Weekly Newsletter

💸 First Rate Cut After Nine-Month Pause

💻 Nvidia Invests In Intel

🏦 US Banks Tap $1.5bn From SRF

📊 PCE Inflation Expectations For Next Week

📝 Key Points From FOMC Press Conference

QUOTE OF THE WEEK:

“Not only are you not seeing a huge push on inflation, you're not likely to see a huge push in consumer inflation expectations. And I will say people who trade inflation for a living—we're not seeing a movement in inflation expectations from those people either. So you know, the only people who seem to be worried about inflation in a material way are some Fed governors and economists on Wall Street.” - Drew Matus, chief market strategist at MetLife Investment Management.

KEY US ECONOMIC EVENTS NEXT WEEK:

MARKET CLOSE:

CNBC EOD 9/19

WEEKLY MARKET WRAP:

Good Afternoon. Another positive week for the markets with continued good macro data and an expected Fed rate cut. S&P 500 and Nasdaq hit fresh record highs on Friday. The most important thing to note was the SEP DOT plot, which inferred two more rate cuts this year. Jerome Powell called this a risk management cut to account for a cooling labor market based on the recently revised job numbers.

It was a quiet week for earnings, with FedEx being the only major company to report, and it beat expectations.

Below are the key things to note this week:

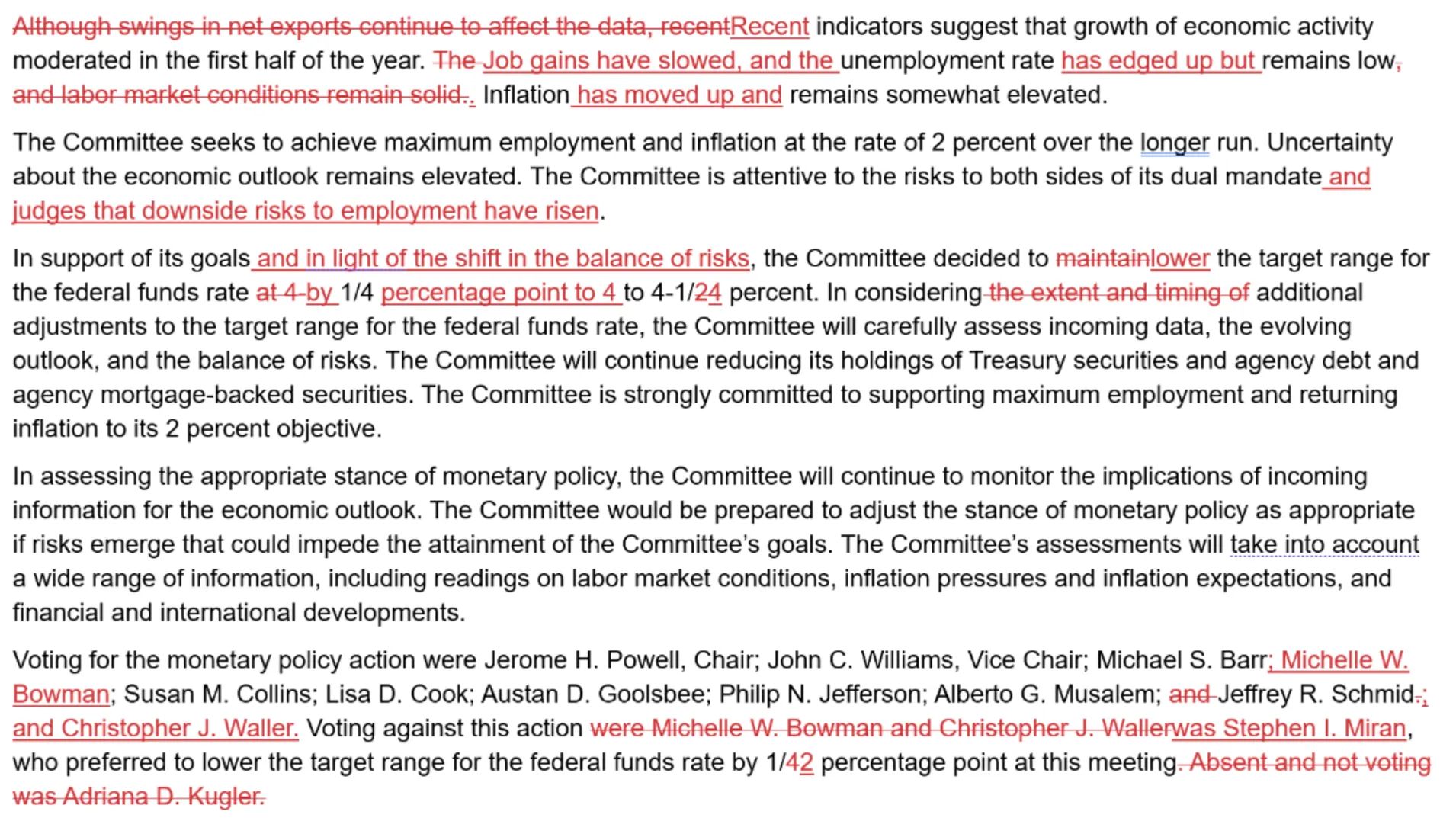

FOMC Statement Changes From Last Meeting:

PCE Next Week: The Fed’s preferred inflation gauge, the PCE, is expected next Friday. It is expected to be at ~2.8% YoY for the headline number and ~2.9% for Core. These projections are not concerning, and if PCE comes in line with this, it will be good news for markets. Tariffs are expected to cause a one-time price adjustment by year's end; however, I provided my analysis last year as to why the inflation is headed down.

For the week:

The S&P 500 is up 1.22%, the Nasdaq is up 2.21%, and the Dow 30 is up 1.05%.

Barchart

CNN's Fear & Greed Index now stands at 62 (Greed) out of 100, up 8 points from last week. Details here

The top five trending stocks on Reddit are Oklo, SPY, Opendoor, Adaptimmune Therapeutics, and Nvidia. Read More

Here is a summary of this week’s key economic releases:

Target Rate Probabilities for October 29th FOMC Meeting:

CME FedWatch

CURATED INSIGHTS & ANALYSIS:

FOMC Press Conference:

Below are the key points from the FOMC press conference:Fed cut rates 25 bps to 4.00–4.25% while continuing balance sheet runoff.

Growth cooled to ~1.5% in H1; SEP revised slightly higher to 1.6% (2025) and 1.8% (2026).

Job gains collapsed from 150k/month at the last meeting to just 29k/month over the past three months — a decisive signal of labor market cooling.

Powell described a “curious balance” in labor supply and demand: both have slowed sharply, with demand now falling faster.

Unemployment edged up to 4.3%; wage growth is moderating but still above inflation.

Inflation stuck above target: PCE 2.7%, core PCE 2.9%. SEP shows 3.0% (2025), easing to 2.1% by 2027.

Tariffs are driving goods inflation; Powell called it mostly one-time but warned persistence is a risk.

Fed now sees two-sided risks: inflation skewed up, employment skewed down — prompting a shift toward neutral.

SEP dots imply rates at 3.6% end-2025, 3.4% in 2026, 3.1% in 2027 — 25 bps below June.

AI may be suppressing entry-level hiring, but Powell said it’s not the main drag.

Housing is burdened by high rates but constrained more by structural shortage.

Consumer stress rising: defaults inching up in cards and loans, but not systemic.

Powell dismissed the risk of asset bubbles, stating that stability vulnerabilities are not elevated.

Independence reaffirmed — decisions remain data-driven despite political noise.

Policy not on autopilot; Fed is strictly meeting-to-meeting.

The FOMC DOT Plot shows the future projections of its members. The outlier in the first column is from the new Trump-nominated Fed Governor Stephen Miran, who prefers the rate to be between 2.75-3% by year's end. He will provide a detailed analysis of this view next week.

FRONT PAGES:

Rate Cut: The Fed cut rates Wednesday for the first time since December and signaled more to come this year. Policymakers delivered a quarter-point cut in line with Wall Street expectations. Stocks briefly rose on the news before sliding across all three major indexes. Read

Funding Pressure: U.S. banks tapped $1.5 billion from the Fed’s Standing Repo Facility on Monday, coinciding with corporate tax payments and Treasury settlements, signaling some funding tightness. The SRF, created in July 2021, provides overnight cash against collateral such as Treasuries to backstop shortages. Read

Nvidia Invests in Intel: Nvidia said Thursday it will buy $5 billion of Intel’s common stock, joining the list of major shareholders just weeks after the US government took a 10% stake. Read

EARNINGS UPDATE:

FedEx Beat: FedEx reported adjusted EPS of $3.83 on $22.2 billion in revenue, topping expectations of $3.63 on $21.7 billion. For the year, it sees 4%–6% revenue growth versus the 1% projected by Wall Street, with adjusted EPS between $17.20 and $19. The $18.10 midpoint is close to analysts’ $18.36 forecast.

EARNINGS PREVIEW:

Date | Symbol | Name | Time |

23-Sep | AZO | Autozone | Before Open |

23-Sep | MU | Micron Technology | After Close |

24-Sep | CTAS | Cintas Corp | Before Open |

25-Sep | ACN | Accenture Plc | Before Open |

25-Sep | COST | Costco Wholesale | After Close |

30-Sep | NKE | Nike Inc | After Close |

30-Sep | PAYX | Paychex Inc | Before Open |

VIDEO’s OF THE WEEK:

Please Share This Newsletter With Your Friends.

Also, check my blog here.

This newsletter's content is for informational and educational purposes only and should not be considered trading or investment recommendations. All the opinions in this newsletter are personal and do not belong to any organization.