In partnership with

Weekly Newsletter

IMF Projects Global Public Debt To Exceed $100 Trillion

Increased Term Premium And Bond Selloff

Why Mortgage Rates Went Up?

Length Of Economic Expansions

The Fed Beige Book Summary

Bizarre Goldman Sachs Forecast for S&P 500

QUOTE OF THE WEEK:

“If you look at EV companies worldwide, to the best of my knowledge, no EV company is even profitable. And to the best of my knowledge, there was no EV division of any company, of any existing auto company that is profitable. So it is notable that Tesla is profitable despite a very challenging automotive environment. And this quarter actually is a record Q3 for us.” Elon Musk - CEO, Tesla

KEY US ECONOMIC EVENTS NEXT WEEK:

Source: ForexFactory

MARKET CLOSE:

CNBC: EOD 10/25

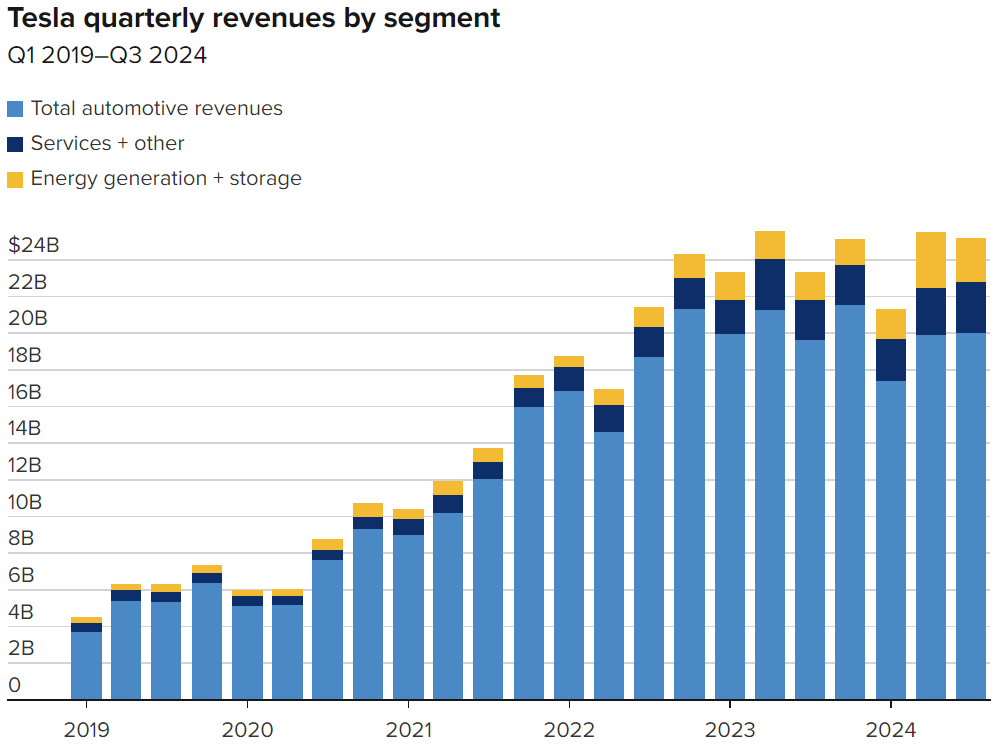

Good Afternoon. Just last week, I wrote about Elon Musk's potential to become the first trillionaire by 2027, and Tesla’s results this week moved him closer to that mark by over $30 billion with a ~22% stock surge.

Next week is action-packed with multiple key macro data releases and major earnings. I expect the data and earnings to continue to show a positive trend. Any weakness or miss will trigger a sharp reaction as markets are near timer highs, and the US election is very close, which should increase volatility. This week's Fed beige book reported moderating economic trends but no significant concerns. Check the curated insights section for more details.For the week:

The S&P 500 is down 0.96%, the Nasdaq is up 0.16%, and the Dow 30 is down 2.68%.

