In partnership with

Weekly Newsletter

Best Month Of The Year For US Markets

First Round, The Clock Stock Exchange, Gets SEC Approval

Ways To Hedge Tail Risk

Why Do Banks Fail?

Why I Will Never Invest In a Banking Stock

Key Points From The FOMC Meeting Minute

QUOTE OF THE WEEK:

“We have two back-to-back 20% years, and now investors are wondering how much good news is baked in. If we look at the 2025 environment, it’s a great setup. We have a new administration coming in that may be pro-animal spirits, you know, a Trump Put. We have a dovish Fed, and interest rates are calming down after rising. There is still $7 trillion in cash on the sidelines. I think sentiments are coming back into check. I would not be too worried about the next 12 months.” Tom Lee, Fundstrat

KEY US ECONOMIC EVENTS NEXT WEEK:

MARKET CLOSE:

Source: CNBC EOD 11/29

Good Afternoon. US stocks recorded the best month of the year and closed positive for the week. December is generally a positive year for the markets, so it will be interesting to see if we have a Santa Clause rally in the last month, considering markets are already at an all-time high. The US is having an exceptional year in terms of equity inflows:

Source: Bloomberg, Barclays

Next week will be busy with critical economic data releases, including the vital unemployment rate on Friday.

For the week:

The S&P 500 is up 1.41%, the Nasdaq is up 1.30%, and the Dow 30 is up 2.37%.

CNN's Fear & Greed Index now stands at 66 (Greed) out of 100, up 7 points from last week. Details here

The top five trending stocks on Reddit are Archer Aviation, Nvidia, MicroStrategy, SPY, and Rocket Lab. Read More

Here is a summary of this week’s key economic releases:

No surprise on inflation: The Personal Consumption Expenditures (PCE) index rose 2.3% year-over-year in October, accelerating from 2.1% in September, in line with expectations. The "core" PCE index, which excludes volatile food and energy costs to capture underlying inflation trends better, increased 2.8% from a year ago, slightly higher than the 2.7% pace recorded in September.

Personal income grew by a robust 0.6% in October, with disposable incomes rising 0.7% and inflation-adjusted real disposable income up 0.4%—the first significant gain in four months. Driven by higher compensation, asset receipts, and transfers, the growth pushed the personal savings rate to 4.4%, signaling sufficient momentum for a strong holiday shopping season.Target Rate Probabilities for Dec 18th FOMC Meeting:

CME FedWatch: * Data as of 29 Nov 2024 09:05:10 CT

FRONT PAGES:

Home sales fall: U.S. new single-family home sales fell in October to their lowest level in nearly two years, driven by rising mortgage rates and hurricane-related disruptions. Read

First Around-the-Clock US Stock Exchange: U.S. regulators have approved the first stock exchange to operate round-the-clock trading, marking a significant shift in how investors access New York-listed equities. The Securities and Exchange Commission (SEC) approved on Wednesday 24 Exchange, a start-up supported by Steve Cohen’s Point72 Ventures, for its two-phase rollout plan. Read

SEC Reports Record Penalties: The SEC reported $8.2 billion in monetary penalties for fiscal year 2024, marking the highest fines in its history. Read

OpenAI Tender Offer: Open AI has initiated a $1.5 billion tender offer, enabling employees to sell shares to SoftBank, CNBC reports. This follows OpenAI's $6.6 billion funding round, valuing the company at $157 billion. Read

MicroStrategy Bitcoin Buying: Microstrategy announced Monday that it acquired 55,000 bitcoins (BTC-USD) last week for $5.4 billion, capitalizing on the cryptocurrency’s all-time high prices. Read

EARNINGS UPDATE:

Analog Devices Beat: exceeded analysts' expectations for fourth-quarter revenue and profit, driven by robust demand for its semiconductors in consumer electronics and a rebound in automotive orders. The consumer electronics market has shown renewed strength following a post-pandemic slowdown, while the automotive segment continues to recover, reflecting positive industry trends. Read

