Summary of July FOMC meeting minutes.

Jackson Hole Update: Jarome Powell hints at starting rate cuts in September.

Apple Targets Sept. 10 Debut for New iPhones, AirPods and Watches.

Nvidia to report earnings next Wednesday. Will it hit $30bn in revenue milestone?

Why Haven’t Rate Increases Slowed the Economy More?

A Helpful Federal Reserve Board Statement on Bank Liquidity.

Near record ETF inflows and new ETF launches in 2024.

QUOTE OF THE WEEK:

“AI adoption is proceeding at a rapid pace, faster than honestly I've seen any other new technology. However, it is following a typical pattern. Innovation is driving the speed of adoption while security might be an afterthought.” - Nikesh Arora, CEO, Palo Alto Networks, on the Q2 earnings call this week.

AFTER-HOURS:

Source - CNN

KEY US ECONOMIC EVENTS NEXT WEEK:

Source - Forex Factory

MARKET CLOSE:

Source - CNBC

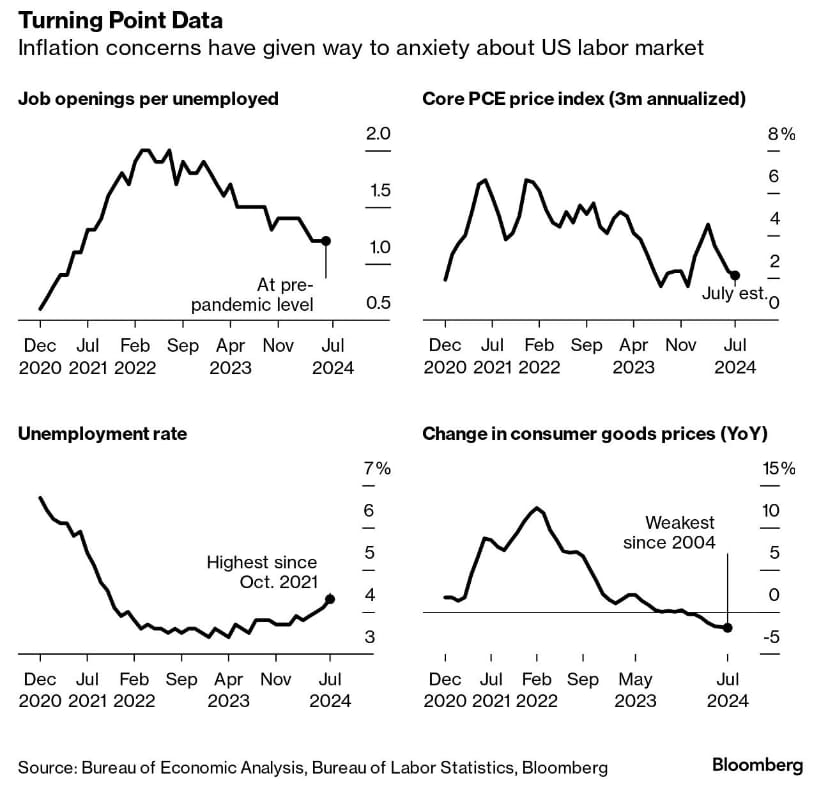

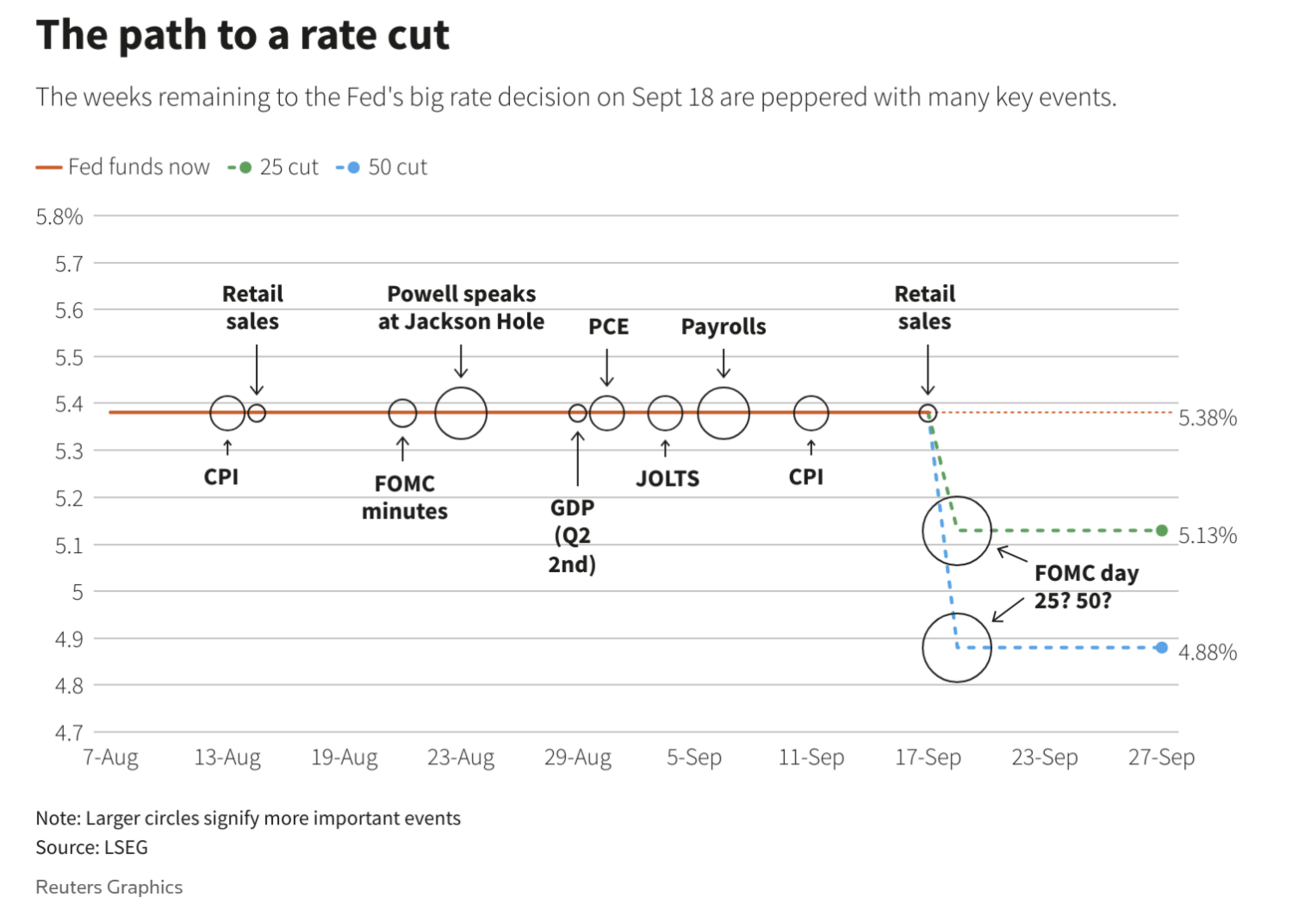

Good Afternoon. This week, the July Fed meeting minutes and Jarom Powel's Jackson Hole speech indicated that the Fed is ready to start cutting rates from the September meeting. He stated, “The time has come for policy to adjust. The direction of travel is clear, and the timing and pace of rate cuts will depend on incoming data, the evolving outlook, and the balance of risks.”

I think the Fed is slightly behind the curve. Whether it will be a 25bp or 50bp cut depends on the critical economic data, especially payroll numbers on September 6th. Check the last video in the curated videos section. Tom Lee discusses that the key to a soft landing is the Fed getting off data dependence, i.e., being more proactive, which I discussed in previous newsletters.

Source: LSEG

For the week:

The S&P 500 is up 1.45%, the Nasdaq is up 1.40%, and the Dow 30 is up 1.27%.

CNN's Fear & Greed Index moved from Fear to Neutral category and now stands at 53 out of 100, an increase of 18 points from last week.

The top five trending stocks on Reddit are Nvidia, Boeing, SPY, AST Spacemobile, and QQQ.

