In partnership with

Weekly Newsletter

📊 Key Points From FOMC Press Conference

📉 Major Indices Posted A Fourth Weekly Loss

🛢️ Impact Of $100 Oil On The US Economy

🌍 US-Iran Threats Escalate

📈 PPI Rose To The Highest Level Since Feb 2025

QUOTE OF THE WEEK:

“A lot of people have been wondering, when was the Fed staff and the Fed itself, the FOMC, going to write up their productivity growth trend to recognize that it's been doing better than that old number for some time now. And they finally did it. I thought that was the one notable thing and in on the pure economics. And it does have the effect that you said, that the economy can safely grow a little bit faster than was implied by the previous forecast indefinitely. Indefinitely, that's the key thing, not just a quarter or two.” - Fmr. Fed Vice Chairman Alan Blinder

KEY US ECONOMIC EVENTS NEXT WEEK:

MARKET CLOSE:

CNBC - EOD 3/21

WEEKLY MARKET WRAP:

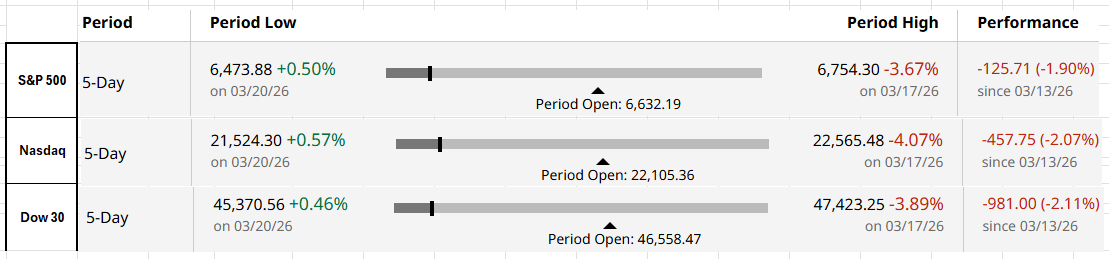

Good Afternoon. Major indices posted a fourth weekly loss amid a surge in energy prices due to escalating geopolitical tensions. As expected, the FOMC left rates unchanged, and the dot plot shows one possible rate cut in 2026.

Below are the key things to note this week:Russell 2000 Enters Correction: The index has declined >10% from its recent high, becoming the first major U.S. benchmark to enter correction territory (10–20% drawdown). Small caps are more exposed to oil price volatility and cyclical slowdown, amplifying downside risk.

S&P below 200 DMA: S&P 500 broke below its 200-day moving average on March 19 for the first time in over a year, a key technical signal with mixed historical outcomes. Past breaks have either reversed quickly or extended into deeper drawdowns; with rising geopolitical risks and volatility, near-term price action will be critical in determining direction.

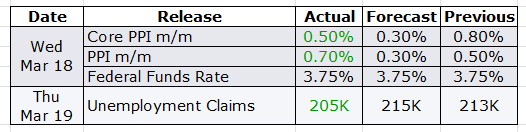

US Wholesale Inflation Hits 1-Year High, Led by Services: PPI rose 0.7% MoM (vs 0.3% est.) and 3.4% YoY (vs 2.9% est.), marking the highest level since Feb 2025, indicating elevated price pressures even before geopolitical risks intensified. Core PPI came in at 0.5% MoM (vs 0.3% est.) and 3.9% YoY (vs 3.7% est.), reflecting persistent underlying inflation.

Services drove the upside, rising 0.5% MoM—significant as tariffs typically impact goods more than services. Within this, portfolio management fees rose 1%, while brokerage, dealing, and advisory services surged 4.2%, pointing to financial services-led inflation. Goods prices also increased 1.1% MoM, adding to broad-based cost pressures.