Source: barchart

CNN's Fear & Greed Index now stands at 59 (Greed) out of 100, down 16 points from last week. Details here

The top five trending stocks on Reddit are Tesla, SPY, Nvidia, QQQ, and Trump Media. Read More

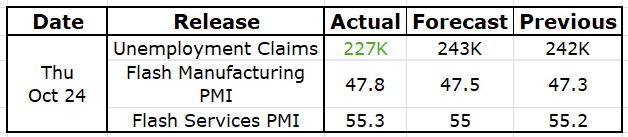

Here is a summary of this week’s key economic releases:

This week also, the overall macro data remained positive, showing the US economy's continued strength.

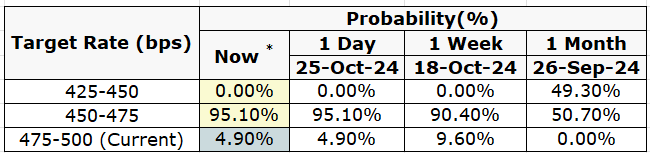

Target Rate Probabilities for Nov 7th FOMC Meeting:

CME FedWatch: * Data as of 26 Oct 2024 05:24:03 CT

The CME Fed watch probabilities show that the market still expects the Fed to cut rates by 25 basis points in the Nov 7th meetings despite good overall economic data. Next week’s inflation numbers and macro data will decide if this changes.

FRONT PAGES:

The U.S. recorded a $1.8 trillion budget deficit in fiscal 2024, an 8% increase from last year, marking the third-highest deficit on record. This gap persisted despite record tax receipts of $4.9 trillion, as spending reached $6.75 trillion. Read More

The IMF projects that global public debt will exceed $100 trillion by the end of 2024, amounting to about 93% of global GDP. This significant rise is largely driven by high spending in major economies like the U.S. and China, with public debt levels expected to approach 100% of global GDP by 2030. The current US debt to GDP ratio is 120%. Read More

The New York Federal Reserve warns that banks are obscuring risks in commercial real estate by extending loan terms to avoid recognizing distressed loans. This "extend-and-pretend" approach adds systemic risks. Read More

U.S. existing home sales hit a 14-year low in September, pressured by rising mortgage rates and home prices. The continuing drop points to deepening challenges in the housing market, which has struggled to recover as mortgage rates surged again this spring. Read More

Delta Air Lines filed a lawsuit against CrowdStrike in Georgia on Friday, alleging breach of contract and negligence after a July IT outage affected millions of computers and led to 7,000 flight cancellations. Read More

Waymo has completed a $5.6 billion funding round, its largest yet, to expand its robotaxi operations. The company plans to use the funds to grow its autonomous vehicle services in existing cities like San Francisco, Los Angeles, and Phoenix while also launching in new cities such as Austin and Atlanta, where its cars will be available through the Uber app. Read More

EARNINGS UPDATE:

Tesla's third-quarter earnings exceeded profit expectations, though revenue fell slightly short, leading to a stock boost on the profit beat and Musk’s forecast of at least 20% vehicle growth for next year. Read More

Source: CNBC

Verizon shares declined after third-quarter revenue and net income missed analysts' estimates, though adjusted profits slightly exceeded expectations after factoring in $2 billion in one-time costs. The company reaffirmed its full-year guidance despite the mixed results. Verizon reported adding only 349,000 net new postpaid connections, a significant drop from the previous year’s 581,000 and below analyst expectations of 510,000. This also suggests a slower start for the iPhone 16. Read More

Source: WSJ

ServiceNow surpassed its Q3 2024 guidance for all critical growth and profitability metrics and increased its full-year subscription revenue outlook, reflecting strong performance across the board. Read More

T-Mobile US surpassed expectations for quarterly wireless subscriber growth as more customers opted for its discounted plans, including streaming perks like Netflix. This strong customer growth is primarily fueled by T-Mobile’s competitive, high-speed 5G plans, often priced lower than AT&T and Verizon. Read More