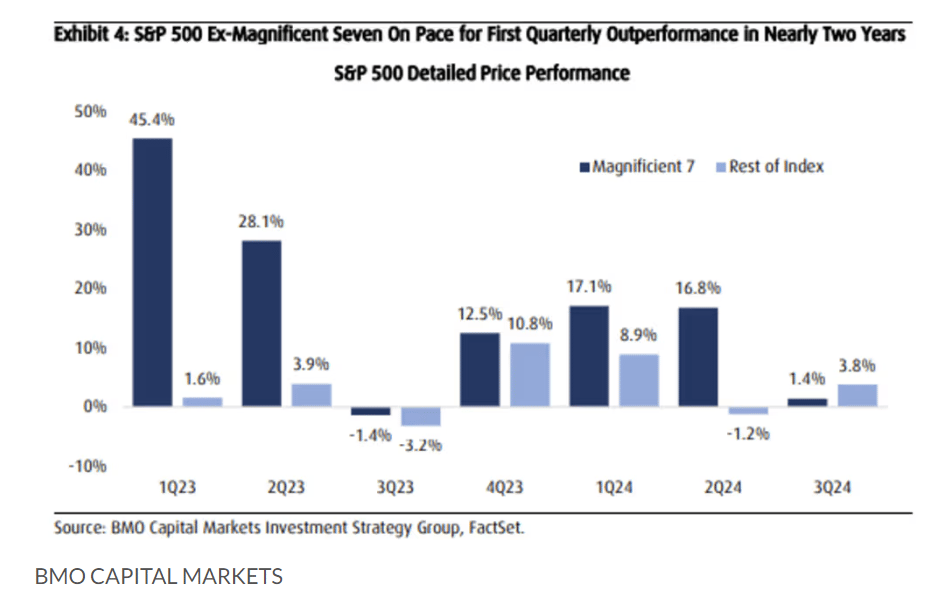

According to BMO, the S&P 493 stocks are outperforming for the first time in two years. Next week, Nvidia earnings will decide if this trend reverses and the magnificent seven stocks regain dominance in the short term.

Key points from the July FOMC meeting minutes:

The critical point in the meeting minutes was that the Participants discussed that the upside risks to inflation are diminishing while downside risks to employment have increased. The detailed summary is outlined below:Current financial conditions appeared to provide neither headwinds nor tailwinds to the growth.

Nominal treasury yields declined over the period, with shorter-term yields decreasing more than long-term yields, leading to the steepening of the yield curve.

The Q2 earnings reports received before the meeting were slightly above analysts’ expectations, although some companies noted a softening in consumer demand.

Repo rates edged higher, reflecting increased demand for financing Treasury securities. The staff projected that the ON RRP usage would decline more noticeably over the remainder of the year.

The unemployment rate for African Americans rose in June, while the rate for Hispanics declined slightly; both were above that of whites.

Corporate bond spreads are little changed and remain in the lowest decline of their respective historical distribution.

Banks’ total deposit levels increased modestly as large-time deposits displayed modest inflows.

Banks reported modestly tighter lending standards for C&I loans.

House prices remained elevated relative to the fundamentals.

Participants agreed that inflation is moving towards the 2% target with the easing of the labor markets.

Participants noted rising credit card delinquencies and an increased share of households paying minimum balances, which warranted continued monitoring.

Participants commented that the Fed should improve the operational efficiency of the discount window.

Participants judged that the Fed should continue reducing the Federal Reserve securities holdings.

Several participants noted that the leverage in the Treasury market remained a risk.

FRONT PAGES:

Fed Chair Powell indicates interest rate cuts ahead: ‘The time has come for policy to adjust.’

ECB and Bank of England officials also signal lower rates, showing that the major central banks are aligned. This marks the beginning of the end of an era of high borrowing costs as the global economy slips out of the grip of post-COVID inflation.

Apple targets Sept. 10 debut for new iPhones, AirPods, and watches.

