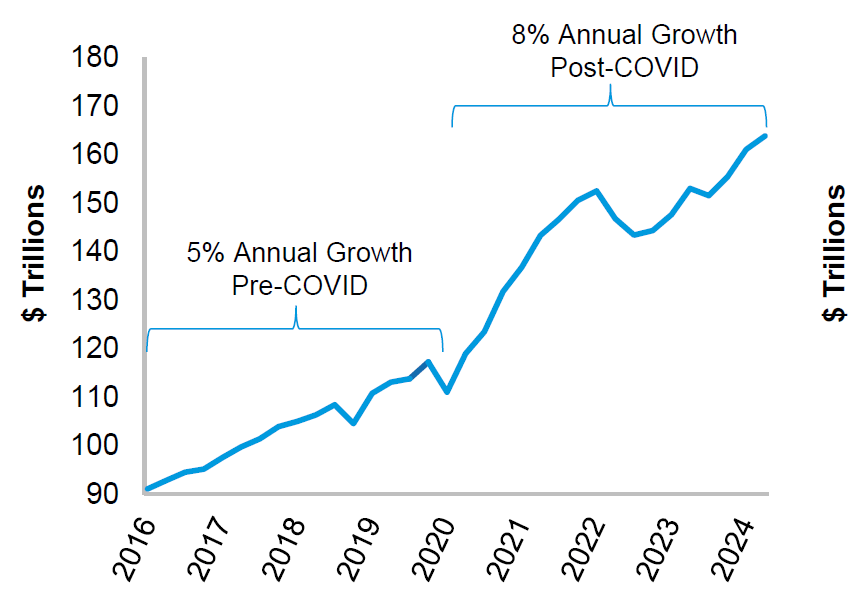

Household wealth has grown rapidly to over $160 trillion, supporting consumer spending. This growth rate accelerated post covid. This is primarily due to an appreciation of home prices and stock market performance.

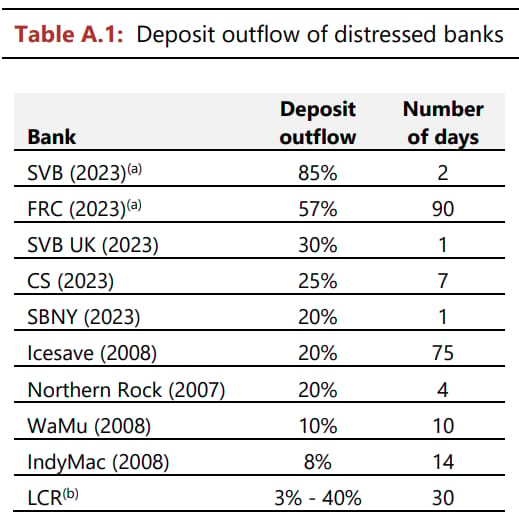

Basel Committee Progress Report on 2023 Bank Turmoil:

Last month, the Basel Committee on Baking Supervision (BCBS) published its progress report on the 2023 banking crisis (March-May 2023). Some of the critical findings in this report align with what I wrote in my blog explaining the collapse of Silicon Valley Bank in July last year. Especially the confirmation that the accounting treatment of HTM securities was not the central issue in the collapse of SVB, compared to other vital issues.

Please check my detailed blog covering the key takeaways from this report. Below is crucial information from the report summarizing the speed and materiality of deposit outflows from the banks that collapsed in the 2008 Global Financial Crisis and last year's 2023 Banking Stress.

VIDEO’s OF THE WEEK:

Invest Wisely with The Daily Upside

In this current market landscape, we all face a common challenge.

Many conventional financial news sources are driven by the pursuit of maximum clicks. Consequently, they resort to disingenuous headlines and fear-based tactics to meet their bottom line.

Luckily, we have The Daily Upside. Created by Wall Street insiders and bankers, this fresh, insightful newsletter delivers valuable market insights that go beyond the headlines. And the best part? It’s completely free.

Subscribe to my Newsletter here.

Also, check my blog here.

This newsletter's content is for informational and educational purposes only and should not be considered trading or investment recommendations. All the opinions in this newsletter are personal and do not belong to any organization.