In partnership with

Weekly Newsletter

🔎 Key Points From The Fed Beige Book

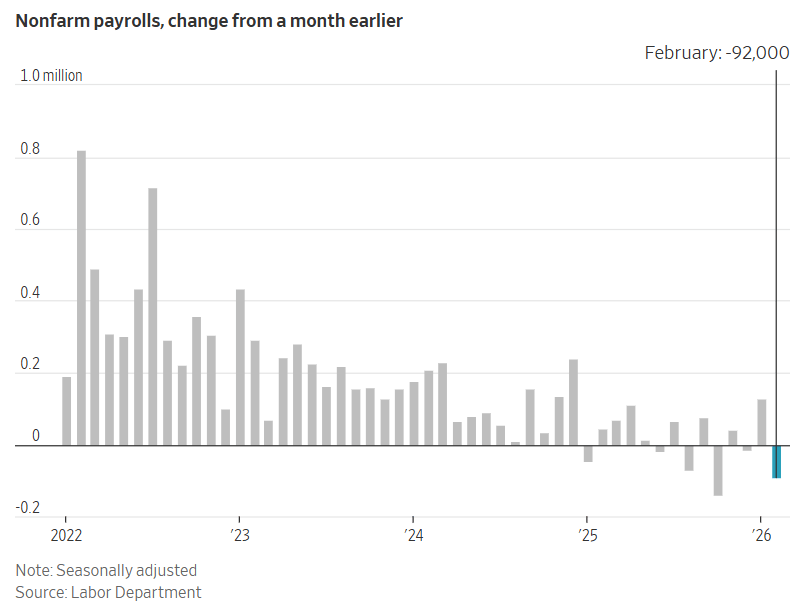

📉 U.S. Labor Market Unexpectedly Contracts

🗣️ Summary Of Comments From Multiple FOMC Members

🤖 Labor Market Impact Of AI

🏦 BlackRock Limits Withdrawals Amid Private Credit Concerns

🛢️ Oil Surged To Its Highest Level Since 2023

QUOTE OF THE WEEK:

“Last year, the narrative in markets was that the economy faced headwinds from the trade war. But that narrative has shifted dramatically. Now the focus has turned to potential tailwinds from AI spending and a broader industrial renaissance. Perhaps the most important catalyst is the “big, beautiful bills” that began taking effect on January 1. According to the CBO, these policies could lift GDP growth by about 0.9% this year. As a result, the key risk to watch is that the economy may actually begin accelerating over the coming quarters.” - Torsten Slok, Chief Economist at Apollo Global Management

KEY US ECONOMIC EVENTS NEXT WEEK:

MARKET CLOSE:

CNBC EOD 3/6

WEEKLY MARKET WRAP:

Good Afternoon. Bad week for markets, with all major indices recording losses amid geopolitical tensions, weak labor data, and concerns about private credit. Earnings continued to be strong.

Below are the key things to note this week:Oil Surges:

Oil surged to its highest level since 2023 amid escalating tensions over the Iran war, while a weak U.S. jobs report signaled a rising softness in the labor market. The S&P 500 fell 1.3% as oil crossed $90 per barrel, capping Wall Street’s worst week since October.

U.S. Labor Market Unexpectedly Contracts:

WSJ

U.S. employers cut 92,000 jobs in February, a sharp reversal from January’s 126,000 gain and far worse than the 50,000 increase economists expected. The unemployment rate edged up to 4.4%, signaling emerging weakness as job growth has slowed across multiple sectors in recent months.

Rising oil prices and a mixed labor market put pressure on both the Fed's inflation and unemployment goals. Rate cuts will depend on which Fed mandate most FOMC voting members prioritize. More on this in curated insights.