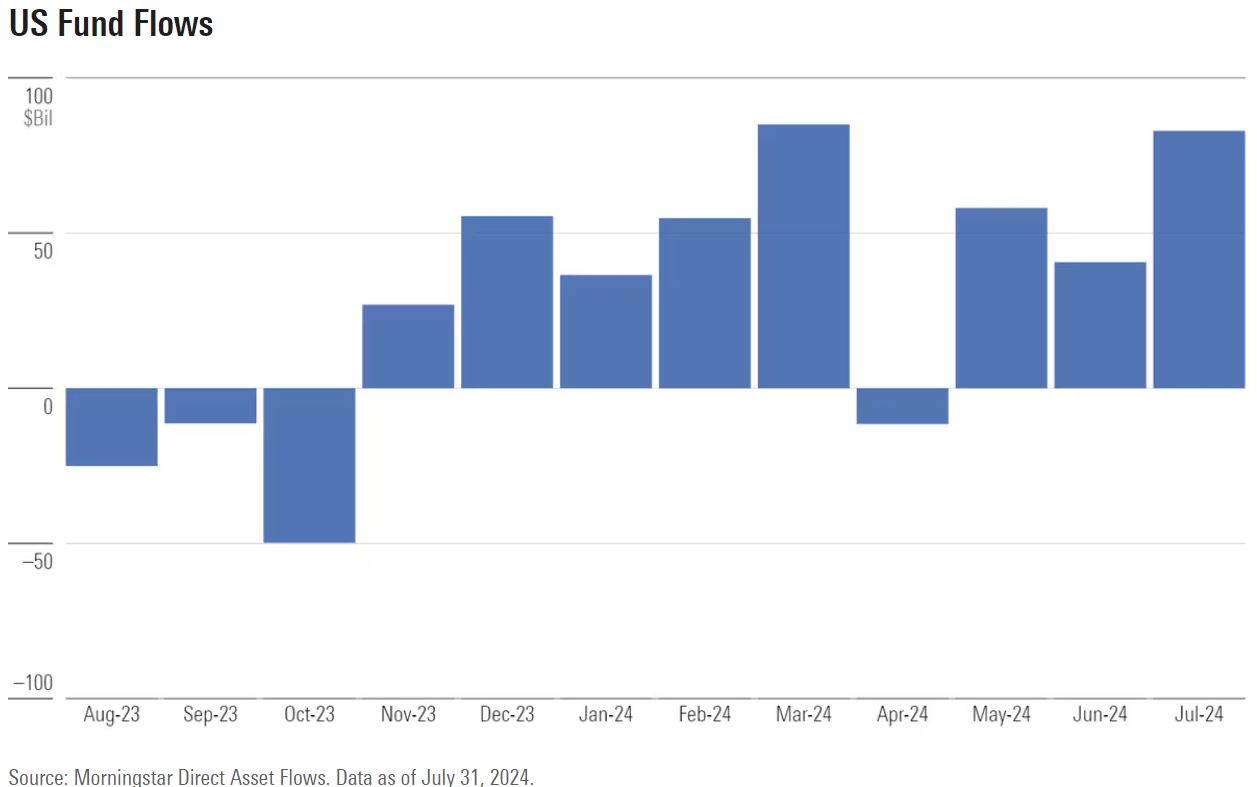

ETFs See Near-Record Inflows in July as US Fund Flows Heat Up.

According to data from Morningstar Direct, the number of new exchange-traded funds hitting the U.S. market is on track to set another record in 2024, with an average of 50 ETFs making their debut monthly.

The US Added the Most Power Generation in 21 Years as AI Demand Surged. Capacity increased by the most since 2003 in the first half of 2024.

EARNINGS UPDATE:

Palo Alto Networks posted better-than-expected revenue in its latest quarter, signaling its cybersecurity offerings remain a priority for companies despite conditions that have curtailed spending elsewhere.

Lowe’s beat fiscal second-quarter earnings expectations but missed on sales and cut its full-year outlook. The company mentioned on the conference call, “In terms of housing specifically, we're seeing significant implications due to a lock-in effect. Simply put, people aren't moving nearly as often as they typically do because current mortgage rates are so much higher than their existing rates.”

EARNINGS PREVIEW:

Date | Symbol | Name | Time |

8/26/2024 | PDD | Pdd Holdings Inc | Before Open |

8/26/2024 | BHP | Bhp Billiton Ltd ADR | After Close |

8/28/2024 | CRM | Salesforce Inc | After Close |

8/28/2024 | RY | Royal Bank of Canada | Before Open |

8/28/2024 | NVDA | Nvidia Corp | After Close |

CURATED INSIGHTS:

Nvidia Earnings:

Nvidia is scheduled to report its earnings next Wednesday, an event likely to influence market sentiment significantly. The company has consistently exceeded consensus revenue expectations for the past five years. The current consensus estimate for this quarter's revenue is $28.7 billion, although some analysts anticipate that figures could exceed $30 billion. Achieving over $30 billion in revenue would underscore Nvidia's remarkable growth trajectory and scalability, considering it first surpassed $10 billion in quarterly revenue just a year ago and $20 billion in January.

