In partnership with

Weekly Newsletter

📌 Key Points From The FOMC Press Conference

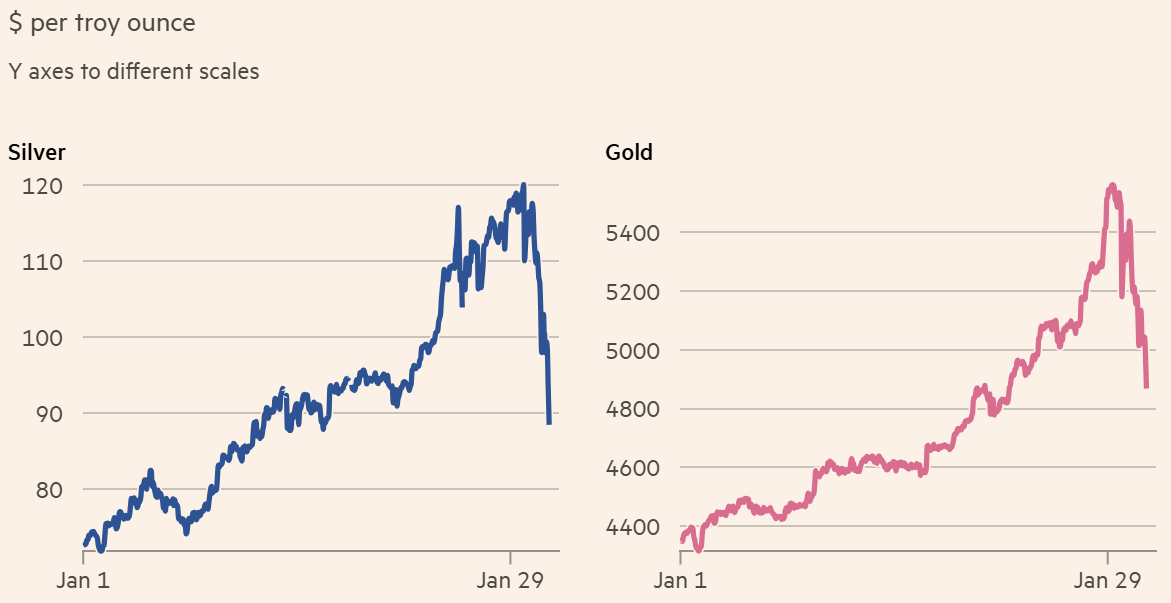

🟡 Gold, Silver, And Bitcoin Correct

🏛️ Trump Announces New Fed Chair

📊 Rising Income And Wealth Inequality

🤖 OpenAI Aiming For New Funding

💻 Key Takeaways From Tech Earnings

QUOTE OF THE WEEK:

“If you buy a business that has real incumbency and they can transform to become more efficient using AI, they can end up being a winner. So I think awareness around disruption, awareness of change, is so important. I do think it's one of the competitive advantages in the US. I think the adoption here is going to happen quicker than the rest of the world.” - Jon Gray, Blackstone President and COO

KEY US ECONOMIC EVENTS NEXT WEEK:

MARKET CLOSE:

CNBC EOD 1/30

WEEKLY MARKET WRAP:

Good Afternoon. A volatile week for the markets, but all major indices closed almost flat. Metals, i.e., Gold and Silver, experienced wild swings and corrections from elevated levels as markets digest the appointment of the new Fed chair and ongoing news flow on tech earnings and AI-related investment concerns. Bitcoin fell to its lowest levels since April 2025.

Below are the key things to note this week:

FOMC Decision: The Fed left rates unchanged as expected. Steven Miran and Chris Wallar dissented, favoring rate cuts. More on this in curated insights.

Tech earnings and uneven market reaction:

Mag Seven's earnings underscored how unevenly AI investments are being monetized. Microsoft was repriced as the market questioned near-term returns at the application layer, despite owning the most vertically integrated AI stack across GPUs, models, cloud, and Copilot. Capex scale is no longer the differentiator—revenue conversion is. Meta, by contrast, was rewarded as AI continues to directly translate into higher engagement and ad efficiency, driving upside even before generative AI meaningfully contributes. The market is signaling that clear cash flow visibility matters more than AI ambition.Apple’s results reinforced its positioning as a demand-driven hardware franchise rather than an AI story. Strong iPhone momentum carried the quarter, but rising memory costs introduced a new trade-off between margins and pricing power. Tesla continued its pivot away from autos toward robotics, autonomy, and physical AI, increasingly valued as a long-duration optionality play. The key inflection remains execution—visible, paid robotaxi adoption at scale. Until that materializes, valuation rests more on belief than fundamentals.

