In partnership with

Weekly Newsletter

🚀 NVIDIA Customers Racing To Buy AI Compute

📊 Another Strong Earnings Season Almost Over

📉 Treasuries Rally & Mortgage Rates Fall

🏦 Banking Reserves Cross $3 Trillion

🏭 Wholesale Prices Rose More Than Expected

QUOTE OF THE WEEK:

“The wave that we're seeing now is the agentic AI inflection, and the next inflection beyond that is physical AI, where we take AI and these agentic systems into the physical applications, such as manufacturing, such as robotics. And so that's a giant opportunity ahead.” - Jen-Hsun Huang - Co-Founder, CEO, NVIDIA

KEY US ECONOMIC EVENTS NEXT WEEK:

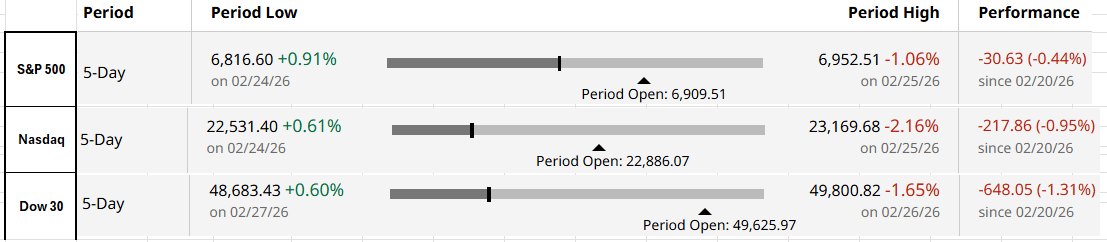

MARKET CLOSE:

CNBC EOD 2/27

WEEKLY MARKET WRAP:

Good Afternoon. AI and private credit-related fear spooked markets this week, too, with all major indices closing in the red. Good that the US struck Iran over the weekend, as markets would have suffered major volatility if this occurred during the week.

Below are the key things to note this week:

The US and Israel Strike Iran:

The US and Israeli forces struck Iran over the weekend. With the supreme leader dead, I hope the conflict will not escalate a lot more, and markets will be calmer on Monday. As long as there is no major military activity, markets should not react negatively. Iran controls 3% of the world's oil supply, so depending on the scale of the conflict, oil prices may shoot up when trading opens on Sunday night. Eight OPEC+ members—including Saudi Arabia, Russia, and the UAE—are set to meet on Sunday. If supply disruptions appear sustained, the group may raise output to preempt a broader shock to global oil markets.

Treasury yeild fall to the lowest level since November:

Bloomberg

Treasuries rallied as a renewed tech selloff pushed the 10-year yield to its lowest level since November, briefly touching 4.01%. Yields fell at least 3bps across the curve, led by the 7-year sector, reflecting a clear bid for duration. Month-end index rebalancing on Friday could add incremental demand, with passive flows expected to drive above-average buying in Treasuries.

Wholesale prices rose more than expected:Core PPI (ex-food & energy) rose 0.8% m/m, accelerating from 0.6% in December and sharply above the 0.3% consensus.

Headline PPI increased 0.5% m/m, also topping the 0.3% forecast and 0.1pp above the prior month.

On a y/y basis, core wholesale prices advanced 3.6%, while headline PPI rose 2.9%.

For the week:

The S&P 500 is down 0.44%, the Nasdaq is down 0.95%, and the Dow 30 is down 1.31%.

Barchart

CNN's Fear & Greed Index now stands at 43 (Fear) out of 100, unchanged from last week. Details here

The top five trending stocks on Reddit are NVIDIA, SPY, Netflix, Microsoft, and QQQ. Read More

Liquidity:

Banking Reserves + ON RRP: Banking reserves remain at approximately $3 trillion. ON RRP balance remains immaterial.

Standing Repo Operations: The New York Fed’s standing repo operation (primarily reflecting SRF take-up) as of Feb 27th is $0.

