Weekly Newsletter

📉 PCE Inflation Heading In The Right Direction

📉 Post Election Enthusiasm Fades

📉 Macro Data Indicating Slowdown

📊 Forecast Of Tariff’s Impact On Inflation

⚔️ Take On Russia-Ukraine War

QUOTE OF THE WEEK:

“GDP is consumer plus investment plus government plus net exports. Well, we've had a period where fiscal spending was huge—it led to inflation, it led to some other things, but it also really helped GDP. Well, now you take the G in the equation and throw it into reverse—that also has multiplier effects, and it's starting to spook the consumer, which is the C. So, both of those can really start to weigh on the GDP even more than the net exports if they are helped by tariffs, which can be an open question.” - Steve Sosnick, Interactive Brokers chief strategist.

KEY US ECONOMIC EVENTS NEXT WEEK:

MARKET CLOSE:

CNBC EOD Feb 28th

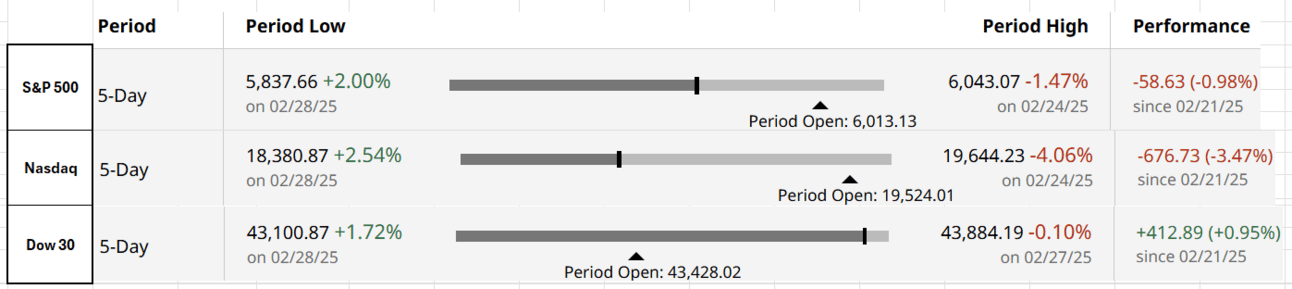

Good Afternoon. It was not a good week for markets, with two out of three leading indices closed down. The Nasdaq lost ~3.5% as the weaker economic data on unemployment claims and consumer confidence raised growth concerns. I don’t think this week’s data clearly shows any issues with the US economy. The PCE numbers especially showed that inflation is moving in the right direction. The data indicates some economic slowdown, which is expected with the restrictive Fed policy.

Inflation (PCE): The Fed’s preferred inflation gauge, the personal consumption expenditures price index, rose 0.3% in January, bringing the annual rate to 2.5%. Core PCE, which excludes food and energy, also climbed 0.3% for the month and stood at 2.6% year over year. This is in line with the FOMC forecast mentioned in the FOMC minutes. Read

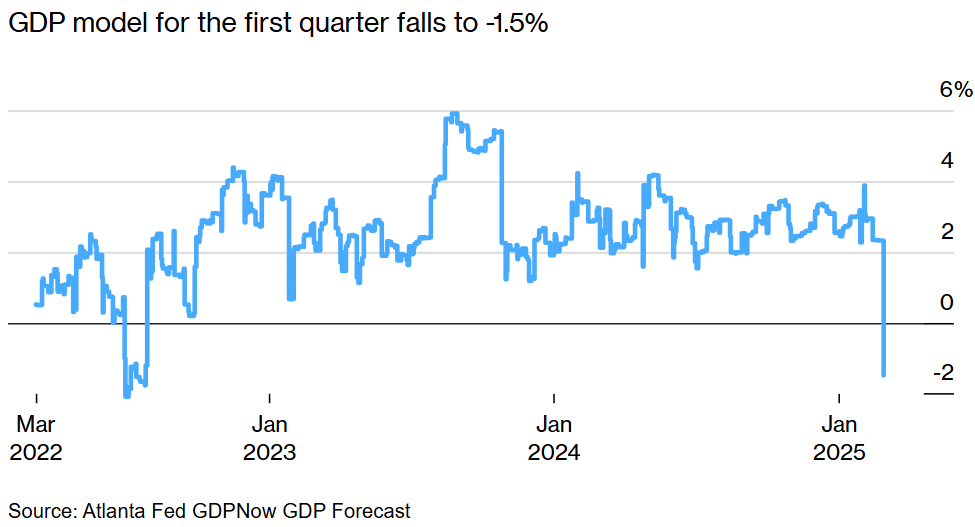

GDP Projection: The Atlanta Fed GDP model predicts a -1.5% GDP for the first quarter, but you can see below how volatile the model output is. A few days ago, this model predicted 2.3% of GDP growth. Hence, I won’t rely on a point in time, one negative number, unless this sustains for some time.