EARNINGS PREVIEW:

Date | Symbol | Name | Time |

2-Dec | BHP | Bhp Billiton Ltd ADR | -- |

3-Dec | CRM | Salesforce Inc | After Close |

4-Dec | RY | Royal Bank of Canada | Before Open |

4-Dec | SNPS | Synopsys Inc | After Close |

5-Dec | TD | Toronto Dominion Bank | Before Open |

9-Dec | ORCL | Oracle Corp | -- |

CURATED INSIGHTS:

Key Points From The FOMC Meeting Minutes:

Nominal treasury yields rose notably over the period. The rise at short maturities reflected increases in both real yields and inflation compensation, while the rise at longer maturities was primarily driven by increases in real yields.

The average of the survey responses indicated that the modal expectation regarding the timing of the end of the balance sheet runoff had shifted a bit later to May 2025.

The ON RRP facility's usage declined by about $140 billion over the inter-meeting period. This decline appeared to be driven primarily by the additional net Treasury bill supply in recent weeks.

The unemployment rate ticked down, and real GDP posted solid gains.

The increase in longer-term yields was primarily attributable to higher-term premiums.

Government money market funds (MMFs) continued to increase allocations to Treasury bills and private repo due to the generally favorable rates on these instruments; usage of the ON RRP facility declined significantly over the period.

Credit availability remained relatively tight for smaller firms.

Consumers appeared to be more price-sensitive and were increasingly seeking discounts.

Wage growth continued to decrease, and the wage premium available to job switchers had diminished.

Some participants remarked that, at a future meeting, the Committee should consider a technical adjustment to the rate offered at the ON RRP facility to set it equal to the bottom of the target range for the federal funds rate, thereby bringing the rate back into alignment with what it was when the facility was established as a monetary policy tool.

Members viewed the economic outlook as uncertain and agreed they were attentive to the risks to both sides of the Committee’s dual mandate.

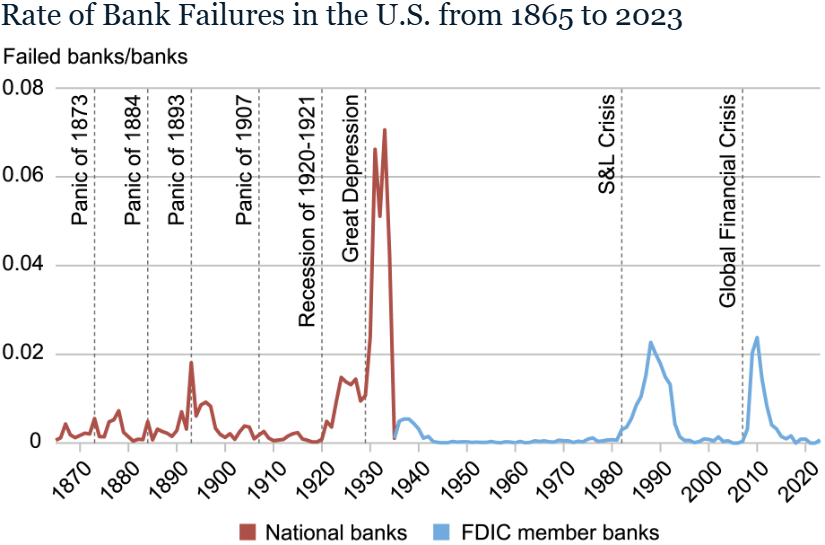

Why Do Banks Fail?

The FRB staff recently published a three-part series of analyses on bank failures in the US. The staff analyzed historical data since 1865 to determine critical reasons for the bank failures.