Trump announces new Fed chair: President Donald Trump named Kevin Warsh to succeed Jerome Powell as Federal Reserve chair.

Gold and Silver Correct:

Gold, after surging to nearly $5,600 on Thursday, fell as much as 11% on Friday to around $4,800 per ounce, extending a sharp reversal after a record run driven by safe-haven demand amid global turmoil and inflation fears. The selloff spilled across precious metals, with silver posting a record 26% one-day drop and platinum sliding 18%.

Financial Times

OpenAI attracting investments:OpenAI is assembling a mega funding round (up to ~$100bn) to finance AI compute, data centers, and long-term scale

The widely cited $100bn Nvidia deal was non-binding and is now on pause, as structure, sizing, and capital intensity are reassessed

NVIDIA has not walked away — management reiterated plans for a large OpenAI investment, but within a broader multi-investor round, not a standalone pact

Capital is shifting from a single bilateral deal to multi-partner “capital stacking”, reducing execution risk and spreading infrastructure burden

Amazon is in talks to invest up to ~$50bn, signaling hyperscaler competition to anchor AI workloads and future cloud rents

SoftBank is discussing up to ~$30bn more, doubling down on AI as a capital-intensive supercycle

Microsoft remains a strategic backer, though expected to contribute less incremental capital than Amazon or SoftBank

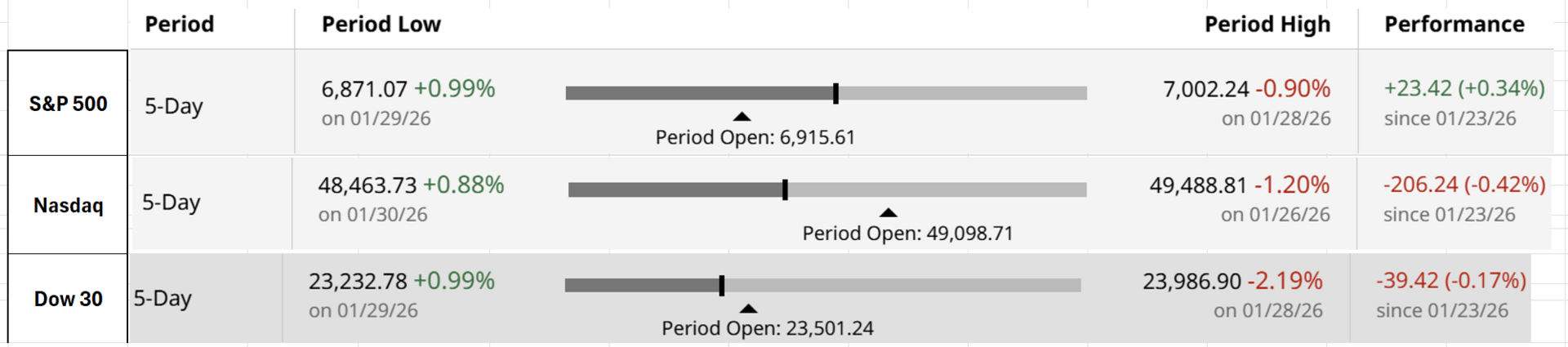

For the week:

The S&P 500 is up 0.34%, the Nasdaq is down 0.42%, and the Dow 30 is down 0.17%.

Barchart

CNN's Fear & Greed Index now stands at 58 (Greed) out of 100, up 6 points from last week. Details here

The top five trending stocks on Reddit are SLV, Scandisk, GLD, SPY, and Microsoft. Read More

Liquidity:

Banking Reserves + ON RRP: Banking reserves remain at approximately $2.9 trillion. ON RRP balance remains immaterial.

Standing Repo Operations: The SRF balance as of Dec 12 is almost zero.

