In partnership with

Weekly Newsletter

🚚 Pick-Up In Demand-Driven Inflation

🛒 Consumers Frontload Shopping Before Tariffs Kick In

🚗 Auto Tariffs: Detailed Economic Impact

📊 S&P 500 Performance After 10% Corrections

💎 Undervalued Quality Stocks After the Pullback

₿ Bitcoin’s Changing Role in Investment Portfolios

QUOTE OF THE WEEK:

“Today's data was such a good example of how challenging it's going to be for the Fed to get ahead of this. When you have core PCE coming in at 0.4, when it continues to be up close to 3%, the Fed cannot move until there's a meaningful weakening of growth. And they haven't seen it yet in data, and they are not going to get ahead of this the way they hoped to before.” - Bob Elliott, Unlimited CEO

KEY US ECONOMIC EVENTS NEXT WEEK:

MARKET CLOSE:

CNBC EOD March 28th

Good Afternoon. After last week's relief, it was another bad week for the markets, mainly due to slightly hotter-than-expected PCE inflation numbers and a drop in the final University of Michigan Consumer Sentiment Index. The primary reason for higher PCE is demand-driven, i.e., consumers are front-loading their purchases in anticipation of tariffs. Considering that tariffs are slated to take effect on April 2nd, inflation should remain elevated in March, too, as the same behavior is expected from consumers. However, long-term inflation expectations (accounting for tariffs) are lower (Goldman Sachs - YoY Core PCE ~2.5% in December).

Next week is a busy week with key labor market-related macro data releases. The auto tariffs are supposed to go into effect from April 2nd. As of now, hard data is still ok and showing no signs of trouble. The survey data in recent weeks has shown weakness, but it’s essential to see if this impact is reflected in hard data. As Fed Chair Jerome Powell mentioned in the FOMC press conference recently, history has shown that people may feel one way, but their actions can be completely different. Hence, we can rely entirely on soft or survey-based data.

Below are the key things to note:

PCE Inflation:

Core PCE rose 0.4% in February, the sharpest monthly gain since January 2024, pushing the annual rate to 2.8%. The all-items index climbed 0.3% month-over-month and 2.5% year-over-year, matching expectations.The SF Fed’s supply & demand inflation series points to a modest pickup in demand-driven inflation, with supply-side factors playing a minimal role in current price pressures.

Source: SF Fed

The data from the latest PCE release below shows where this demand comes from. Durable goods spending jumped, especially in import-heavy categories like autos and furnishings, thanks to tariff fears. This is a sharp reversal from January data—check the image below. For example, motor vehicles and parts were down ~$41 billion in January, but in February, they’re up ~$13 billion.

The $87.8 billion increase in current-dollar PCE in February reflected increases of $56.3 billion in spending on goods and $31.5 billion in spending on services.

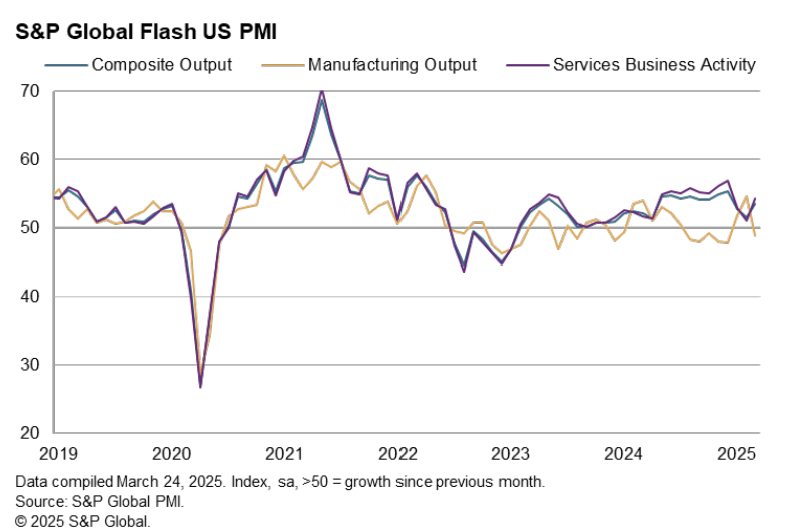

Good Flash PMI Data:

US business activity accelerated in March, driven by a strong service rebound that outweighed another drop in manufacturing output.