Source: FRB NY

The staff's fundamental reasons make sense; however, using too much historical data has affected some observations, especially the time taken for the changes to occur. The speed at which a bank can collapse has increased significantly due to various factors. Hence, any timeline-related findings won’t make sense now. Below is the summary of the analysis and my take:

Three Facts:Sharp Rise In NPAs: The analysis reveals that failing banks experienced a sharp 10% rise in nonperforming loans a decade before failure, triggering higher loan loss provisions, a 5% drop in return on assets, and a significant 10% decline in equity-to-assets, while net interest margins remained stable.

Reliance on Noncore Funding: Failing banks relied increasingly on noncore funding, i.e., expensive deposit funding or non-deposit wholesale funding.

Boom-Bust Pattern: Failing banks follow a boom-bust pattern. They grow rapidly for up to three years before failing, and then they contract.

These observations make sense; however, as I mentioned earlier, a decade in #1 can be a year now, and three years in #3 can be as close as last quarter if we consider last year’s bank stress.

Conclusion: The FRB analysis shows that the ultimate cause of failures is almost always insolvency. Even if there were no bank runs or deposit outflows in some cases, it would eventually lead to failure.

Due to the speed at which information travels, it's almost impossible to avoid a bank run if a bank is weak and insolvent in modern times. Hence, as shown by this analysis, it may have taken years or decades for banks to reach failure in the past; however, it’s certainly not relevant now.

On a related topic, check my blog below😀Why I Will Never Invest In a Banking Stock:

Last year, I wrote this blog explaining why I will never invest in a banking stock. Below are key points. You can read my blog for details:There are inherent issues of maturity mismatch in banks' business models.

Banks generally have low returns on equity and

Most importantly, short selling affects banks more than any other sector and can expedite a bank's collapse quickly.

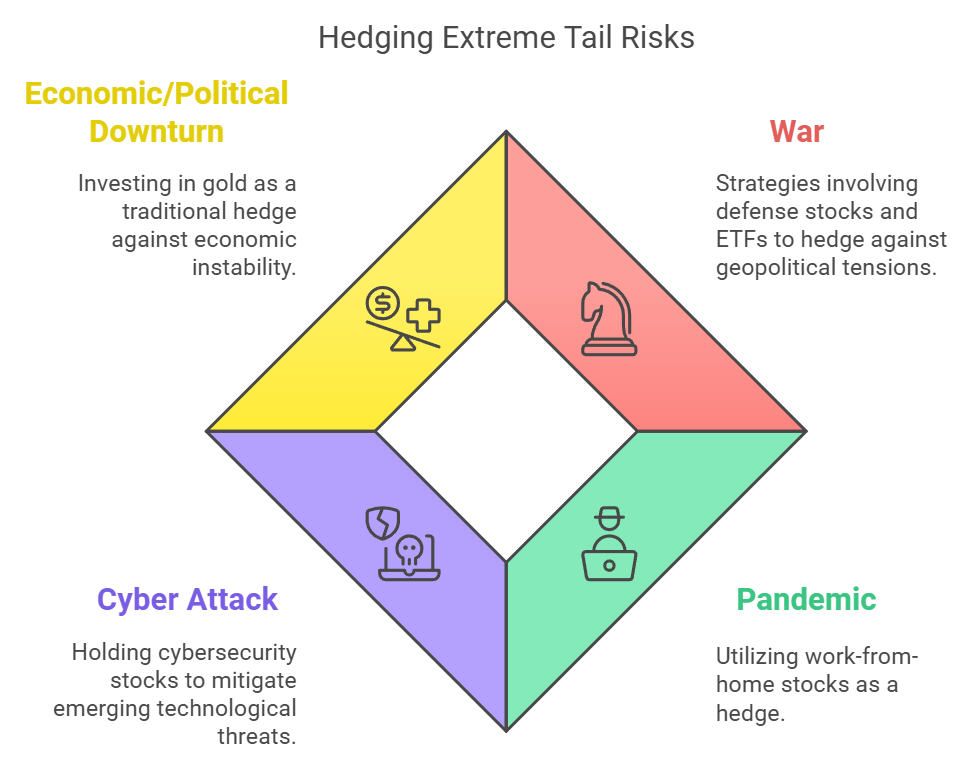

Hedging Tail Risk:

