Weekly Market Thesis

Inflation is falling closer to the Fed target as expected.

China Central Bank Stimulus and Fiscal Support Plan.

Headlines from JP Morgan, OpenAI, Volkswagon, and more.

Why I will never bet against Mark Zuckerberg.

Bain & Company's Annual Technology Report focuses on AI.

Impact of Reg YY FAQ on Bank HLA (Highly Liquid Asset) Monetization.

QUOTE OF THE WEEK:

“Overall, inflation was essentially flat. We saw a little bit of inflation in fresh. That was mainly driven by produce right now. That was sort of the key category there that drove- but again, there was very low inflation, and there was nothing meaningful to talk about.” Gary Millerchip - EVP & CFO, Costco.

KEY US ECONOMIC EVENTS NEXT WEEK:

Source: Forex Factory

MARKET CLOSE:

EOD 9/27: CNBC

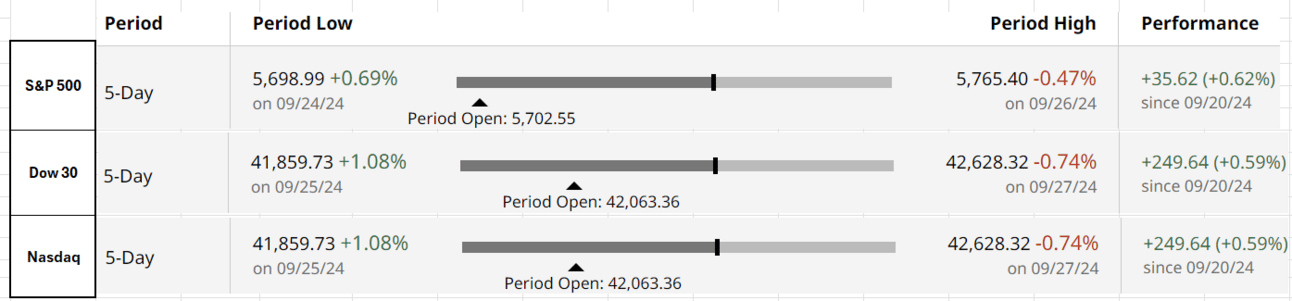

Good Afternoon. US markets closed positive for the week as the economic data was broadly in line with expectations, with inflation cooling and the economy doing fine. Stimulous from the Central Bank of China also helped lift global market sentiments.

For the week:

The S&P 500 is up 0.62%, the Nasdaq is up 0.95%, and the Dow 30 is up 0.59%.

Source: barchart

CNN's Fear & Greed Index now stands at 68 (Greed) out of 100, up 5 points from last week. Details here

The top five trending stocks on Reddit are Nvidia, SPY, Rocket Lab USA, AST Spacemobile, and Tesla. Read More

Here is a summary of this week’s key economic releases:

The macro data released this week once more confirms a slowdown in the US economy and further lowers any fear of a recession. The GDP grew by 3%, in line with the consensus.

The PCE price index rose 0.1% lower than expected in August, putting the 12-month inflation rate at 2.2%, close to the 2% Fed average inflation target. In last week's newsletter, I covered why inflation is expected to come down (Base effect, drop in pandemic savings, and average inflation targeting). The drop in PCE is in line with what I expected and also validates the forecasts done by Fed governor Chris Waller’s team.

Target Rate Probabilities for Nov 7th FOMC Meeting:

Source: CME Fed Watch

FRONT PAGES:

China’s Bold Stimulus Measures: China's central bank unveiled its biggest stimulus measure since the pandemic on Tuesday to aid the economy. Thanks to these measures, Chinese stocks posted their best week since 2008. Below are the key policy changes -

OpenAI expects to lose $5bn on $3.7bn in revenue this year. Revenue is expected to jump to $11.6bn next year. The company is currently pursuing a funding round that would value it more than $150bn. Its board is considering restructuring the firm to a for-profit business. Read More

JPMorgan Chase is preparing to sue the U.S. government over potential penalties from the Consumer Financial Protection Bureau related to its handling of the Zelle payment platform. Read More

Volkswagen is considering closing its factories in Germany for the first time in its 87-year history due to increasing competition and challenges in profitability. Read More

Janus Henderson has partnered with Anem Limited to launch a blockchain-based fund that provides investors access to short-term U.S. Treasurys, potentially transforming the ETF industry through benefits like 24/7 trading and instant settlement. Read More

Gold hit an all-time high mid-week again. This has been partly driven by the demand from global central banks, which I covered in this newsletter on 9/1. Gold climbed ~30% this year, outperforming the benchmark S&P 500 index’s 20% gain. Read More

Federal Reserve Vice Chair for Supervision Michael Barr stated that the discount window could serve as a source of normal funding for banks, not just as an emergency measure, emphasizing the Fed's efforts to reduce the stigma associated with its use and encourage more routine borrowing from this facility. Read More

EARNINGS UPDATE:

AutoZone missed fourth-quarter profit and sales estimates, as higher costs and weaker consumer discretionary spending hurt results. On the conference call, the company mentioned opening 49 new international stores in Mexico and Brazil. Currently, international stores account for 13% of the total stores. The company plans to ramp up international store openings by 2028 and aims to open 200 international stores annually. Read More

Micron delivered its best quarterly revenue growth in a decade in the fourth quarter that ended Aug. 29, and its forecast for the current period came in widely above Wall Street estimates. The company expects high-bandwidth memory (HBM) chips used in AI data centers to increase to $25 billion in 2025, up from $5 billion this year. Read More

Costco reported mixed earnings with EPS beat but missed revenue expectations. The company opened 30 new warehouses in FY 2024, with its first warehouse in Maine delivering Costco to its 47th US state. Read More

EARNINGS PREVIEW:

Date | Symbol | Name | Time |

10/1/2024 | NKE | Nike Inc | After Close |

10/1/2024 | PAYX | Paychex Inc | Before Open |

10/3/2024 | STZ | Constellation Brands Inc | Before Open |

CURATED INSIGHTS:

Why I will never bet against Mark Zuckerberg: Bloomberg reported that Mark Zuckerberg’s net worth has jumped sixfold in the last two years, and Meta’s stock is up 60% this year. This is thanks to the successful pivot from a social media company to a metaverse company.

During the pandemic, when the market was flooded with liquidity, everyone was upbeat for crypto and metaverse. However, Meta is the only firm I know of that achieved this success in this space, where most of the projects had to wound down as soon as excess liquidity dried when the Fed started increasing the rates. This highlights the genius of Zuckerburg. Below is the track record of Mark Zuckerberg, which I observed over more than a decade, which shows that he is always two steps ahead of the competition and has the foresight that anyone else could hardly match in his game -

I came to the US in 2007 from India to pursue my MBA. At that time, I had never heard of Facebook, and I used to have an Orkut.com account, which was a very popular social media site in India. I started using Facebook in 2007 and naturally moved to FB, and eventually, Google shut down Orkut as the whole world was moving to Facebook. Then, after a year or so, Facebook made significant design changes, and everyone initially hated those changes. I remember my friends saying they would no longer use FB as they hated the new website. However, the new design gained popularity in a few months, and Facebook got a few more years of life under its belt. That was the first time I noticed this guy knew what he was doing. Facebook had a few more design changes after 2008, and I remember the exact story where initially, users may not have liked it but eventually accepted the new changes.

When FB was getting out of date, Mark quickly noted that, and he purchased an Instagram. The story of how he purchased Instagram is also interesting: He bought it over the weekend to avoid competition. Instagram did not make any money when Facebook bought it.

He declined Yahoo’s $1bn offer in 2006 to buy Facebook against the advice of his board as he was confident that he could make FB bigger.

In 2014, Mark bought Whatsapp, another great acquisition.

He continued to innovate Instagram, sometimes copying features from competitors like Snapchat, and never giving up.

The latest example is his gamble with Metaverse, where he changed the company's name and went all-in with this belief. Initially, he faced challenges. In 2022, Meta was in trouble, but Zuckerburg again made tough decisions and let go of ~15% of the workforce. Ultimately, Mark Zuckerberg proved correct again with success in the hardware segment outside social media's core strength. He was also wise to stitch the partnership with RayBan, which I am sure helped Meta with the hardware side of things for the Metaverse push.

Finally, if you watch the movie Social Network, you can see that Zuckerberg is cunning and intelligent and will do anything to achieve success. Over the years, he has proven this many times, and I will never bet against him. He can sense where the tide is turning way better than many in social media and tech innovation.

Impact of Reg YY FAQ on Bank HLA (Highly Liquid Asset) Monetization: On Tuesday, Aug. 13, 2024, the Federal Reserve Board published a Reg YY FAQ response impacting the Internal Liquidity Stress Tests (ILST) assumptions. I covered that briefly in this newsletter on 8/25. I think there are two main implications of this clarification: G-SIB ILSTs and overall improvements in the discount window readiness. Please check my detailed blog post on this topic here.

The AI Opportunity: Bain & Company released its Annual Technology Report this week. Below are the key highlights:

The AI market could reach $780 billion to $990 billion by 2027.

The number of large companies investing more than $100 million in AI has doubled in a year.

Gen AI saves 10-15% of software engineering time, but with the proper process, it can save up to 30% of time.

Demand for upstream components could rise 30% or more by 2026, creating the next chip shortage.

Neel Keshkari on Why He Supported Cutting Rates Last Week: The Minneapolis Fed president wrote an essay explaining why he supported the 50bp cut. The key factors were substantial progress on inflation, softening of the labor market, and confusing economic signals. Read More

VIDEO’s OF THE WEEK:

Subscribe to my Newsletter here.

Also, check my blog here.

This newsletter's content is for informational and educational purposes only and should not be considered trading or investment recommendations. All the opinions in this newsletter are personal and do not belong to any organization.