Reminder:

Source: Goldman Sachs

For the week:

The S&P 500 is down 1.53%, the Nasdaq is down 2.59%, and the Dow 30 is down 0.96%.

Barchart

CNN's Fear & Greed Index now stands at 22 (Extreme Fear) out of 100, down 3 points from last week. Details here

The top five trending stocks on Reddit are Tesla, SPY, EnCore Energy, Nvidia, and QQQ. Read More

Here is a summary of this week’s key economic releases:

Target Rate Probabilities for May 7th FOMC Meeting:

CME FedWatch

CURATED INSIGHTS & ANALYSIS:

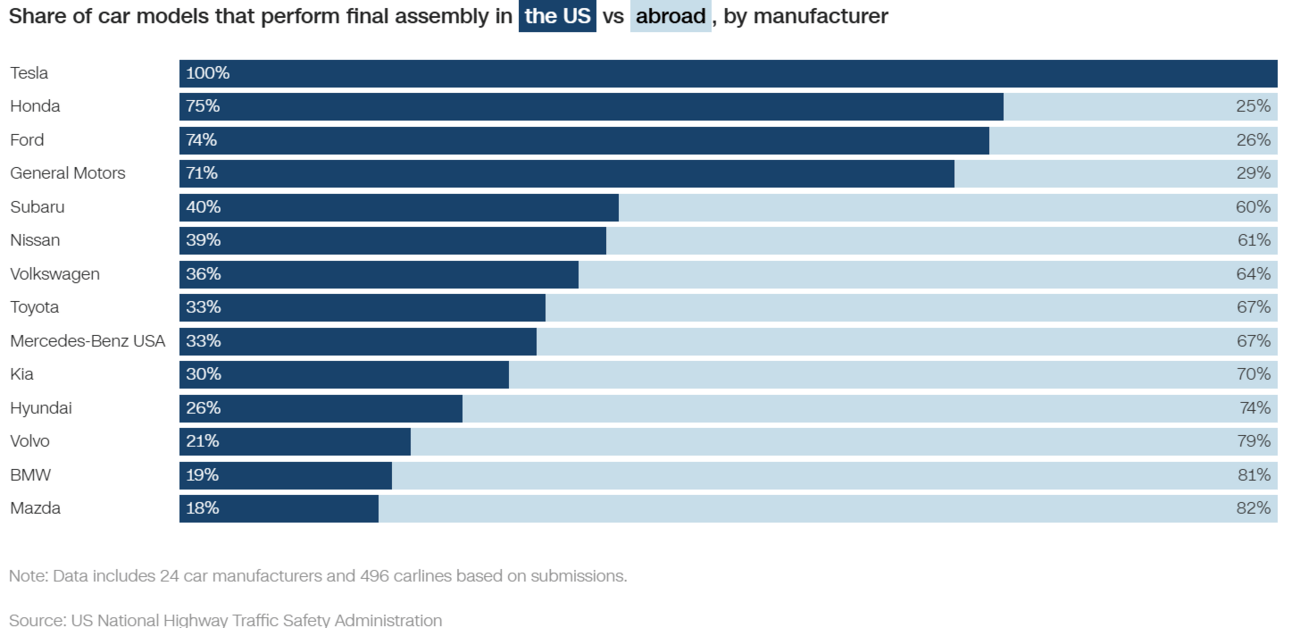

Impact of Auto Tariffs:

CNN published three charts that explain the impact of tariffs. Almost 50% of cars sold in the US may be subject to the tariffs.

Source: CNN

Below are details of manufacturers and their assembly practices:

Source: CNN

Check the detailed list of potential impacted car models: herePerformance of S&P 500 After Correction:

Source: Bloomberg, Apollo

Fallen Gems:

Below are some of my favorite stocks, down more than 25% from their 52-week high, offering a good opportunity for long-term investors to get in. Some of these had a great run before this sell-off, so they are still up significantly from their 52-week lows. For example, Palantir is down ~32% from the 52-week high, but it's still up 320%+ from its 52-week low— Shared just for analysis - no investment advice.