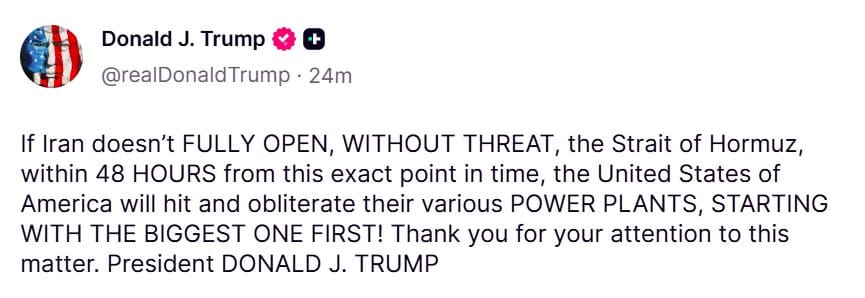

US-Iran Threats Escalate Around Hormuz and Nuclear Sites: President Trump warned of strikes on Iranian power plants if Hormuz isn’t reopened within 48 hours; Tehran threatened U.S. energy and desalination assets in response, as Iran-Israel attacks intensified near nuclear facilities, including strikes around Natanz and Israel’s main research site.

For the week:

The S&P 500 is down 1.90%, the Nasdaq is down 2.07%, and the Dow 30 is down 2.11%.

Barchart

CNN's Fear & Greed Index now stands at 15 (Extreme Fear) out of 100, down 5 points from last week. Details here

The top five trending stocks on Reddit are SPY, SMCI, Microsoft, NVIDIA, and QQQ. Read More

Liquidity:

Banking Reserves + ON RRP: Banking reserves remain at approximately $2.99 trillion. ON RRP balance remains immaterial.

Standing Repo Operations: The New York Fed’s standing repo operation (primarily reflecting SRF take-up) as of March 20th is zero.

Here is a summary of this week’s key economic releases:

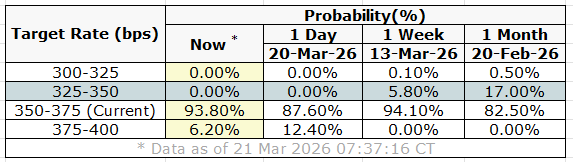

Target Rate Probabilities for April 29th FOMC Meeting:

CME FedWatch

CURATED INSIGHTS & ANALYSIS:

Key points from FOMC press conference:

The Fed held rates unchanged, stating that the current policy stance is appropriate after prior easing moves.

Economic activity remains solid, supported by resilient consumer spending and continued business investment, while housing remains weak.

The labor market is stabilizing: unemployment held at 4.4%, but job growth remains subdued, and hiring demand is soft.

Payroll data likely overstates underlying strength, with downward adjustments and weak recent trends highlighted.

Inflation remains above target, with core measures around ~3%; goods inflation is elevated due to tariffs, while services inflation continues to ease.

Tariff-driven inflation is generally viewed as a one-time price-level adjustment rather than as persistent demand-driven inflation.

Near-term inflation expectations have declined, while longer-term expectations remain anchored near 2%.

The Fed emphasized that policy is now within a broad neutral range, allowing flexibility to respond to incoming data.

Further easing will depend on clearer evidence that inflation is cooling or that labor-market conditions are weakening further.

A rate hike is not the base case, but the Fed is not ruling out any action depending on how inflation evolves.

The recent government shutdown has distorted economic data, increasing uncertainty around near-term assessments.

Powell reiterated that policy is not on a preset path and decisions will remain data-dependent.

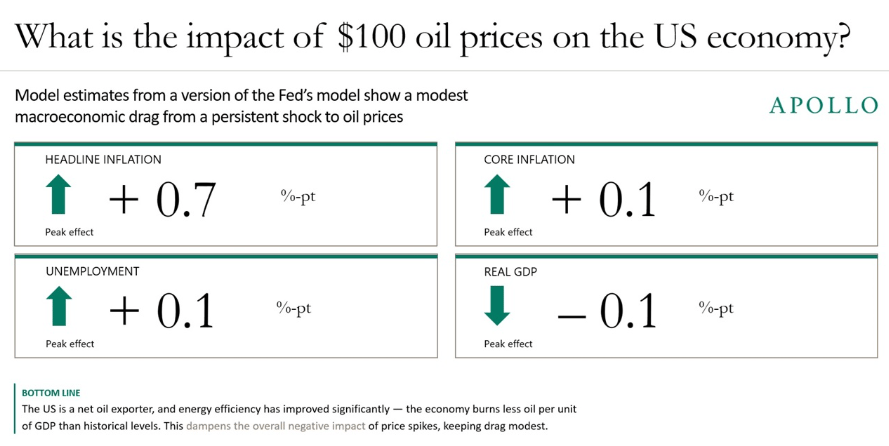

Apollo estimates for the impact of oil prices:

Detailed Blog on AI Capex Model:

I already shared the Excel file for the AI GDP estimation model I mentioned in last week’s newsletter. Posting only the blog link here again for a broader audience who may not be the subscribers -

🔗 Read the full post: primalthesis.com/ai-capex-is-justified

FRONT PAGES:

Money Market Assets Hit Record Amid Risk Aversion: Geopolitical tensions and war-related uncertainty drove investors toward safe-haven assets, pushing US money market fund assets to record levels. Elevated yields and liquidity preference accelerated inflows, reflecting risk-off positioning across markets. Read

Kalshi Doubles Valuation to $22B on Strong Growth: New funding led by Coatue values Kalshi at $22B, ~2x its $11B valuation in December, driven by rapid scale with annualized revenue reaching $1.5B. Read

US Strikes Target Iran’s Strategic Capabilities: US Central Command hit Iranian assets threatening Strait of Hormuz shipping, degrading targeting capacity, while Natanz nuclear site was also struck per IAEA; despite Trump signaling possible de-escalation, Israel indicated operations will intensify. Read

US Regulators Rework Bank Capital Rules: Fed, FDIC, and OCC move to revise Basel III proposals after industry pushback, signaling lower capital burdens and a more tailored approach for large banks. Debate highlights trade-off between financial stability safeguards and credit availability, with final rules expected to ease earlier requirements. Read

Super Micro Governance Shift: Co-founder exits board amid ongoing scrutiny, signaling internal leadership transition and potential governance reset as the company navigates operational and compliance challenges. Read

EARNINGS UPDATE:

Primal Thesis

Accenture Beat: Bookings hit $22.1B with 41 deals >$100M; revenue $18.0B (+8% YoY) at the top end of guidance. Diluted EPS rose to $2.93 (+4% YoY). Operating margin improved to 13.8% (+30 bps), with free cash flow at $3.7B and DSOs at 46 days. FY26 revenue growth guided at 3%–5% in local currency.

Micron Beat: Record Q2 FY2026 across revenue, margins, EPS, and cash flow: revenue surged to $23.86B (+196% YoY; vs $13.64B QoQ). GAAP gross margin at 74.4% and operating margin at 67.6%. Operating cash flow reached $11.90B; adjusted free cash flow $6.90B. Dividend raised 30% to $0.15/share. AI-driven demand and tight supply support potential Q3 records.

EARNINGS PREVIEW:

Date | Symbol | Name | Time |

24-Mar | GME | Gamestop Corp | After Close |

25-Mar | CTAS | Cintas Corp | -- |

25-Mar | KRMN | Karman Holdings Inc | After Close |

25-Mar | PAYX | Paychex Inc | Before Open |

25-Mar | PDD | Pdd Holdings Inc | Before Open |

26-Mar | AEG | Aegon N.V. ADR | -- |

27-Mar | CCL | Carnival Corp | Before Open |

VIDEO’s OF THE WEEK:

When it all clicks.

Why does business news feel like it’s written for people who already get it?

Morning Brew changes that.

It’s a free newsletter that breaks down what’s going on in business, finance, and tech — clearly, quickly, and with enough personality to keep things interesting. The result? You don’t just skim headlines. You actually understand what’s going on.

Try it yourself and join over 4 million professionals reading daily.

Please Share This Newsletter With Your Friends.

Also, check my blog here.

This newsletter's content is for informational and educational purposes only and should not be considered trading or investment recommendations. All the opinions in this newsletter are personal and do not belong to any organization.