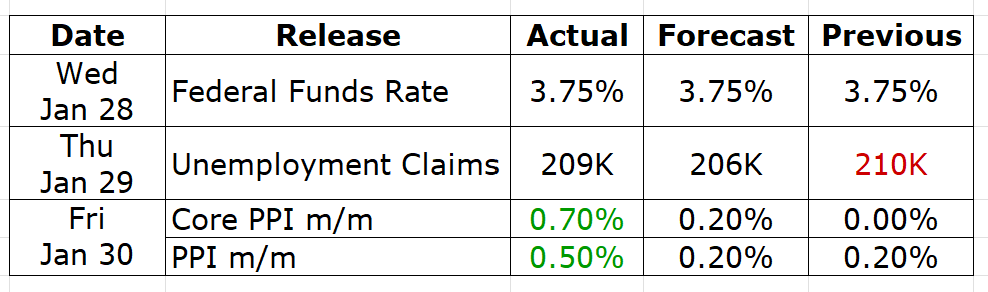

Here is a summary of this week’s key economic releases:

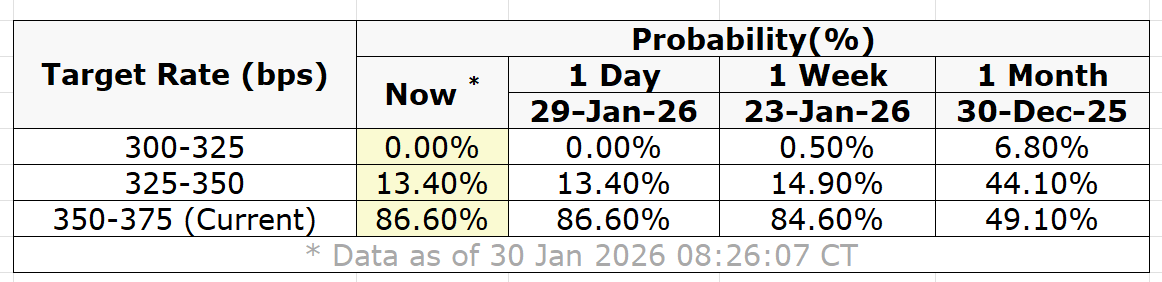

Target Rate Probabilities for March 18th FOMC Meeting:

CME FedWatch

CURATED INSIGHTS & ANALYSIS:

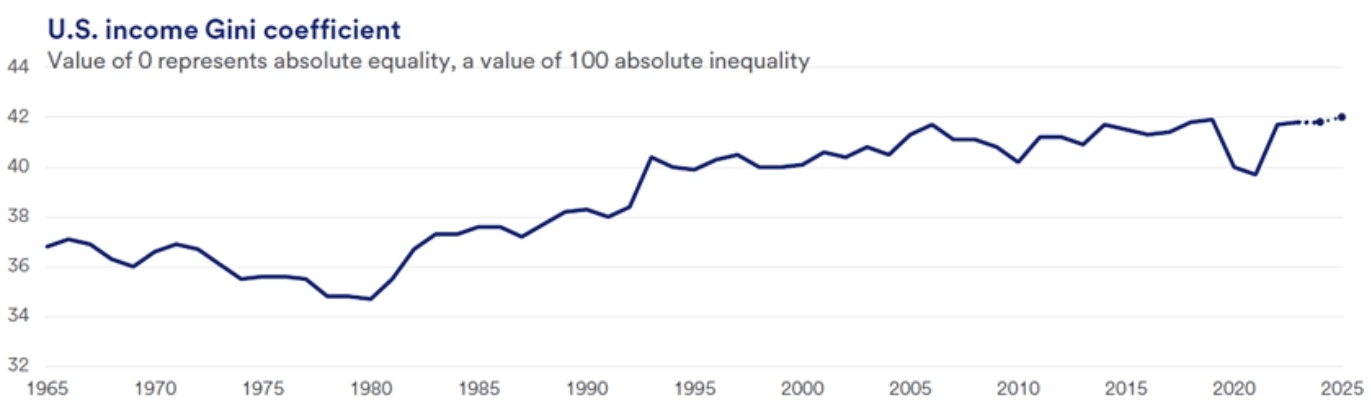

Rising Wealth and Income Inequality:

U.S. Bank recently published a report highlighting rising wealth and income inequality in the U.S. I have written about this before, and it's not just a U.S. issue but a global one.

