Weekly Newsletter

📌 Key Points From FOMC Minutes

🥇 Gold And Silver Record Best Year Since 1979

💵 Best Year For Treasuries Since 2020

📉 Worst Performance Of The Dollar In 8 Years

⏳ Year-End Funding Pressure

🏦 Big Central Banks Signal Rate-Cut Cycle Is Ending

QUOTE OF THE WEEK:

“The resilience in earnings is related to the fact that companies know what they're doing — they're using technology and increasing their usage of AI. When we talk to people in leadership across industries — whether it's healthcare, private equity, or finance — everyone is using AI as it exists today, with the likelihood that they will continue to do so.” - John Stoltzfus, chief investment strategist at Oppenheimer Asset Management

KEY US ECONOMIC EVENTS NEXT WEEK:

MARKET CLOSE:

CNBC - EOD 1/2/2025

WEEKLY MARKET WRAP:

Good Afternoon. Happy New Year! A negative week for the markets, with no major macroeconomic news aside from the FOMC meeting minutes, which were released on Wednesday. The S&P 500 and Dow Jones Industrial Average closed higher on the first trading day of the year, while the Nasdaq was flat.

Below are the key things to note this week:Mortgage rates hit their lowest level in a year: Freddie Mac’s latest Primary Mortgage Market Survey shows the average 30-year fixed mortgage rate edged down to 6.15% from 6.18% last week. The benchmark rate began the year near 7%, highlighting a meaningful easing in borrowing costs.

Key point for 2025: Despite significant concerns throughout the year about US policy uncertainty and tariff impacts, US assets remain in high demand. There is a lot of talk, but when it comes to putting money to work, the US is where global investors come.

Apollo

For the week:

The S&P 500 is down 1.06%, the Nasdaq is down 1.60%, and the Dow 30 is down 0.72%.

Barchart

CNN's Fear & Greed Index now stands at 45 (Neutral) out of 100, down 11 points from last week. Details here

The top five trending stocks on Reddit are SPY, Tesla, Micron, Nvidia, and Amazon. Read More

Liquidity:

Banking Reserves + ON RRP: Banking reserves remain at approximately $2.8 trillion. ON RRP balance remains immaterial.

Standing Repo Operations: The New York Fed’s standing repo operations (primarily reflecting SRF take-up) saw increased usage on Wednesday, as eligible financial institutions tapped the facility to manage balance sheet and funding needs on the final trading day of 2025. On 12/31, usage was ~$74bn; it has since dropped to ~$23bn.

Here is a summary of this week’s key economic releases:

Initial jobless claims fell, signaling layoffs remain contained even as labor-market momentum cools. Claims for the week ending Dec. 27 declined by 16,000 to 199,000 from 215,000, undershooting the 208,000 consensus estimate, according to the Labor Department.

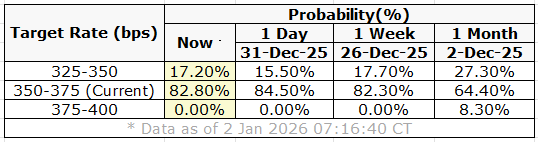

Target Rate Probabilities for Jan 28th FOMC Meeting:

CME FedWatch

CURATED INSIGHTS & ANALYSIS:

Key points from FOMC meeting minutes:

Three members dissented from the decision to cut rates by 25 bps. Two members voted to keep rates unchanged, citing insufficient progress toward the 2% inflation objective and concerns that easing could risk higher long-term inflation expectations. One member voted for a 50 bps cut, arguing that downside risks to employment had increased and warranted a faster move toward a more neutral policy stance.The Committee cut rates by 25 bps to 3½–3¾%, citing rising downside risks to employment even as inflation remained above target.

Inflation stayed elevated at 2.8% PCE, with tariffs pushing up core goods prices while housing and some services inflation cooled.

Most participants viewed tariff effects as temporary, though uncertainty remains about the timing and degree of pass-through; inflation risks remain tilted to the upside.

Labor market conditions continued to cool gradually—unemployment rose to 4.4%, hiring stayed subdued, and job gains slowed; employment risks are skewed to the downside.

Real private domestic final purchases (PDFP) grew faster than GDP over much of 2025, signaling firmer underlying demand despite slower growth versus last year.

Consumer spending remained solid but increasingly driven by higher-income households, while lower-income households showed rising price sensitivity.

Business investment remained strong, driven by technology and AI-related capital expenditure; housing and agriculture remained under pressure.

Money-market conditions tightened: repo rates rose, EFFR climbed faster than in prior QT episodes, ON RRP usage stayed low, and SRF usage increased.

Reserve balances were judged to be within an ample range, prompting the Fed to initiate reserve-management purchases, primarily Treasury bills.

The Fed removed the aggregate cap on standing repo operations to reinforce interest-rate control and market functioning.

Balance-sheet actions were emphasized as technical tools, not a signal about the stance of monetary policy.

Policy remains data-dependent, with no preset path, as the Fed balances persistent inflation risks against a softening labor market.

FRONT PAGES:

Record Gains for Gold and Silver in 2025: Gold and silver opened the year steady after their strongest annual gains since 1979, as markets weighed an upcoming benchmark commodity index reweighting. While further U.S. rate cuts and a weaker dollar could support prices in 2026, near-term pressure may emerge from index rebalancing. Record gold prices, central bank buying, easier Fed policy, and dollar weakness drove last year’s surge. Read

Best Year Since 2020 for Treasuries: The Treasury market in 2025 delivered its strongest performance since 2020, as shifts in US trade policy slowed economic activity and prompted the Fed to cut rates amid a weakening labor market. Yields fell most at the front end, while the 30-year edged higher on expectations of further cuts in 2026. For 2026, Wall Street strategists broadly expect yields to remain stable or rise as the easing cycle ends. Read

Big central banks signal rate-cut cycle is ending: Major central banks are pivoting. The Bank of Japan raised rates to a 30-year high, the ECB signaled an end to easing, and the Bank of England cut rates on a narrow vote, with dissenters warning that inflation risks persist. Read

Reuters

Worst Year for Dollar in 8 Years: The dollar closed 2025 with its steepest annual decline in eight years, and investors expect further weakness if the next Fed chair delivers deeper-than-expected rate cuts. The Bloomberg Dollar Spot Index fell ~8% this year, with markets already pricing at least two rate cuts next year. Read

Tesla Miss Deliveries: Tesla said a company-compiled consensus posted on Dec. 29 showed analysts expecting deliveries to fall 15% year over year to 422,850 vehicles. Q4 2025 deliveries declined about 16% versus Q4 2024, when the company reported 495,570 vehicles, while production fell 5.5% year over year from 459,445. For the full year, deliveries fell 8.6% to 1.64 million, down from 1.79 million in 2024. Read

EARNINGS UPDATE:

No major earnings reported this week.

EARNINGS PREVIEW:

No major earnings are scheduled for the next week

VIDEO’s OF THE WEEK:

Please Share This Newsletter With Your Friends.

Also, check my blog here.

This newsletter's content is for informational and educational purposes only and should not be considered trading or investment recommendations. All the opinions in this newsletter are personal and do not belong to any organization.