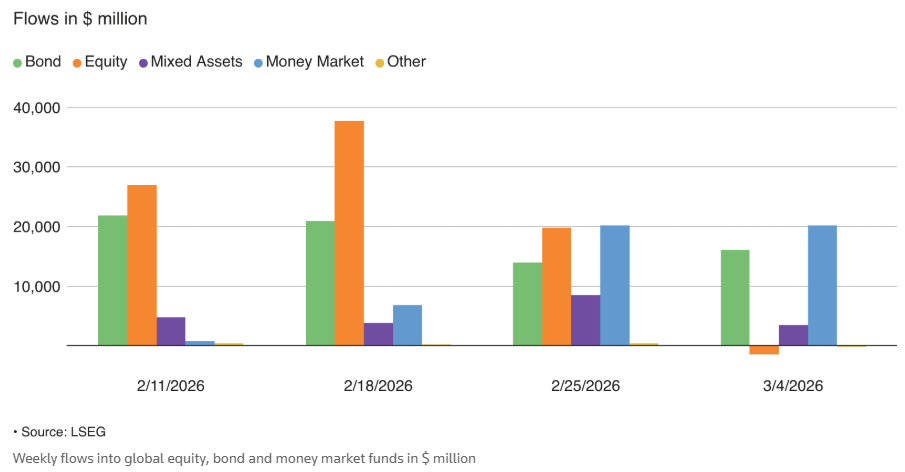

Global Equity Funds See First Outflow In Two Months:

Reuters

Global investors cut exposure to equity funds for the first time in eight weeks as the escalating U.S.–Iran conflict reignited inflation fears and weakened risk appetite. U.S. equity funds led the decline, recording $21.9B in outflows—the largest since Jan 7—pushing global equity funds to a net $1.44B outflow.

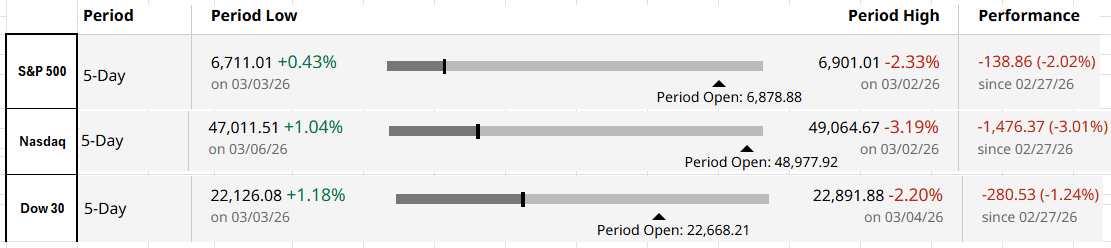

For the week:

The S&P 500 is down 2.02%, the Nasdaq is down 3.01%, and the Dow 30 is down 1.24%.

Baarchart

CNN's Fear & Greed Index now stands at 27 (Fear) out of 100, down 16 points from last week. Details here

The top five trending stocks on Reddit are SPY, USO, NVIDIA, Hims & Hers Health, and DTE Energy. Read More

Liquidity:

Banking Reserves + ON RRP: Banking reserves remain at approximately $3 trillion. ON RRP balance remains immaterial.

Standing Repo Operations: The New York Fed’s standing repo operation (primarily reflecting SRF take-up) as of March 7th is zero.

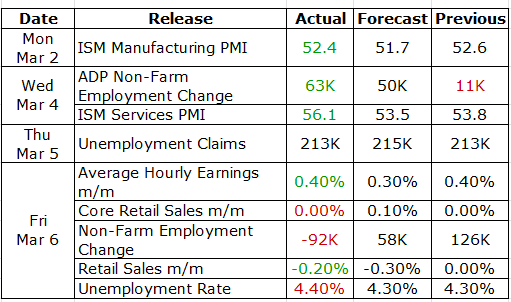

Here is a summary of this week’s key economic releases:

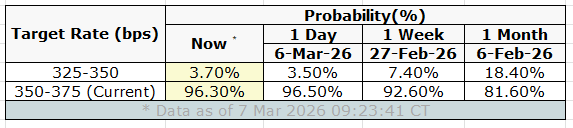

Target Rate Probabilities for March 18th FOMC Meeting:

CME FedWatch

CURATED INSIGHTS & ANALYSIS:

