The worst week for the S&P 500 since 2023.

Updates on the overall weak macro data releases.

US regulators are expected to announce bank capital rule revisions.

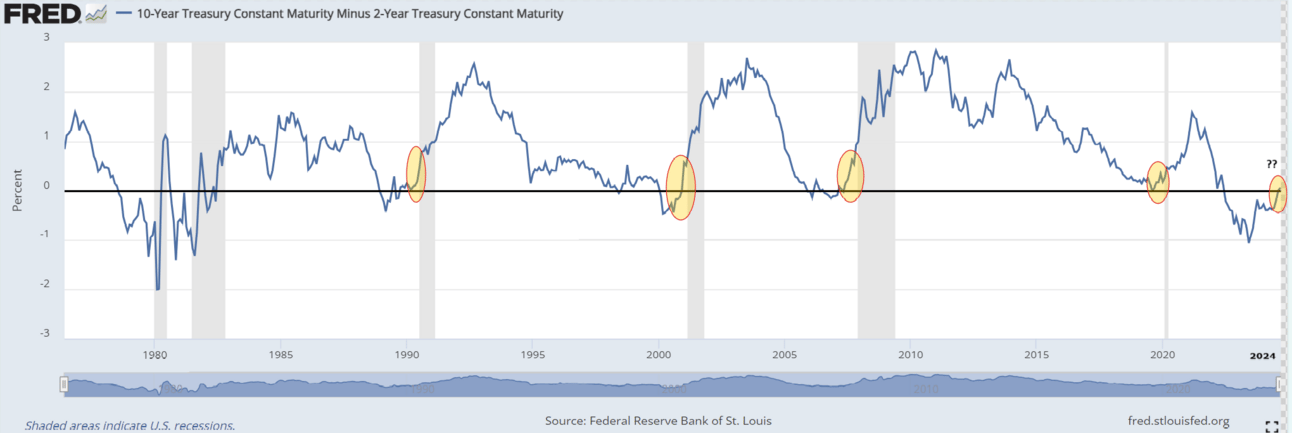

Yeild curve dis-invertes.

The Federal Reserve's Beige Book shows declining US economic activity.

Rate cuts: Initial expectations vs outcome.

Market returns after the first rate cut.

QUOTE OF THE WEEK:

“Considering the achieved and continuing progress on inflation and moderation in the labor market, I believe the time has come to lower the target range for the federal funds rate at our upcoming meeting,” Fed Governor Christopher Waller.

AFTER HOURS:

Source - CNN

KEY US ECONOMIC EVENTS NEXT WEEK:

Source - Forex Factory

MARKET CLOSE:

EOD Sept. 6th - CNBC

Good Afternoon. Last week, I talked about the September seasonality. The first week of this month lived up to that reputation, as the S&P 500 posted the worst week since 2023, and the Nasdaq posted the worst week since 2022.

For the week:

The S&P 500 is down 3.28%, the Nasdaq is down 4.71%, and the Dow 30 is down 2.39%.

Source - Barchart

CNN's Fear & Greed Index moved from Greed to Fear and now stands at 39 out of 100, a drop of 24 points from last week. Details here

The top five trending stocks on Reddit are Nvidia, SPY, Broadcom, Tesla, and QQQ. Read More

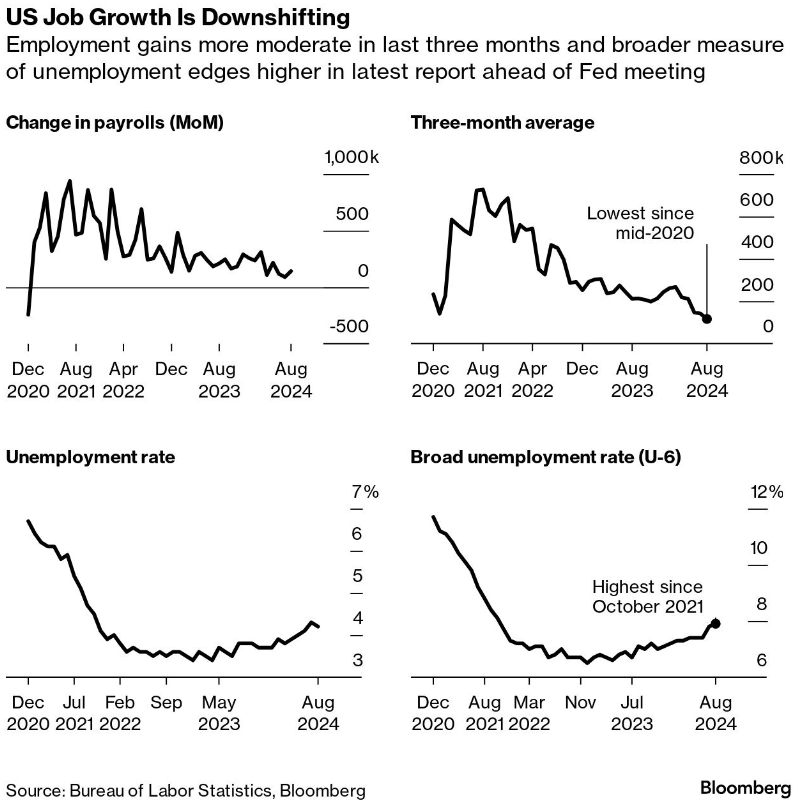

The key macro data released this week confirms that the economy, especially the labor market, is slowing. Below is the summary -

The U.S. ISM manufacturing PMI edged up 0.4 pts to 47.2 in August. While that’s the first increase in five months, the gauge has held below the 50 mark (indicating shrinking activity) for most of the past two years.