Here is a summary of this week’s key economic releases:

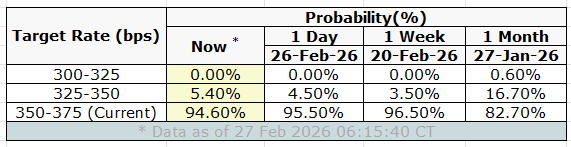

Target Rate Probabilities for March 18th FOMC Meeting:

CME FedWatch

CURATED INSIGHTS & ANALYSIS:

No issue with earnings:

LSEG

The above QoQ comparison of S&P500 earnings shows that earnings in this season were very strong. We cannot predict geopolitical events like the latest Iran war, and hopefully, it will be over soon. Ultimately, markets will follow earnings once short-term volatility subsides.Key Points from NVIDIA Earnings Call:

Business Drivers

Blackwell architecture demand remains extremely strong; Grace Blackwell systems accounted for ~2/3 of data center revenue

Networking revenue hit $11B in Q4, up 3.5x YoY, driven by NVLink, Spectrum-X, and InfiniBand

Sovereign AI business surpassed $30B for the year, tripling YoY

Gaming revenue of $3.7B, up 47% YoY, though supply constraints are expected to persist

Strategic Moves

$10B investment in Anthropic announced, with a partnership for training on Blackwell/Rubin systems

Licensing deal with Groq for low-latency inference technology

Rubin platform unveiled (6 new chips); first samples shipped, production expected H2 2026

Jensen cited Claude Code, OpenAI Codex, and agentic AI broadly as key demand drivers

Key Themes from Jensen

"Compute equals revenues" — inference tokens are now directly monetized, making GPU capacity a revenue-generating asset for customers

Agentic AI has hit an inflection point in the last 2-3 months

Physical AI (robotics, autonomous vehicles) is the next major wave

Long-term data center CapEx opportunity seen at $3-4 trillion by 2030

Weak Earnings from Home Depot and Lowe’s:

Both Lowe’s (LOW) and Home Depot (HD) reported earnings this week that disappointed investors, leading to stock declines. The main reasons for their earnings misses are summarized below:Stagnant Housing Market: Both companies cited ongoing weakness in the housing market, resulting in reduced demand for home improvement projects. High mortgage rates and affordability issues have discouraged new home purchases and renovations, directly impacting sales growth.

Cautious Consumer Spending: Economic pressures, including inflation and broader economic uncertainty, have made consumers more cautious about discretionary spending. This has resulted in fewer large-ticket purchases and home improvement projects.

Flat or Lowered Sales Guidance: Lowe’s forecasted flat to 2% sales growth for the upcoming year, which was below analyst expectations. Home Depot also maintained a cautious outlook, projecting only gradual margin improvement and modest growth.

Professional Segment Growth Not Enough: While both companies have seen some growth in their professional customer segments, it has not been sufficient to offset the slowdown in DIY (do-it-yourself) consumer demand.

Inventory and Cost Pressures: Both retailers have faced higher costs and inventory management challenges, which have pressured margins and profitability.

In summary, the combination of a sluggish housing market, cautious consumer behavior, conservative sales outlooks, and ongoing cost pressures led both Lowe’s and Home Depot to miss earnings expectations this week.

FRONT PAGES:

Geopolitical Risk: The US and Israel struck Iran, with Israel targeting Iran’s supreme leader, president, and armed forces chief. According to CNN sources, the US is preparing for several days of continued attacks. Read

Netflix Walks Away: Netflix is stepping away from its bid to acquire Warner Bros. Discovery’s studio and streaming assets after the WBD board determined that Paramount Skydance’s revised proposal constituted a superior offer. Read

OpenAI Valued @ $730bn: OpenAI closed a $110B funding round—more than 2x last year’s record raise. Amazon committed $50B, Nvidia $30B, and SoftBank $30B. The deal values OpenAI at a $730B pre-money, up sharply from $500B in October’s secondary round. Read

Financial Times

Mortgage Rates Fall: US mortgage rates fell below 6% this week, breaking a critical threshold after years of elevated borrowing costs that sidelined buyers. The average 30-year fixed rate declined to 5.98% on Thursday, its first sub-6% reading since 2022, according to Freddie Mac. Read

First major AI job losses: Block will cut thousands of jobs and increasingly rely on AI to replace displaced roles. Headcount will fall from 10,000 to just over 6,000, CEO Jack Dorsey said in a shareholder letter Thursday. Read

EARNINGS UPDATE:

Home Depot Miss: Q4 sales were $38.2B, down 3.8% YoY, as the prior year included a 14th week (~$2.5B); comparable sales rose 0.4% (+0.3% U.S.). GAAP EPS was $2.58 (adjusted $2.72) vs. $3.02 last year, missing consensus (EPS $3.53; revenue $41.7B). The dividend increased 1.3% to $2.33, marking the 156th straight quarterly payout. FY2026 guides to 2.5%–4.5% sales growth and flat to +4% EPS growth.