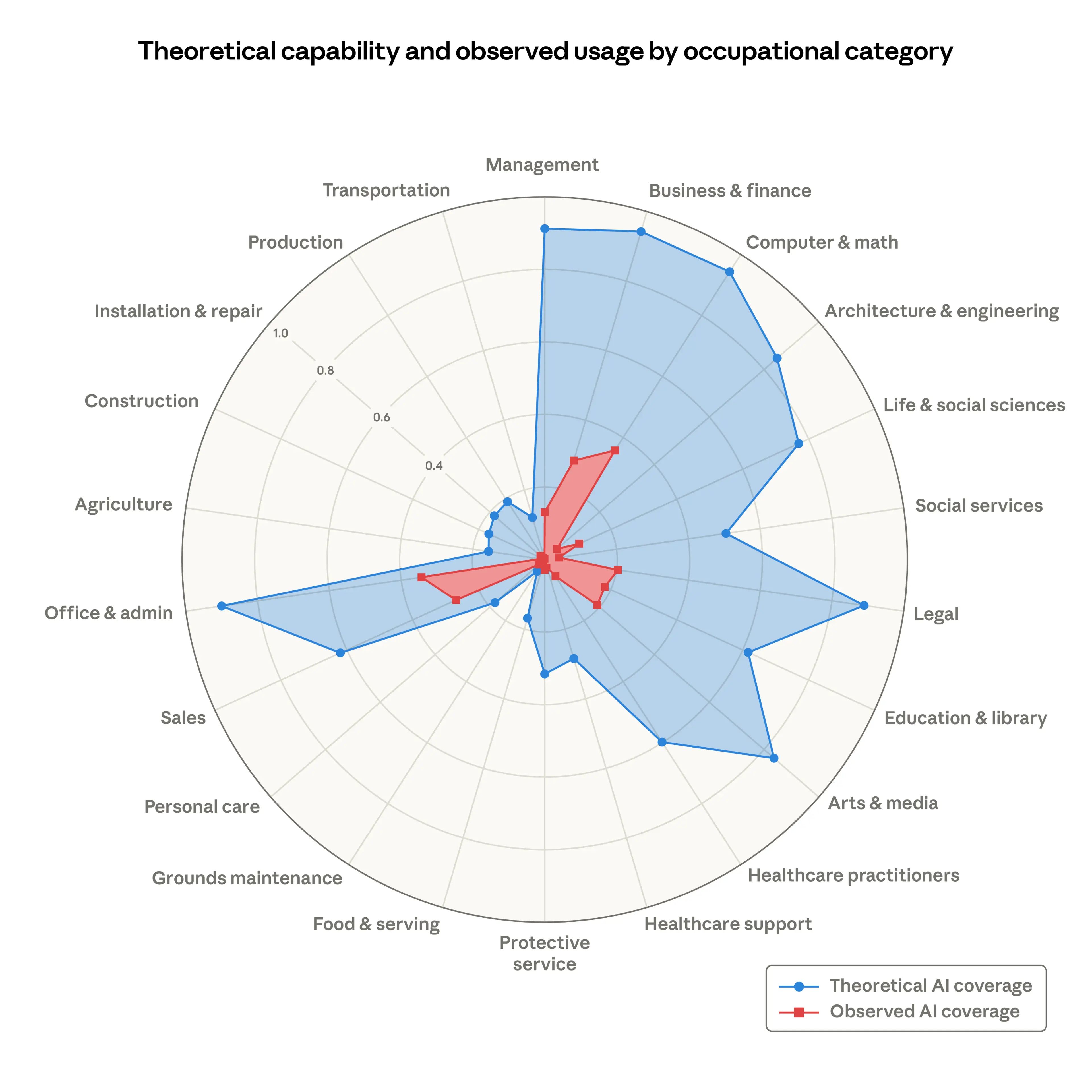

Anthropic Study On AI & Jobs:

Source: Anthropic

Anthropic released a new research report measuring AI’s labor-market impact using an “observed exposure” metric that combines theoretical AI capabilities with real-world usage data. The analysis finds that while many white-collar tasks are technically automatable, actual adoption remains far below potential and has not yet led to a measurable rise in unemployment, though early signals suggest AI may already be affecting hiring patterns. Key points -AI adoption is still far below its theoretical capability across most occupations.

Most exposed roles include programmers, customer service, data entry, and financial analysis.

Occupations with higher AI exposure are projected to grow slightly slower through 2034.

Workers in highly exposed jobs tend to be more educated, higher paid, and more likely to be female.

No clear rise in unemployment in exposed occupations since the AI boom began.

However, hiring of younger workers in exposed roles has slowed, suggesting early labor market adjustment.