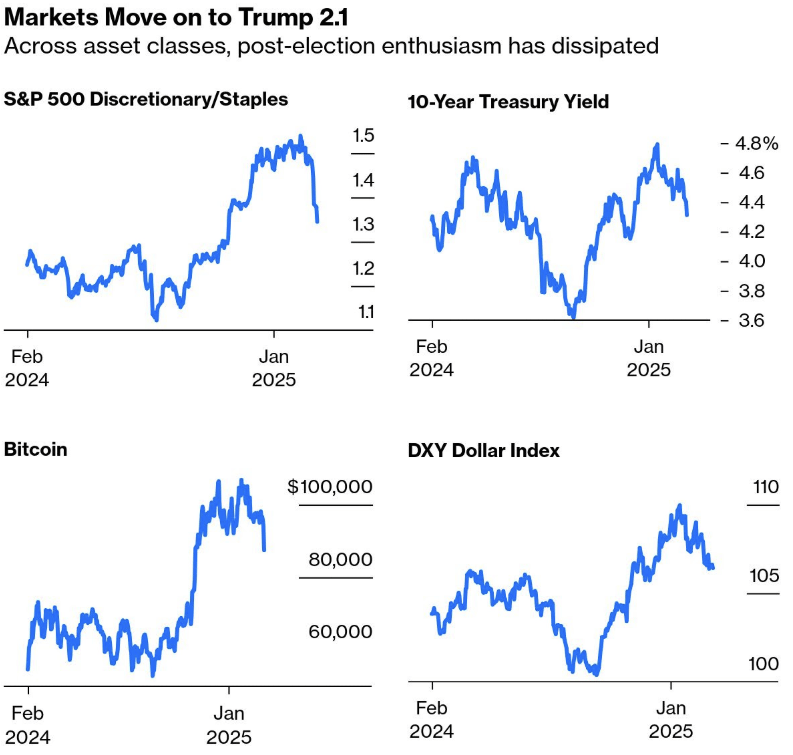

Post-Election Enthusiasm Fades: After back-to-back two good years, 2025 was expected to be volatile. There is a lot of uncertainty around new administration policies, especially around tariffs, which is making the market nervous. However, the tariffs are still uncertain, and their effect generally takes some time to reflect. I would say some healthy corrections are good for the markets. This earning season was also very strong, and with inflation moving in the right direction, this is good for the folks who do dollar cost averaging.

New Home Sales Down: New home sales fell 10.5% in January, partly due to cold weather. The median price rose 3.7% year-over-year to $446,300. Inventory reached its highest level since late 2007.

Unemployment Claims: According to Labor Department data, jobless claims rose by 22,000 to 242,000 for the week ending Feb. 22, reaching the highest level since October. Economists surveyed by Bloomberg had projected 221,000 applications.

Growth Assets Suffer: Tesla is down ~40% from the pick and close to giving up all the post-election gains. Bitcoin is also down ~30% from the pick. Mag 7’s are underperforming in 2025 compared to other sectors. As expected, the growth assets/stocks are struggling even with mostly good earnings.

Overall, there is definitely some slowdown in the economy, which is expected with the restrictive Fed policy. If this continues, the Fed will be forced to cut rates later in the year, maybe even with somewhat higher inflation. With inflation expected to decrease and rate cuts offset the slowdown, equity markets should still give decent returns for 2025. There is tariff uncertainty, but more about it is in the curated insights section. Overall, the impact of tariffs on inflation should be limited, and due to the higher base effect, inflation will eventually cool closer to the Fed target.

For the week:

The S&P 500 is down 0.98%, the Nasdaq is down 3.47%, and the Dow 30 is up 0.95%.

Source: barchart

CNN's Fear & Greed Index now stands at 20 (Extreme Fear) out of 100, down 15 points from last week. Details here

The top five trending stocks on Reddit are SPY, Nvidia, Tesla, AMD, and Weight Watchers. Read More

Here is a summary of this week’s key economic releases:

Target Rate Probabilities for Mar 19th FOMC Meeting:

CME FedWatch

CURATED INSIGHTS & ANALYSIS:

Ukraine War:

Trump and Zelensky clashed publicly this week, with many accusing Trump of mistreating him. Emotion favors Ukraine, but pragmatically, Ukraine must bend and take efforts to end the war—its only viable path forward.

I'm no foreign affairs expert, but I argued this in my blog two years ago: “Ukraine Must Surrender.” Click here to read.

In Summary:Taking Freedom for Granted: Ukraine has failed to fully appreciate its independence, showing a lack of preparedness in defending its sovereignty.

Arrogance and Complacency: The leadership has been overconfident, misjudging both Russia’s strength and the extent of Western support.