Coca-Cola reported earnings and revenue that exceeded analysts' estimates on Wednesday, driven by price increases that helped offset weaker demand. Read More

EARNINGS PREVIEW:

Date | Symbol | Name | Time |

29-Oct | AMD | Adv Micro Devices | After Close |

29-Oct | GOOGL | Alphabet Cl A | Before Open |

29-Oct | GOOG | Alphabet Cl C | Before Open |

29-Oct | V | Visa Inc | After Close |

29-Oct | MCD | McDonald's Corp | Before Open |

29-Oct | NVS | Novartis Ag ADR | Before Open |

30-Oct | MSFT | Microsoft Corp | After Close |

30-Oct | META | Meta Platforms Inc | After Close |

30-Oct | LLY | Eli Lilly and Company | Before Open |

30-Oct | ABBV | Abbvie Inc | Before Open |

31-Oct | AAPL | Apple Inc | After Close |

31-Oct | AMZN | Amazon.com Inc | After Close |

31-Oct | LIN | Linde Plc | Before Open |

31-Oct | MA | Mastercard Inc | Before Open |

31-Oct | MRK | Merck & Company | Before Open |

31-Oct | SHEL | Royal Dutch Shell Plc ADR | Before Open |

1-Nov | CVX | Chevron Corp | Before Open |

1-Nov | BRK.B | Berkshire Hathaway Cl B | -- |

1-Nov | XOM | Exxon Mobil Corp | Before Open |

CURATED INSIGHTS:

Increased Term Premium And Bond Selloff:

The Fed started cutting rates on September 18th, but bond yields increased this month. Ideally, one would think that treasury yields should go down if the Fed cuts rates. Instead, as Bloomberg reported, the latest bond selloff (which pushes yields higher) was similar to the one observed in 1995. There is a lot of coverage this week in the media on this topic, from Bloomberg to the NY Times, so I thought of providing a summary analysis here.

Source: Bloomberg

The increase in bond yields can be attributed mainly to the increase in term premiums. The term premium is defined as the compensation that investors require for bearing the risk that interest rates may change over the life of the bond. The NY Fed estimates for the term premia turned positive in the second week of this month. It makes sense for investors to expect positive term premiums for long-term tenor bonds like 10 years due to future economic uncertainty. This premium was negative in the recent past, post-financial crisis, due to the excess liquidity pumped into the market or the central bank buying bonds, but it increased in the last two years due to higher inflation expectations and long-term fiscal concerns. Read More

Source: Bloomberg, NY Fed

There are three factors behind increased term premiums and, thereby, the bond selloff:

US Election Odds Favor Trump Win: Whether you look at Polymarket or Kalshi, the betting world is showing odds decisively (~ 60%) in favor of Trump's victory. In addition, the odds for Republicans sweeping all three, i.e., the Presidency, the Senate, and the House, are at 50%. No one can say for sure if the betting world knows for sure who wins. However, this trend increases concerns about higher fiscal deficits due to tax cuts and other Trump policies. A nonpartisan group has estimated that Trump's policies could add $7.5 trillion to U.S. Treasury debt over the next decade, more than double the projected increase under Harris's policies.

China Stimulus: China's stimulus announcement in late September and continued indication of more actions led to increased commodity prices recently, which affected the bond market due to an inflation scare.

Strong Economy: The US economy is doing well, and there is a strong feeling that the Fed achieved the soft landing. In addition, the Fed is expected to continue rate cuts into 2025 as the neutral rate (R*) is expected to be somewhat in the 3.5-4% range. So, the Fed cutting rates in the robust economy is expected to help corporate earnings and the economy. Historical data shows that the 10-year treasury yield generally tracks nominal GDP. Read More

Why Mortgage Rates Went Up:

On a related topic, in addition to the 10-year treasury yields, mortgage rates have also been up since the Fed cut rates in September. The main cause of this is the negative convexity of mortgage-backed securities. This means that when mortgage rates go down, people refinance; hence, the MBS holder just gets his principal back with no benefits. Hence, MBS always trades at a premium to the treasuries to compensate for negative convexity. As the treasury yields are higher, so are MBS, and if MBS investors require a higher yield, the mortgage rate will reflect that.Current Expansion Is Relatively Young:

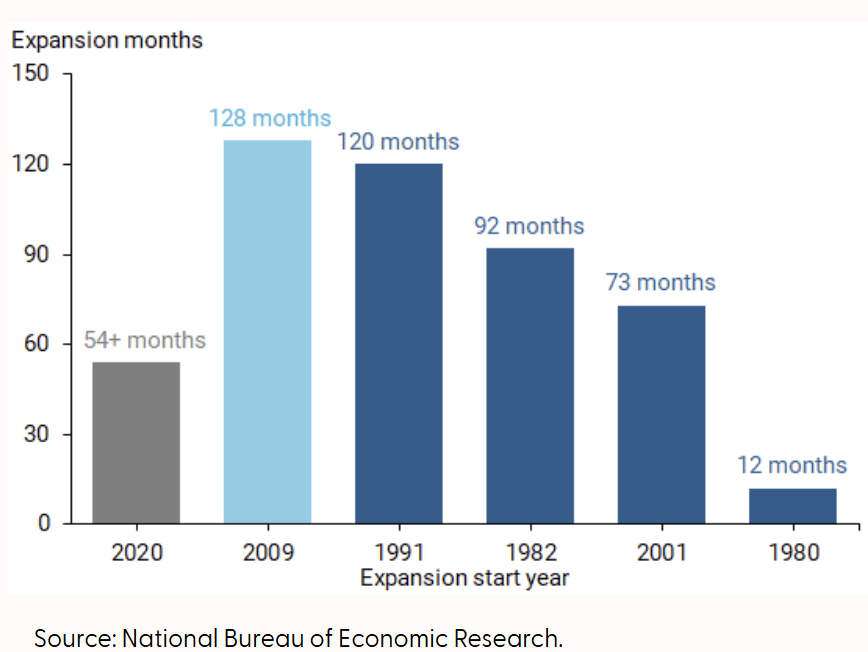

Mary Daly, the president and CEO of the Federal Reserve Bank of San Francisco, wrote this week about the current soft landing scenario and the future. According to her, the current economic expansion is relatively young, i.e., 54 months compared to recent history. History shows that sustainable expansion is possible. While at the Federal Reserve, she witnessed two of the longest U.S. economic expansions—the 1990s and the pre-pandemic period—where businesses thrived, jobs flourished, and gains in earnings and wealth were widely shared. The expansion before the pandemic, lasting nearly 11 years, showcased sustainable growth with low inflation, creating opportunities and reducing income inequality. Similar trends are emerging in the current expansion, with record-high labor force participation and narrowing wage gaps, further benefiting households and businesses. Read More

The Fed Beige Book Summary:

Economic activity remained unchanged across districts, with modest growth in only two districts.

Manufacturing activity declined, while banking saw steady growth and mixed loan demand due to falling interest rates.

Consumer spending was mixed with a shift toward less expensive alternatives, and housing market activity held steady despite mortgage rate uncertainty.

Commercial real estate markets were generally flat. Agricultural activity was flat to down modestly. Energy activity was also unchanged or down modestly.

Labor markets saw slight employment growth, reduced hiring demand, and easing wage pressures, though skilled worker shortages persisted.

Inflation moderated with slight price increases, but rising insurance and healthcare costs squeezed profit margins across several industries.