U.S. Bank

The U.S. remains firmly K-shaped, with higher-income households benefiting from asset appreciation, technology, and capital income, while lower-income households face wage pressure, higher debt stress, and inflation erosion.

Pandemic-era stimulus briefly reduced inequality, pushing income concentration to its lowest level since the early 1990s, but the effect reversed quickly once fiscal support faded, and asset markets surged.

Income concentration is now near 60-year highs, with the Gini coefficient estimated around 42 in 2025, driven by capital gains, higher rates, and regressive policy effects.

Between 2019 and 2021, pre-tax income rose ~19% for the top quintile, largely from capital gains, while income for the lowest quintile fell ~11%, underscoring the role of asset ownership.

Wealth inequality is more extreme than income inequality: the top 10% hold ~60% of U.S. wealth, the top 1% ~27%, while the bottom half owns ~6%, with intergenerational transfers reinforcing this pattern.

Higher interest rates, tariffs, and recent tax policy disproportionately hit credit-sensitive households and small firms, with estimates showing the bottom 10% losing ~7% of income versus gains for top earners.

Wage growth for lower-paid workers now trails higher earners for the first time in over a decade, while delinquency rates are rising fastest among younger and lower-income households.

Aggregate consumption remains resilient due to wealthy households, but demand is increasingly fragile, with higher exposure to asset-market shocks.

AI and automation are key amplifiers: without broad adoption, they risk hardening the K by rewarding specialized skills and capital-intensive firms.

Policy focus matters: digital literacy, workforce upskilling, asset-building, and housing access could turn innovation into an equalizer; failure to do so risks weaker, less durable growth.

Key points from FOMC press conference:

The Fed held rates unchanged after 75 bps of cuts over the prior three meetings, judging the current stance appropriate for the dual mandate.

Economic growth remains solid entering 2026; consumer spending and business investment are resilient, while housing remains weak.

The government shutdown likely weighed on Q4 activity, with reopening expected to boost growth this quarter.

Labor market conditions appear to be stabilizing: unemployment held at 4.4%, but job gains remain low.

Payroll growth slowed sharply, reflecting weaker labor force growth from lower immigration and participation, alongside softer labor demand.

Inflation remains above target, with PCE inflation at 2.9% and core PCE at 3.0% over the past year.

Goods inflation is being driven largely by tariffs, while services disinflation continues.

Near-term inflation expectations have declined; longer-term expectations remain anchored near 2%.

The policy is within a plausible neutral range; further adjustments will depend on incoming data and the risk balance.

Tariff-driven inflation is viewed as a one-time price-level effect; further easing would require clearer evidence of cooling inflation or renewed labor-market weakness.

FRONT PAGES:

New Fed Chair: President Donald Trump named Kevin Warsh to succeed Jerome Powell as Federal Reserve chair, marking the end of a long and turbulent chapter for the central bank. The decision follows a process that formally began last summer but traces back to Trump’s sustained criticism of the Powell-led Fed since Powell assumed the role in 2018. Read

NVIDIA-OpenAI Pause $100bn deal: Nvidia’s plan to invest up to $100 billion in OpenAI to support training and deployment of next-gen AI models has stalled, after internal concerns emerged at the chipmaker, according to people familiar with the matter. The agreement, unveiled last September, included a memorandum under which Nvidia would build at least 10 gigawatts of compute for OpenAI, with OpenAI leasing the chips as part of the arrangement. Read

Potential Merger: Elon Musk’s SpaceX and AI startup xAI are planning to merge into a single company, further consolidating Musk’s business empire, according to people familiar with the matter. SpaceX executives have begun informing select investors about the proposed tie-up. Read

OpenAI funding round: OpenAI is in discussions to raise nearly $40bn from Nvidia, Microsoft, and Amazon as part of a landmark $100bn funding round. NVIDIA may commit up to $20bn, Amazon has explored an investment of $10bn or more, and Microsoft, which already owns a 27% stake, could add several billion dollars. Read

Metal Sold off: Gold and silver sold off sharply on Friday after reports that President Donald Trump selected Kevin Warsh to replace Jerome Powell as Fed chair. Gold futures suffered their worst one-day drop on record, settling at $4,745, down 11%. Silver plunged 31% to $78.53, its steepest same-day fall since March 1980. Read

EARNINGS UPDATE:

Primal Thesis

Apple Beat: Record highs in total revenue and EPS. iPhone delivered its strongest quarter ever, with records across every geography. Services revenue hit an all-time high, growing 14% year over year. Operating cash flow approached $54B, with roughly $32B returned to shareholders. The installed base crossed 2.5B active devices. The board declared a $0.26 per share cash dividend.

