In partnership with

Weekly Newsletter

📈 Equities End Four-Week Slide

🎤 Key Points From FOMC Press Conference

📊 Earning Season Recap

🤖 Elon Musk’s GROK AI Exposing Lies & Causing A Storm In India

🔥 PCE Inflation Forecasts

📚 UBS’s Analysis of 125 Years Of Stock Market History

QUOTE OF THE WEEK:

“You’ve got to think through every scenario. I still think the economy is resilient. And if we get past this bumpy period of some uncertainty, I still think that when the unemployment rate and the job market are settled in at what looks like full employment, if we can continue to make progress on inflation over the long run, I believe that rates 12 to 18 months from now will be lower than where they are today.” - Austan Goolsbee, Chicago Fed President.

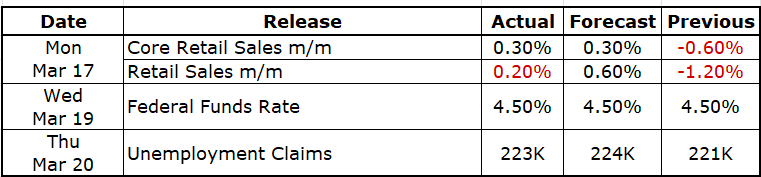

KEY US ECONOMIC EVENTS NEXT WEEK:

MARKET CLOSE:

CNBC - EOD March 22nd

Good Afternoon. Last week, I mentioned multiple positive market catalysts in the coming days, and this week, some positive events helped markets to stop falling further.

Next Friday has the most critical PCE release, which is expected to be 2.5%. Based on the CPI data, there is a strong chance that PCE will be better than expected, which will help the markets. Cleveland Fed forecasts that Feb PCE will be ~2.4% and core PCE is 2.6%.Below are some of the key highlights of the week:

FOMC Rate Decision:

The Fed decided to keep the rates unchanged in the meeting this week. Jay Powell also mainly talked positively in the FOMC press conference and explained that the hard data shows the economy is strong and soft data is showing uncertainty. However, we will have to see if some soft data will be reflected in hard data in the coming days.

Hard vs Soft Data: Hard data is actual data observed in stats or official calculations. Soft (Survey) data is based on surveys/opinions that can be unreliable due to various biases and sentiments. For example, after Trump's victory, his opponents suddenly changed their opinions about the economy, inflation, etc., from positive to negative a few months ago. They can’t be taken at face value.

Starting in April, the Fed will cut its monthly Treasury runoff cap from $25bn to $5bn, keeping the $35bn cap on agency debt and MBS unchanged. This means it will reinvest $20bn more into Treasuries each month (when $25bn matures), potentially driving yields down and prices up.

Check below to see what changed in the FOMC statement from last meeting:

Source: CNBC

Nvidia Joins High Spenders: At Nvidia’s high-energy GTC conference on Wednesday, Huang said the company plans to spend about $500bn on electronics over the next four years. Nvidia also announced new chips. CEO Jensen Huang unveiled Blackwell Ultra, set to ship in H2 2025, and Vera Rubin, NVIDIA’s next-gen GPU slated for 2026.

Retail Sales: February retail sales rose 0.2%, missing the 0.6% forecast but rebounding from January’s revised 1.2% drop. Core sales excluding autos climbed 0.3%, matching estimates. Despite slower headline growth, underlying demand remained resilient amid inflation and slowdown concerns.

Crew 10: All stranded astronauts landed safely on Earth this week.For the week:

The S&P 500 is up 0.51%, the Nasdaq is up 0.17%, and the Dow 30 is up 1.20%.