Bizarre S&P 500 Returns Predictions From Goldman Sachs:

I was surprised to see this week that Goldman Sachs released a report predicting the broad market index (S&P 500) will produce an annualized nominal total return of just 3% over the next 10 years. GS predicts that the equal weight of the S&P 500 index will give 8% returns in the same period, i.e., 5% more than the S&P 500. I listened to the Bloomberg interview with David Kostin, the Chief US Equity Strategist at Goldman Sachs, explaining this prediction. It was a waste of time, as he made many illogical arguments. Below are the reasons I think this GS prediction should not be taken seriously:First, the idea that one can predict 10-year returns for the index itself is impractical, as there are so many variables. Companies struggle to predict their earnings even two quarters out accurately.

GS says the S&P 500 index currently has too much concentration, and the equal-weight index will outperform as these top few companies are overvalued and the starting point is higher. The massive flaw in this argument is that GS seems to assume that the S&P 500 composition will remain the same for the next 10 years or have the same concentration as today. If the remaining 493 stocks perform well, their market cap will grow as investors rotate from underperforming prominent names, and the composition of the S&P 500 will change. As the composition changes, so do the ETFs like SPY, which are proxies for holding the S&P 500. So, if someone holds SPY, his exposure will shift to the new names according to weight in real-time.

David Kostin cited the historical trend behind this prediction: when the S&P 500 is concentrated, it underperforms in the next decade. I'm not sure which data he is citing as recent decades; I don't think this happened, and there is no reason to believe history will repeat itself. I wish predicting markets was as easy as just checking history.

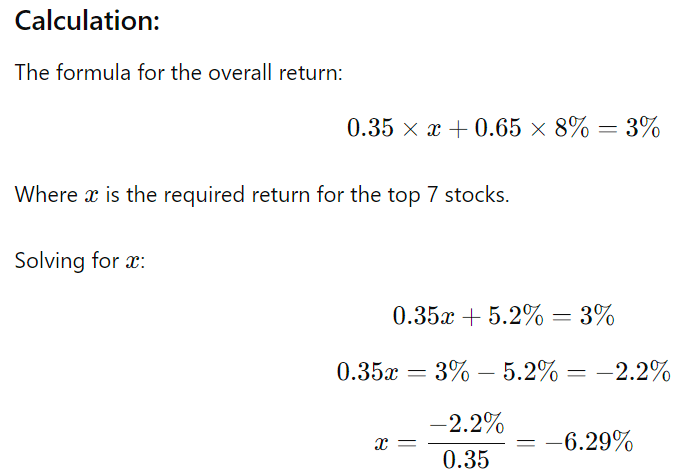

It's a fact that ~35% of the S&P 500 is concentrated in seven magnificent companies. These companies are world monopolies, have unique products, and are constantly innovating. How’s it logical to think these companies will underperform for a decade? I agree that the market can broaden in the future, but even in that case, the S&P 500 weightings will adjust, as I said above. Even for argument's sake, if you think the S&P 500 remains as it is, below is the calculation, which shows the top 7 stocks would need to underperform by approximately -6.29% for the overall S&P 500 return to be 3%, with an equal-weighted index return of 8% and top seven stocks representing 35% of the index. I just don’t see any reason for such underperformance for so long.

Given:Equal-weighted index return: 8%

Market-cap weighted index return: 3%

The top 7 stocks represent: 35% of the S&P 500 by weight

The remaining 493 stocks represent: 65% of the index

Maybe I am missing something, but based on facts and common sense, I really think I am not. I am surprised that a firm like Goldman Sachs can come up with something illogical like this. I do not believe in the GS prediction at all. I am not posting David Kostin’s Bloomberg interview here, so you don’t waste time watching it. Also, note that as the market broadens, the top seven concentration will fall from ~35%, and the lower it goes, the more underperformance will be needed from top companies to achieve 8% equal-weight returns. In short, this prediction doesn’t make any sense.

VIDEO’s OF THE WEEK:

We put your money to work

Betterment’s financial experts and automated investing technology are working behind the scenes to make your money hustle while you do whatever you want.

Subscribe to my Newsletter here.

Also, check my blog here.

This newsletter's content is for informational and educational purposes only and should not be considered trading or investment recommendations. All the opinions in this newsletter are personal and do not belong to any organization.