RTX Beat: Q4 sales reached $24.2B, up 12% year over year and 14% organically. Adjusted EPS was $1.55, up 1% year over year, with GAAP EPS of $1.19. Operating cash flow totaled $4.2B and free cash flow $3.2B. Backlog stood at $268B, led by $161B in Commercial and $107B in Defense. Pratt & Whitney sales rose 25%, Raytheon 7%, and Collins 3%. The company completed the divestiture of Collins’ Simmonds Precision Products business.

UnitedHealthcare Mixed: FY2025 revenue reached $447.6B, up 12% YoY, with operating cash flow of $19.7B. Q4 revenue was $113.2B; GAAP EPS came in at $0.01 and adjusted EPS at $2.11, excluding a $2.8B pre-tax charge related to cyber issues, divestitures, and restructuring. For 2026, management guides to revenue above $439B, operating earnings over $24B, and an operating margin of near 5.5%. UnitedHealthcare delivered $344.9B in revenue (+16%), while Optum generated $270.6B (+7%).

Lam Research Beat: Revenue was $5.34B with non-GAAP EPS of $1.27 and GAAP EPS of $1.26. Cash and equivalents declined to $6.2B from $6.7B last quarter, while deferred revenue fell sequentially to $2.25B from $2.77B. Revenue mix was China 35%, Taiwan 20%, and Korea 20%. Systems revenue totaled $3.36B, and customer support-related revenue totaled $1.99B. The company returned $1.47B through share repurchases and paid a $0.26 per share dividend.

Meta Beat: Q4 revenue reached $59.9B, up 24% YoY, with diluted EPS of $8.88 versus $8.02 last year. Advertising strength drove results, with ad impressions up 18% YoY and average pricing up 6%. Free cash flow totaled $14.1B in Q4, operating cash flow was $36.2B, cash and marketable securities stood at $81.6B, while Reality Labs posted a $6.0B operating loss.

Microsoft Beat: Microsoft Cloud revenue topped $50B, driven by Azure and cloud services up 39% YoY. Total revenue reached $81.3B, up 17% GAAP and 15% in constant currency. GAAP net income surged 60% to $38.5B; non-GAAP rose 23% to $30.9B. More Personal Computing fell 3%, with Xbox content down 5%. The company returned $12.7B to shareholders, up 32% YoY.

Tesla Mixed: Quarterly revenue reached $24.9B with operating margins of 5.7%. Energy storage posted record deployments, driving segment gross profit to roughly $1.1B. APAC achieved a record quarter for vehicle deliveries. Driverless Robotaxi testing began in Austin in December, and safety monitors were removed starting in January. AI training capacity continues to scale with the Cortex 2 buildout in Texas.

Apple Beat: The company delivered record revenue and EPS. iPhone had its strongest quarter ever, setting records across all regions. Services revenue hit a new high, growing 14% year over year. Operating cash flow was nearly $54B, of which about $32B was returned to shareholders. The installed base crossed 2.5B active devices, and the board declared a $0.26 per-share cash dividend.

Caterpillar Beat: Delivered record quarterly sales with Q4 revenue up 18% YoY to $19.13B. Q4 GAAP EPS was $5.12 and adjusted EPS was $5.16, slightly above last year. Operating margin declined to 13.9% (15.6% adjusted) from 18.0% (18.3%) due to tariffs and restructuring, with operating profit at $2.66B. Returned $7.9B via buybacks and dividends in 2025, ending the year with $10.0B in cash and $11.7B in operating cash flow.