Source: Barchart

CNN's Fear & Greed Index now stands at 23 (Extreme Fear) out of 100, up 3 points from last week. Details here

The top five trending stocks on Reddit are Tesla, SPY, enCore Energy, Boyd Gaming, and Nvidia. Read More

Here is a summary of this week’s key economic releases:

Target Rate Probabilities for May 7th FOMC Meeting:

CME FedWatch

CURATED INSIGHTS & ANALYSIS:

Key Points from the FOMC Press Conference:

In this week's meeting, the Fed decided to keep the policy rate unchanged. Below are the key points from the Fed statement and FOMC press conference:Below are the key points from the FOMC press conference this week:

Balance Sheet: The Fed slowed down the balance sheet runoff as it saw some signs of tightness in money markets.

Economy:

There is a slowdown in consumer confidence. A survey of households and businesses points to heightened uncertainty about the economic outlook.

The economy is strong, with GDP rising at 2.3%. The labor market remains solid.

Hard data is very strong. The survey data (soft data) show a significant rise in uncertainty and downside risk. The relationship between survey data and hard data has not always been very tight. We will be observing for signs of weakness in real data.

Labor Market:

Wages are growing faster than inflation.

As per SEP, the unemployment rate is low at 4.1% and is expected to be 4.3% over the next two years.

It's been a low hiring and firing environment for quite some time.

The labor market is in balance.

Inflation:

Inflation has progressed towards the 2% inflation goal but remains slightly elevated.

For 2027, the median PCE projections are at the 2% target. Long-term inflation expectations remain consistent with the 2% target. The tariffs are not expected to impact long-term inflation expectations and are well anchored to 2%.

There is an increase in short-term inflation expectations. However, it will be tough to understand precisely how much inflation comes from the tariffs.

It’s tough to trace the impact of tariffs. For example, washing machines were tariffed in the last round of tariffs, but dryer prices increased as manufacturers followed the crowd. So, these things happen indirectly.

The impact of the last round of tariffs in President Trump's first tenor on inflation was transitory, and the same is expected this time.

GROK AI - Positive AI Story:

Elon Musk’s AI chatbot, Grok, has stirred controversy in India with blunt responses about political figures, including Prime Minister Modi and Rahul Gandhi. It questioned Modi’s educational claims, praised Gandhi’s academic background, and commented on caste-based discrimination, triggering debate online. Grok’s bold tone aligns with xAI’s mission to challenge norms, raising questions about how Indian authorities might respond.

This has irked the ruling dispensation in India, which has controlled local media in recent years. It is called “Godi Media” as it only praises Narendra Modi and his party. GROK exposed multiple lies spread by Modi’s party instead of being politically correct like other AI tools. I am unsure how long this will remain, as there is already news that the Indian government is in touch with X regarding concerns about GROK.

It will be essential to see if Elon Musk and his X back down to the political pressure or continue supporting the facts and GROK's unambiguous tone. GROK is an example of how AI can help spread facts when the local media fails to do so. ReadEarnings Recap:

Below is the analysis of the earnings season till now based on LSEG data and a comparison with the last quarter around the same time. Analysis shows that small companies improved their performance, with Russell 2000 QoQ companies reporting strong earnings and revenue growth. Large-cap S&P 500 companies also continue to report growth. It will be keen to see if the earning season starting next month shows any weakness due to the tariff war.

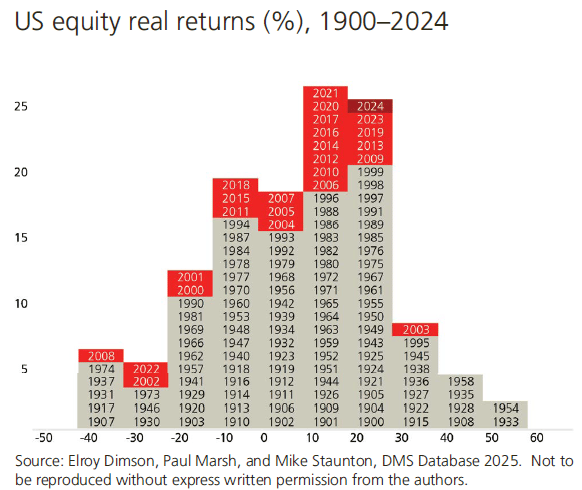

UBS Global Investment Return Yearbook:

UBS published an excellent analysis of what 125 years of history tells us about market returns. Below are the key points:The outperformance of stocks has been striking

Real returns on government bonds have been modest

It hasn’t always been a smooth ride

Patience has been valuable

Multi-asset diversification has helped manage volatility

There is a compelling case for diversification within equities

Inflation is also an important consideration in long-term returns

Gold and commodities can play a role in hedging inflation

Factors have delivered long-term outperformance, but some styles have disappointed for years. Momentum and low volatility outperformed broader equity markets than value, size, and income.

Check the report summary below:

FRONT PAGES:

FOMC Meeting: The FOMC held its key rate steady at 4.25%–4.5%, unchanged since December. It lowered its economic growth forecast and slightly raised its inflation outlook. Read

New Vice Chair of Supervision: President Trump named Fed Governor Michelle Bowman vice chair for supervision, succeeding Michael Barr, who remains a governor through 2026. Bowman, seen as banking-friendly, joined the Fed during Trump’s initial term. Read

Gold Soars: Gold surged to a record high after the Fed held rates steady as expected, while Powell signaled a potential 50 bps cut by year-end. Read

One More Crypto Win: Ripple announced this week that the SEC has officially dropped its four-year lawsuit, ending a prolonged standoff between the regulator and the crypto industry. Read

Google’s New Takeover: Google signed a definitive deal to acquire cloud security startup Wiz for $32B in cash. In July, Wiz had rejected a $23B offer from Google and told employees it planned to go public instead. Read

StubHub IPO: StubHub, the ticket resale platform, filed to go public on the NYSE under the ticker “STUB” on Friday. Read

The Fed Reports Loss: The Federal Reserve reported a $77.5 billion loss for 2024, down from $114.6 billion in 2023, as inflation-fighting efforts kept it in the red for a second year. It last posted a profit in 2022. Read

Source: Wall Street Journal

EARNINGS UPDATE:

Micron Beat: Micron beat fiscal Q2 estimates and issued strong guidance, with revenue up 38% YoY. CEO Sanjay Mehrotra noted data center revenue tripled YoY. Read

Nike Beat: Nike topped Wall Street’s Q3 expectations but warned Q4 sales would fall at the low end of the mid-teens range—sharply below forecasts—citing restructuring, tariffs, and weakening consumer confidence. Read

FedEx Miss: FedEx posted Q3 adjusted EPS of $4.51, up from $3.86 a year ago but below the $4.54 consensus. It cut full-year profit and revenue forecasts, citing weak demand and U.S. industrial uncertainty amid Trump-era tariffs. Read

Accenture Beat: Accenture's strong earnings were overshadowed by investor concerns over slowing U.S. government spending. The consulting firm noted that federal budget tightening is beginning to pressure revenues, marking it as an early casualty of the Trump administration’s Department of Government Efficiency push. Read

EARNINGS PREVIEW:

Date | Symbol | Name | Time |

25-Mar | MKC | Mccormick & Company | Before Open |

26-Mar | CTAS | Cintas Corp | Before Open |

26-Mar | PAYX | Paychex Inc | Before Open |

27-Mar | LULU | Lululemon Athletica | After Close |

VIDEO’s OF THE WEEK:

Written By

Vijay Jadhav

LinkedIn | Newsletter | Blog

Hands Down Some Of The Best 0% Interest Credit Cards

Pay no interest until nearly 2027 with some of the best hand-picked credit cards this year. They are perfect for anyone looking to pay down their debt, and not add to it!

Click here to see what all of the hype is about.

Please Share This Newsletter With Your Friends.

Also, check my blog here.

This newsletter's content is for informational and educational purposes only and should not be considered trading or investment recommendations. All the opinions in this newsletter are personal and do not belong to any organization.