Source: Barchart

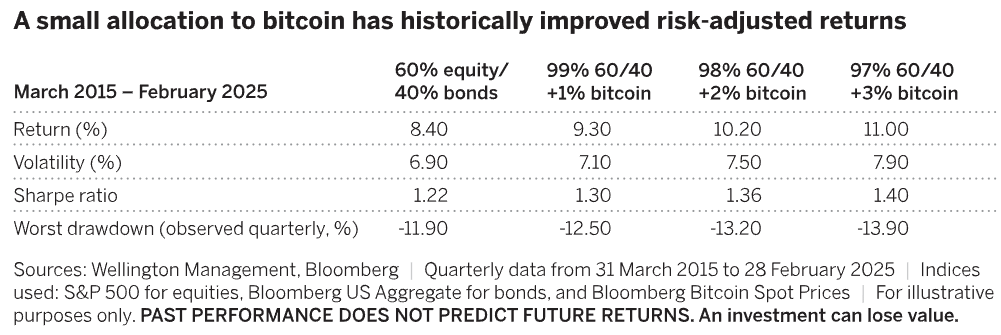

Case For Bitcoin Investing:

There is a constant flow of good news on crypto since the new administration came. I talked about bitcoin and, in general, crypto multiple times in recent weeks in this newsletter. This week, Wellington Management published an article highlighting the case of bitcoin investing. Two key points are that bitcoin volatility is decreasing, and a small allocation to bitcoin can enhance returns. Check here for details -

Source: Wellington Management

FRONT PAGES:

Auto Tariff: President Trump announced a 25% tariff on all foreign-made cars, emphasizing that U.S.-built vehicles face “absolutely no tariff.” The policy, signed via presidential proclamation, takes effect April 2, with collections starting April 3. Read

Wall Street Bonus Surge: Wall Street bonuses jumped nearly a third last year to $244,700 on average, marking the first major rise since the pandemic. The total payout pool hit a record $47.5 billion, the highest since tracking began in 1987, driven by soaring profits from trading and underwriting. Read

Source: Bloomberg

xAI-X Merger: Elon Musk announced Friday that xAI has merged with X in an all-stock deal, valuing the AI startup at $80 billion and the social media platform at $33 billion. Read

IMF Forecast: The IMF expects U.S. growth to slow this year amid Trump’s aggressive tariff push but doesn’t anticipate a recession. Read

Reg Relief For Crypto: The FDIC announced Friday that banks may engage in legally permitted activities, including those involving crypto, without prior approval—provided they manage the risks. Read

CoreWeave IPO: CoreWeave, an Nvidia-backed cloud firm, ended its first trading day flat at $40 after a $1.5B IPO priced below expectations. Shares opened at $39, swung between $37.50 and $42, and closed right at the offer price. Read

EARNINGS UPDATE:

Lululemon Beat: Lululemon topped Q4 earnings and revenue estimates but issued weaker-than-expected 2025 guidance. CEO Calvin McDonald cited a recent survey showing reduced U.S. consumer spending amid inflation worries, though shoppers responded positively to the brand's innovation. Read

Paychex Beat: Paychex beat quarterly profit estimates, driven by tight cost control despite uneven demand for human capital management services amid economic uncertainty. Read

EARNINGS PREVIEW:

Date | Symbol | Name | Time |

9-Apr | DAL | Delta Airlines | -- |

9-Apr | STZ | Constellation Brands Inc | After Close |

VIDEOS OF THE WEEK:

Pay No Interest Until Nearly 2027 AND Earn 5% Cash Back

Use a 0% intro APR card to pay off debt.

Transfer your balance and avoid interest charges.

This top card offers 0% APR into 2027 + 5% cash back!

Please Share This Newsletter With Your Friends.

Also, check my blog here.

This newsletter's content is for informational and educational purposes only and should not be considered trading or investment recommendations. All the opinions in this newsletter are personal and do not belong to any organization.