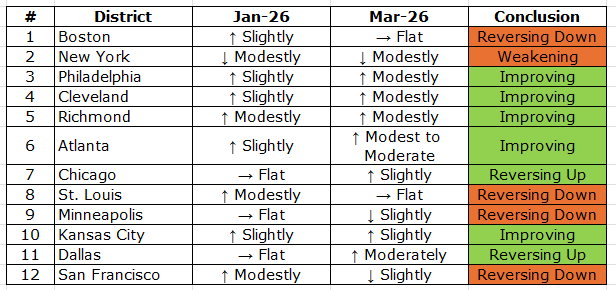

Key Points from the Fed Beige Book:

Primal Thesis

Overall activity improved: 7 districts reported slight-to-moderate growth; 5 were flat or down

Consumer spending rose slightly overall, but lower-income pullback and price sensitivity remained a drag; auto sales were mostly down

Manufacturing improved, with 8 districts reporting growth; data-center and energy-infrastructure demand stood out

Housing stayed soft: most districts saw slightly weaker residential sales/construction; affordability and low inventory remained issues

Financial services were stable to up, with commercial lending the main bright spot

The labor market was broadly stable: 7 districts reported no hiring change; AI was more about productivity than outright replacement

Wages grew modestly to moderately; health-insurance costs continued to pressure compensation budgets

Prices rose moderately; tariffs were still pushing up input costs, but many firms held prices steady because customers were price-sensitive

Outlook was broadly optimistic, with most districts expecting slight-to-moderate growth ahead

Fed Speak This Week:

Multiple Fed members spoke today. Below is the summary -

Fed Member | Rate Cut Inclination | Key Policy Stance | View on the Labor Market | View on Inflation | Other Highlights |

Stephen Miran (Governor) | High / Dovish | Miscalibrated. Believes policy is "too tight" and the labor market needs more support now. | Weakening Demand. Sees slack in younger and non-college workers, indicating a demand issue rather than a supply/immigration one. | "Phantom" Inflation. Claims 0.4% of core inflation is "fake," driven by portfolio management fees. | Views oil shocks as a reason for more dovish policy, as they pull demand from the economy. |

Christopher Waller (Governor) | Higher / Willing | Labor-Focused. More worried about labor market downside risk than inflation persistence. | Fragile. Concerned hiring is too concentrated; 80% of the economy showed zero to negative growth. | Transitory. Believes inflation will drop as tariff effects pass. Views oil as a "one-off" event. | Views private credit issues as "one-off" fraud cases rather than a systemic stability risk. |

Austan Goolsbee (Chicago) | Patient | Data-Dependent. Conflicting data means it's a time for "sniffing" the data before acting. | Concerning. Worried about the "tough miss" in jobs and the lack of new hiring. | Stalled. Disturbed by "disturbingly high" inflation in non-tariff categories like services. | High productivity (2.8%) allows for faster wage growth without fueling inflation. |

Mary Daly (San Francisco) | Neutral | Cautious. "No one month of data is decisive." Needs more time to assess the "balance of risks." | Vulnerable. Describes a "low hiring, low firing" state that is susceptible to shocks. | Balanced Risk. Watching oil prices for persistence; notes inflation is still above target. | Argues that current wage growth is not "outsized" when balanced against productivity. |

Beth Hammack (Cleveland) | Low / On Hold | Neutral. Sees risks as "two-sided." Policy is likely neutral; stay on hold for "quite some time." | Stabilizing. Characterized the market as stabilizing in the 4.3%-4.4% range. | Persistent. Progress has stalled at ~3% for two years. Concerned about pricing pressures. | Open to shifting the balance sheet to a "scarce reserve" regime using repos. |

FRONT PAGES:

NVIDIA Signals Final OpenAI Funding Before IPO: NVIDIA CEO Jensen Huang said the company’s recent $30B investment in OpenAI could be the final funding round before the AI startup eventually goes public. Read

Crypto Gains Direct Access To Fed Payment Rails: Crypto moved closer to mainstream finance as Kraken’s banking unit secured access to the Federal Reserve’s core payment systems, becoming the first crypto firm able to move funds on the same payment rails used by thousands of banks and credit unions. Read

SEC Moves To Drop Justin Sun Fraud Case: The SEC moved to dismiss its civil fraud lawsuit against crypto investor Justin Sun, who recently invested in President Trump’s crypto projects while seeking regulatory leniency. A firm allegedly linked to Sun agreed to pay a $10M fine over claims employees manipulated trading in the TRX crypto asset, pending court approval. Read

Robinhood Venture Fund Debut Stumbles: Robinhood’s Venture Fund I fell 11% in its NYSE debut, signaling weaker investor appetite for riskier assets amid rising geopolitical uncertainty. The RVI fund provides retail investors with exposure to private firms, including Revolut and Databricks, aiming to broaden access to traditionally restricted venture investments. Read