Analysts project a potential revenue quarter of $40 billion within the following year. FactSet consensus estimates forecast revenues of $39.6 billion for the July quarter next year and $42.3 billion for the October quarter.

AI-heavy firms, i.e., magnificent Seven + Broadcom, now account for 1/3rd of the S&P 500. Hence, poor Nvidia earnings will impact investors' portfolios holding broader index funds due to this concentration. This pic is perfect to reflect Nvidia’s importance 😃

Source - Barchart

On the same topic

Source - Reddit

An analysis by the Kansas City Fed discusses why the current tightening cycle has not slowed the economy. In summary, recent monetary policy tightening appears less restrictive than expected, mainly because:

Higher policy rates have not passed through to the rates paid by private firms and households.

The excess bond premiums are also surprisingly low. As the spreads did not increase during monetary policy tightening, they may not decrease as much as expected during loosening, which may require policy recalibration.

The Federal Reserve Board published an FAQ related to Reg YY, which clarified a critical question for large banks with assets worth over $100 billion. As a result, banks can now consider non-private market sources such as the Federal Reserve’s discount window, Standing Repurchase Facility (SRF), or Federal Home Loan Bank (FHLB) advances as monetization channels to demonstrate their capability to monetize highly liquid asset (HLA) securities under each internal liquidity stress test (ILST) scenario. Clarity on the ability to consider these additional monetization channels in the ILSTs will help the monetization capacity assumptions for the large banks. The requirements for an asset to qualify as HLA remain unchanged, and firms must continue to demonstrate the other Reg YY requirements to test the monetization channels in private markets. This response does not expand the scope of the assets that qualify for inclusion in a covered firm’s liquidity buffer, i.e., covered firms can only include assets that are HLA in their required liquidity buffer and cannot include assets that do not qualify as HLA even if they are prepositioned at the discount window or FHLB.