Mastercard Beat: Adjusted EPS of $4.76 beat estimates by $0.43, while revenue of $8.80B exceeded expectations by $512M. Value-added services and solutions grew 26% in Q4, with GAAP operating margin expanding 320 bps to 55.8%. Card issuance reached 3.7B, and Q4 capital return totaled $4.3B through buybacks and dividends.

Thermofisher Beat: Q4 revenue rose 7% YoY to $12.21B, with organic growth of 3%. GAAP diluted EPS increased 9% to $5.21, while adjusted EPS grew 8% to $6.57. GAAP operating margin expanded 80 bps to 18.5%, though adjusted margin eased 30 bps to 23.6%. The company announced a strategic collaboration with OpenAI to scale AI across operations and products, alongside major launches including Orbitrap Astral Zoom, Krios 5 Cryo-TEM, and Helios MX1. Capital deployment for 2025 is ~$16.5B, with $13B committed to M&A, including the Clario agreement.

Visa Mixed: Net revenue reached $10.9B, up 15% YoY (13% constant-dollar). GAAP EPS grew 17% to $3.03, while non-GAAP EPS rose 15% to $3.17. Payment volume increased 8% on a constant-dollar basis, with cross-border volumes up 12%. Processed transactions totaled 69.4B, up 9% YoY. Shareholder returns were $5.1B through buybacks and dividends, with a $0.670 dividend declared. GAAP operating expenses rose 27% YoY, primarily due to a litigation provision.

American Express Mixed: Q4 revenue was $19.0B, up 10% YoY (9% FX-adjusted). GAAP EPS of $3.53 missed estimates by $0.46. Card Member spend grew 9% (8% FX-adjusted). Provisions totaled $1.4B, with net write-offs at 2.1% vs 1.9% last year. FY2026 guidance calls for 9–10% revenue growth and EPS of $17.30–$17.90, alongside a planned ~16% dividend hike to $0.95 per share.

Chevron Beat: Q4 2025 earnings totaled $2.8B, or $3.0B on an adjusted basis. Sales and other operating revenues reached $45.8B, while CFFO came in at $10.8B, marking a record annual level. Worldwide production rose 12%, with U.S. output up 16% to record highs. The reserve replacement ratio was 158%. The quarterly dividend was raised by 4% to $1.78 per share, and the Hess integration delivered its initial $1B in synergies.

Exxon Mixed: Q4 earnings totaled $6.5B with GAAP EPS of $1.53 and non-GAAP EPS of $1.71. Revenue came in at $82.3B, down ~1.3% YoY from $83.4B last year. Operating cash flow was $12.7B, with free cash flow of $5.6B. Shareholder returns reached $9.5B in Q4, including $4.4B in dividends and $5.1B in buybacks. Upstream Q4 production was 4,988 koebd, delivering the highest full-year output in over 40 years.

EARNINGS PREVIEW:

Date | Symbol | Name | Time |

2-Feb | DIS | Walt Disney Company | Before Open |

2-Feb | PLTR | Palantir Technologies Inc Cl A | After Close |

3-Feb | AMD | Adv Micro Devices | After Close |

3-Feb | MRK | Merck & Company | Before Open |

4-Feb | ABBV | Abbvie Inc | Before Open |

4-Feb | GOOG | Alphabet Cl C | After Close |

4-Feb | GOOGL | Alphabet Cl A | After Close |

4-Feb | LLY | Eli Lilly and Company | Before Open |

5-Feb | AMZN | Amazon.com Inc | After Close |

5-Feb | LIN | Linde Plc | Before Open |

6-Feb | PM | Philip Morris International Inc | Before Open |

VIDEO’s OF THE WEEK:

Investor-ready updates, by voice

High-stakes communications need precision. Wispr Flow turns speech into polished, publishable writing you can paste into investor updates, earnings notes, board recaps, and executive summaries. Speak constraints, numbers, and context and Flow will remove filler, fix punctuation, format lists, and preserve tone so your messages are clear and confident. Use saved templates for recurring financial formats and create consistent reports with less editing. Works across Mac, Windows, and iPhone. Try Wispr Flow for finance.

Please Share This Newsletter With Your Friends.

Also, check my blog here.

This newsletter's content is for informational and educational purposes only and should not be considered trading or investment recommendations. All the opinions in this newsletter are personal and do not belong to any organization.