BlackRock Limits Withdrawals Amid Private Credit Concerns: BlackRock restricted withdrawals from a flagship debt fund following a surge in redemption requests, highlighting rising investor concerns around the $2T private credit market. Shares of the world’s largest asset manager fell 6.7% during a broader selloff triggered by weak U.S. jobs data and escalating U.S.–Israeli conflict with Iran. Read

EARNINGS UPDATE:

Primal Thesis

Autozone Miss: Net sales rose 8.1% YoY to $4.3B. Net income totaled $468.9M with diluted EPS of $27.63. Same-store sales increased 5.2% overall (3.3% CC), led by domestic growth of 3.4% and international growth of 17.1% (2.5% CC). Gross margin declined to 52.5%, primarily due to a 138 bps non-cash LIFO charge. The company repurchased 85k shares for $310.8M, with $1.4B in remaining authorization, and opened 64 net new stores, bringing the total to 7,774.

Crowdstrike Beat: ARR reached $5.25B, up 24% YoY, surpassing the $5B milestone. Net new ARR rose 47% to a record $331M in Q4. The company reported positive GAAP net income and record non-GAAP net income. Q4 operating cash flow hit a record $497.9M, with FCF at $376.4M. Falcon Flex ARR climbed over 120% YoY to $1.69B. Cash and cash equivalents stood at $5.23B.

Ross Stores Beat: Q4 sales rose 12% YoY to $6.64B with comparable store sales up 9%. Diluted EPS came in at $2.00, above company guidance of $1.77–$1.85, beating consensus by $0.38 (+23.5%). Revenue exceeded estimates by $1.32B (+24.8%). The company authorized a new $2.55B two-year share repurchase and raised its dividend 10% to $0.445. Outlook: Q1 EPS $1.60–$1.67 with comps up 7%–8%; FY2026 EPS $7.02–$7.36.

Broadcom Mixed: Revenue reached $19.3B, up 29% YoY, marking a record quarter driven by AI semiconductors. GAAP net income was $7.35B and non-GAAP net income was $10.19B, with adjusted EBITDA of $13.13B (68% margin). AI revenue totaled $8.4B, surging 106% YoY. The company guided Q2 FY2026 revenue to about $22B with ~68% EBITDA margin and announced a new $10B share buyback after returning $10.9B to shareholders in Q1.

Costco Beat: Q2 revenue rose 9.2% YoY to $69.6B, with net sales up 9.1% to $68.2B. Diluted EPS increased to $4.58 from $4.02 last year (+13.9% YoY). Adjusted comparable sales rose 6.7%, while adjusted e-commerce sales jumped 21.7%. February (4 weeks) sales reached $21.69B, up 9.5% YoY. The company operates 924 warehouses globally, including 634 in the U.S. and Puerto Rico and 114 in Canada.

Marvell Mixed: Q4 revenue reached $2.22B, up 22% YoY and $19M above guidance midpoint. Non-GAAP EPS was $0.80, while GAAP EPS came in at $0.46. Data center generated $1.65B (74% of revenue) and communications & other segments $567M (26%). Operating cash flow was $373.7M with a cash balance of $2.64B. For Q1 FY2027, the company guides to $2.4B revenue ±5% and Non-GAAP EPS of $0.79 ±$0.05.

EARNINGS PREVIEW:

Date | Symbol | Name | Time |

12-Mar | ADBE | Adobe Systems Inc | After Close |

12-Mar | WPM | Wheaton Precious Metals | After Close |

10-Mar | ORCL | Oracle Corp | After Close |

12-Mar | BABA | Alibaba Group Holding ADR | Before Open |

VIDEO’s OF THE WEEK:

A comprehensive guide for addressing the tax talent crisis

A labor shortage in tax is driving the need for a new skill set: one that blends technical tax knowledge with digital fluency.

Automation, AI and data-driven insights now define the role of tax professionals.

This new era of tax is not simply about adopting new tools, it’s about reshaping the skill set and mindset required to thrive in this field. Check out this guide for actionable insights into how to cultivate these skills with your team. See how advanced technologies can help bridge the tax tech gap to increase efficiency, ensure compliance, and drive better decision-making.

Please Share This Newsletter With Your Friends.

Also, check my blog here.

This newsletter's content is for informational and educational purposes only and should not be considered trading or investment recommendations. All the opinions in this newsletter are personal and do not belong to any organization.