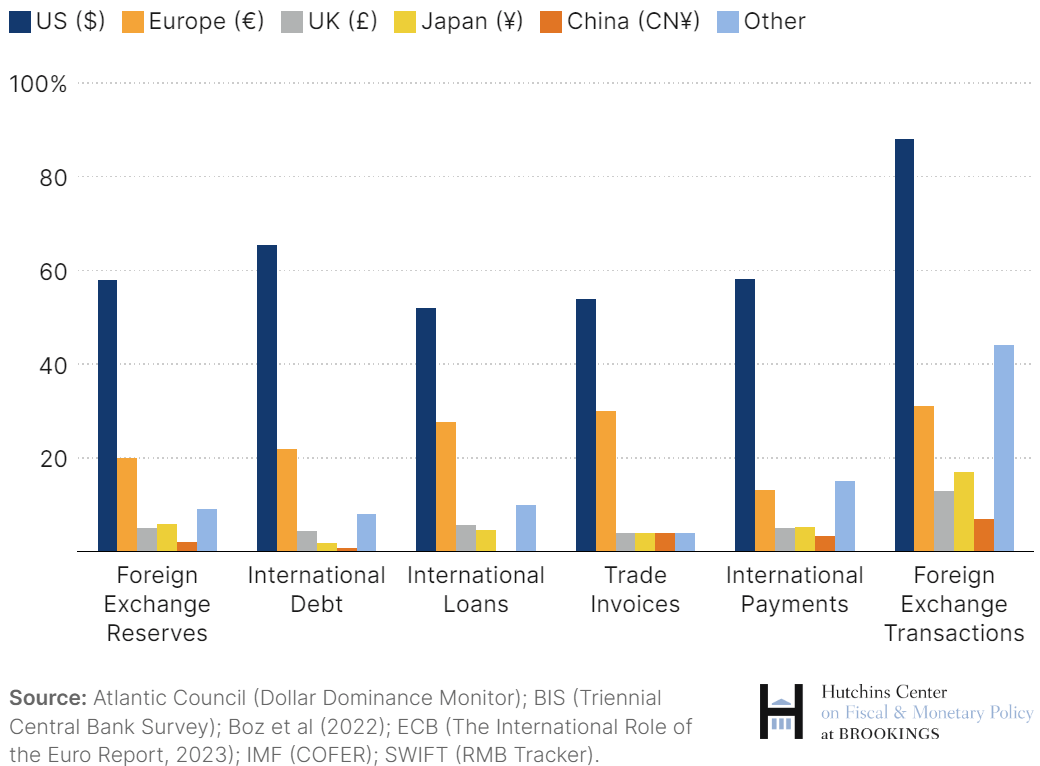

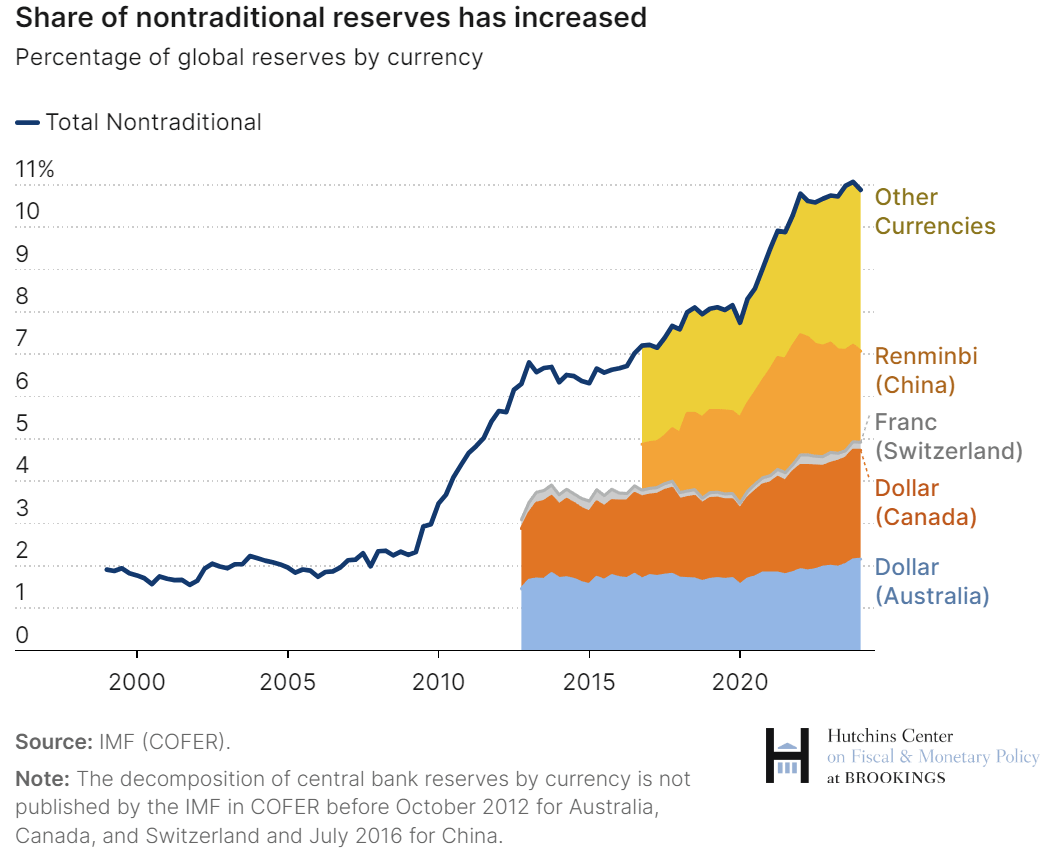

This article from The Brookings Institution, published this Friday, analyzes the changing role of the US dollar. Key points are:

The dollar's role remains strong and is still by far the world’s dominant currency.

The dollar’s share of global reserves has fallen from more than 70% in 2000 to 59% today. So, the dollar is losing some market share, but foreign reserves are not flowing to its main competitors, the euro and the yen. Instead, the reserves are going to nontraditional currencies such as the Canadian dollar, the Australian dollar, and the Chinese renminbi.

VIDEO’s OF THE WEEK:

Subscribe to the Primal Thesis Newsletter here.

Find past newsletter archives here.

This newsletter's content is for informational and educational purposes only and should not be considered trading or investment recommendations. All the opinions in this newsletter are personal and do not belong to any organization.