In his article "Hedging Armageddon," Steven Desmyter (President, Man Group) explains the critical role of hedging strategies in mitigating extreme market downturns. He emphasizes that traditional diversification may fall short during systemic crises, as correlations between asset classes can converge, leading to simultaneous declines. Desmyter advocates incorporating tail risk hedging into investment portfolios to protect against severe losses during market turmoil.

This article made me think about the importance of tail risk and the possibilities of easy hedging with some common sense. Below are a few tail risks (some of which Steven D also covered in his article) and possible options to mitigate them:

War: This is a tail risk becoming more probable with recent geopolitical developments. Consider the tensions between Russia and Ukraine, China and Taiwan, etc. The good thing is that it’s easy to hedge by having some defense stocks in the portfolio. Defense stocks are boring in normal times compared to Mag 7’s of the world, so I will struggle to name a few good defense stocks. However, good we have sector ETFs. An easier option is to hold defense ETF in your portfolio, e.g., “XAR,” etc. (not a recommendation).

Pandemic: This is very recent in memory. Theoretically, pharma stocks should act as a hedge for this tail event, but I don’t think so. It’s always morally impossible for pharma companies to charge more money and make profits. Look at Pfizer's stock performance since the pandemic. There were no significant gains for shareholders even though Pfizer led the COVID-19 vaccine efforts. I think work-from-home stocks are a better hedge for pandemic risk.

Cyber Attack: Steven D hasn’t discussed this, surprisingly, in his article, but I think it is one of the emerging top risks. There are many good cyber security companies, especially in the US, that one can hold to hedge this risk. These are also hot tech sector companies, so you won’t technically give up on exposure to the growth.

Severe Economic Downturn/ Political Turmoil: This is an improbable event for an innovative economy and stable democracy like the US. However, you will always find doomsday predictors, and even though I can't entirely agree with them, it doesn’t hurt to be careful. The best hedge for this type of risk will be Gold, which has performed much better recently due to multiple reasons (including central bank buying). I covered why Gold is surging a few months ago in my newsletter.

Some will argue that crypto is the best hedge against this risk, but I disagree. History has provided that crypto market performance is highly correlated to the stock market or needs loss monetary policy to perform. I covered last week that Bitcoin is here to stay, but it's not the hedge against bad economic times or severe political turmoil.

Conclusion:

Primal Thesis Newsletter

As Steven D calls them, we can not avoid tail risks or armageddon events. Significant tail risks can be hedged by holding sector ETFs such as defense and cyber security. In addition, Gold can play a crucial role in the coming years. How much of a percentage to hold is up to individual considerations.

VIDEO’s OF THE WEEK:

This Smart Home Company Hit $10 Million in Revenue—and It’s Just the Beginning

No, it’s not Ring or Nest—it’s RYSE, the company redefining smart home innovation, and you can invest for just $1.75 per share.

RYSE’s patented SmartShades are transforming how people control their window shades—offering seamless automation without costly replacements. With 10 fully granted patents and a pivotal Amazon court judgment safeguarding their technology, RYSE has established itself as a market leader in an industry projected to grow 23% annually.

This year, RYSE surpassed $10 million in total revenue, expanded to 127 Best Buy locations, and experienced explosive 200% month-over-month growth. With partnerships in progress with major retailers like Lowe’s and Home Depot, they’re set for even bigger milestones, including international expansion and new product launches.

This is your last chance to invest at the current share price before their next stage of growth drives even greater demand.

Subscribe to my Newsletter here.

Also, check my blog here.

This newsletter's content is for informational and educational purposes only and should not be considered trading or investment recommendations. All the opinions in this newsletter are personal and do not belong to any organization.