No Chance of Winning: Militarily, Ukraine cannot defeat Russia, and continuing the fight only leads to unnecessary loss and suffering.

Global Perspective: The international community has no compelling reason to prioritize Ukraine’s resistance, making surrender the most pragmatic choice.

Goldman Tariff Forecast:

This week, Goldman Sachs put out an analysis of potential tariffs and their impact on inflation. GS estimates baseline tariffs will raise the effective rate by ~4pp, adding 0.4pp to YoY core PCE, bringing it to 2.5% in December. The tariff-driven increase should fade after a year.

FRONT PAGES:

New Sports Asset Class: Morgan Stanley is launching a portfolio linked to major sports leagues, targeting high-net-worth sports fans with a $250,000 minimum investment. Over the past decade, rising valuations have solidified sports as a lucrative asset class. Read

BNY OpenAI Partnership: BNY Mellon announced a multiyear partnership with OpenAI, granting the bank access to advanced AI tools like Deep Research and its top reasoning models to enhance its internal AI platform, Eliza. Through this collaboration, OpenAI aims to assess its models’ effectiveness in handling complex real-world tasks. Read

Bitcoin Retracts: Bitcoin plunged 7.2% to $78,226 on Friday, extending its drop to 28% from its all-time high set less than six weeks ago. It later trimmed losses, closing the session nearly unchanged. Read

Relief For Robinhood: Robinhood Markets announced the SEC had closed its investigation into its crypto unit without pursuing enforcement action, reflecting the Trump administration's favorable stance on cryptocurrency. Read

Setback For FDIC: A California federal judge ruled that the FDIC must face a lawsuit over its seizure of $1.93 billion following Silicon Valley Bank’s 2023 collapse. Read

Skype Retired: Microsoft will retire its 21-year-old messaging service in May. After rapid growth in the 2000s, Microsoft acquired it in 2011, but it faded in the smartphone era. Read

EARNINGS UPDATE:

Nvidia Beat: Nvidia’s fourth-quarter earnings exceeded Wall Street expectations. Quarterly revenue surged 78%, while full-year revenue climbed 114% to $130.5 billion. The company projected first-quarter revenue of approximately $43 billion, ±2%, surpassing LSEG’s $41.78 billion estimate. Read

Home Depot Beat: HD slightly exceeded Wall Street’s Q4 earnings estimates, breaking an eight-quarter streak of declining comparable sales. The retailer continues to navigate pressure from high interest rates and home prices, which have weighed on both Home Depot and Lowe’s. Read

Salesforce Miss: Salesforce reported quarterly revenue below expectations and issued a forecast that missed analysts' estimates. Read

Lowes Beat: Lowe’s surpassed Wall Street’s Q4 earnings and revenue forecasts, projecting an end to its sales decline this year. Its strong results follow Home Depot’s first positive comparable sales in nine quarters. Elevated borrowing and housing costs have dampened home improvement demand. Read

TJX Beat: TJ Max's parent company reported a strong holiday quarter, surpassing expectations as higher customer transactions drove growth. This signals continued market share gains from department stores and discounters as budget-conscious shoppers seek deals. Read

EARNINGS PREVIEW:

Date | Symbol | Name | Time |

4-Mar | AZO | Autozone | Before Open |

4-Mar | CRWD | Crowdstrike Holdings Inc | After Close |

4-Mar | SE | Sea Ltd ADR | Before Open |

4-Mar | TGT | Target Corp | Before Open |

5-Mar | MRVL | Marvell Technology Inc | After Close |

6-Mar | AVGO | Broadcom Ltd | After Close |

6-Mar | CNQ | Canadian Natural Resources | Before Open |

6-Mar | COST | Costco Wholesale | After Close |

6-Mar | JD | Jd.com Inc ADR | Before Open |

10-Mar | ORCL | Oracle Corp | -- |

VIDEO’s OF THE WEEK:

Everyday investors net +$60M in proceeds from the sale of exclusive assets

From CEOs to shop owners, investors in Masterworks’ art offerings have received more than +$60,000,000 in total net proceeds to date (including principal) across their 23 exits.*

Surprised that so many people are interested in art investing? Bank of America recently found 83% of wealthy American investors 43 and under already collect, or want to. Normally, only the top 1% of investors would be able to diversify with art like Picassos and Banksys. But with Masterworks, you can easily diversify into this asset class without needing millions, or art expertise.

With a team that’s been working since 2019, Masterworks investors have realized representative annualized net returns like +17.6%, +17.8%, and +21.5% (among assets held for longer than one year).

Past performance not indicative of future returns. Investing Involves Risk. See Important Disclosures at masterworks.com/cd.

Please Share This Newsletter With Your Friends.

Also, check my blog here.

This newsletter's content is for informational and educational purposes only and should not be considered trading or investment recommendations. All the opinions in this newsletter are personal and do not belong to any organization.