Mercadolibre Miss: Net revenues and financial income rose 45% YoY to $8.76B (+47% FXN). Operating income was $889M with a 10.1% margin (9.0% excluding $99M Brazil tax credits). Net income reached $559M (6.4% margin) with a normalized tax rate vs Q4’24. GMV grew 36.8% to $19.9B and TPV 42.1% to $83.7B. Advertising revenue surged 67% YoY (FXN) in Q4’25. Adjusted EBITDA was $1.13B; Adjusted FCF $763M.

Salesforce Beat: Q4 revenue rose 12% Y/Y to $11.2B, with Subscription & Support up 13% to $10.7B. Operating margin was 16.7% GAAP and 34.2% non-GAAP. RPO increased 14% to $72.4B; current RPO rose 16% to $35.1B. Buyback authorization expanded to $50B; dividend raised to $0.44/share. Agentforce ARR surged 169% to $800M, with 29k deals closed (+50% Q/Q). FY27 revenue guided to $45.8–$46.2B (+10–11%) and 34.3% non-GAAP margin.

Lowe’s Miss: Comparable sales rose 1.3%. Quarterly revenue increased 10.9% YoY to $20.6B (vs. $18.6B). GAAP EPS was $1.78; adjusted EPS came in at $1.98 (+2.6% YoY). Results included $149M in pre-tax acquisition-related expenses tied to FBM and ADG. The company returned $673M to shareholders via dividends during the quarter.

NVIDIA Beat: Record quarterly revenue of $68.1B, up 20% Q/Q and 73% Y/Y, driven by Data Center revenue of $62.3B (+22% Q/Q, +75% Y/Y). Returned $41.1B to shareholders, with $58.5B remaining under buyback authorization. GAAP EPS was $1.76; non-GAAP EPS was $1.62. Declared $0.01 dividend payable Apr 1, 2026 (record Mar 11). Q1 FY2027 revenue guided to ~$78.0B (±2%) with ~75% gross margins.

Intuit Beat: Total revenue was $4.7B, up 17% YoY. GBS rose 18% to $3.2B, led by Online Ecosystem at $2.5B (+21%). Consumer grew 15% to $1.5B; Credit Karma increased 23% to $616M; TurboTax added 12% to $581M. GAAP EPS climbed 49% to $2.48; non-GAAP EPS rose 25% to $4.15. The company repurchased $961M of stock, set a $1.20 quarterly dividend, and reiterated FY2026 guidance, with Q3 GAAP EPS of $10.56–$10.62 and non-GAAP EPS of $12.45–$12.51.

TJX Beat: Q4 comps rose 5% with net sales of $17.7B (+9% YoY). Adj EPS was $1.43 vs $1.39 est; GAAP EPS $1.58. Pretax margin 13.5% (12.2% adj); gross margin 30.9% (31.1% adj). Returned $4.3B in FY26; guiding $2.50–$2.75B buybacks in FY27. Board plans a 13% dividend hike to $0.48 (subject to approval). Q1 FY27 EPS seen at $0.97–$0.99; FY27 EPS $4.93–$5.02.

EARNINGS PREVIEW:

Date | Symbol | Name | Time |

3-Mar | AZO | Autozone | Before Open |

3-Mar | CRWD | Crowdstrike Holdings Inc | After Close |

3-Mar | ROST | Ross Stores Inc | After Close |

3-Mar | SE | Sea Ltd ADR | Before Open |

4-Mar | AVGO | Broadcom Ltd | After Close |

5-Mar | CNQ | Canadian Natural Resources | Before Open |

5-Mar | COST | Costco Wholesale | After Close |

5-Mar | MRVL | Marvell Technology Inc | After Close |

5-Mar | PBR | Petroleo Brasileiro S.A. Petrobras ADR | After Close |

VIDEO’s OF THE WEEK:

Wake up to better business news

Some business news reads like a lullaby.

Morning Brew is the opposite.

A free daily newsletter that breaks down what’s happening in business and culture — clearly, quickly, and with enough personality to keep things interesting.

Each morning brings a sharp, easy-to-read rundown of what matters, why it matters, and what it means to you. Plus, there’s daily brain games everyone’s playing.

Business news, minus the snooze. Read by over 4 million people every morning.

Please Share This Newsletter With Your Friends.

Also, check my blog here.

This newsletter's content is for informational and educational purposes only and should not be considered trading or investment recommendations. All the opinions in this newsletter are personal and do not belong to any organization.