JOLTS job openings came below forecast (7.67M), its lowest reading since April 2021.

Non-farm employment change (both ADP and Government data) came below forecast.

The US economy added 142,000 jobs in August, below the average economist estimate of 164,000. The unemployment rate was in line with consensus at 4.2%, a slight drop from 4.3% last month.

The ISM services PMI (51.5) shows that the service sector is still doing slightly better. Also, average hourly earnings came in better than forecast, indicating that the last leg of the inflation fight may take longer.

FRONT PAGES:

Apple is set to unveil its latest iPhone, featuring the A18 chip powered by Arm's advanced V9 chip design, at an event on September 9th. Arm had said in July that its V9 chip accounts for 50% of smartphone revenue. Arm owns the intellectual property behind the computing architecture for most of the world's smartphones, which it licenses to Apple and many others. Read More

The U.S. Federal Reserve and other regulatory bodies are set to propose significant revisions to banking capital regulations, potentially announcing changes as early as September 19, 2024. These revisions may reduce capital requirements for certain business segments and lessen market-risk standards for large banks, addressing previous opposition to the stricter "Basel III Endgame" proposal. Read More

OPEC+ has agreed to extend its crude oil production cuts into 2025, gradually phasing out 2.2 million barrels daily from October 2024 to September 2025 to support market stability. Oil prices have declined this year despite continued output cuts and ongoing geopolitical tension in the Middle East. Read More

Federal Reserve Governor Christopher Waller has expressed support for an interest rate cut at the upcoming September meeting, citing progress in managing inflation and a cooling labor market. Read More

Dell and Palantir shares rose in extended trading after the announcement that they’re being added to the S&P 500. Read More

EARNINGS UPDATE:

Broadcom reported strong fiscal third-quarter results, exceeding Wall Street's expectations for both revenue and earnings. CEO Hock Tan announced that Broadcom expects to generate $12 billion in revenue from AI components and custom chips in fiscal 2024. Read More

Zscalaler reported stronger-than-expected results but provided weak guidance for the first half of FY25. Read More

HP Enterprise reported strong results. The company posted record AI revenue of $1.3 billion, up 39% from the previous year. On the earnings call, the company highlighted its strong partnership with Nvidia. Read More

EARNINGS PREVIEW:

Date | Symbol | Name | Time |

9/9/2024 | ORCL | Oracle Corp | -- |

9/12/2024 | ADBE | Adobe Systems Inc | After Close |

9/12/2024 | LEN | Lennar Corp | -- |

9/12/2024 | KR | Kroger Company | Before Open |

CURATED INSIGHTS:

Yield curve dis-inverted:

The bond market's yield curve briefly returned to a normal state on September 4, 2024, with the 10-year Treasury yield surpassing the 2-year yield for the first time since June 2022. While the normalization of the yield curve might seem positive, historically, it often occurs before or during a recession, as the Federal Reserve typically cuts rates in response to a slowing economy.Out of the six recessions the U.S. has faced since 1980, five were preceded by a yield-curve inversion of at least 20 days. Historically, recessions have occurred between 6 and 24 months after the yield curve was inverted. This time, the yield curve was inverted for a record 26 months, and there is still no recession. This puts the yield curve's ability to predict recession in question. Historically, recession followed in the short term when the yield curve dis-inverters (after a long period of inversion). As discussed earlier, macro data still suggests that the US economy is slowing, but there are no apparent signs of a recession. Hence, maybe history won’t repeat this time, but this is something to keep a close watch on in the short term.

Check the chart below. Grey-shaded areas indicate US recessions, and dis-inversions are highlighted in yellow ovals. Read More

Yield Curve Dis-Inversion: Yellow highlighted the last four recessions

The Beige Book:

The Fed’s Beige Book, published on September 4th, shows declining US economic activity. This report is based on information collected on or before August 26, 2024. Below is the summary:

The number of districts reporting flat or declining activity rose to nine, up from five in the prior period.

Economic activity grew modestly in three districts (out of twelve): Boston, Chicago, and Dallas.

Manufacturing slowed in most districts. Most districts reported softer home sales.

Employment levels were mainly flat to slightly up. Due to economic uncertainty, some firms reduced shifts and hiring, leading to modest wage growth overall, while skilled workers and union members experienced stronger increases.

Prices increased modestly in the most recent reporting period, with three districts noting only slight increases in selling prices, while non-labor input costs were generally easing.

The Beige Book Activity Index slipped into red in August but isn’t in recession territory -

Source: Oxford Economics, Bloomberg

Rate Cuts: Investors’ Expectations Versus Outcomes:

Fed Funds Futures price 225-250 bps of rate cuts between now and mid-2026. CME Group’s analysis published this week shows that investors were spot on in anticipating the magnitude of rate cuts in soft landing scenarios like 1995 and 2019. However, when the economy tipped into a recession, as was the case in 1990-91, 2001, and 2008-09, the markets’ initial pricing underestimated the ultimate breadth of policy easing by anywhere from 400 bps to 625 bps. Read MoreMarket returns after first rate cut:

Of the 14 rate cycles since 1929, 12 saw positive S&P 500 returns for the 12 months following the first rate cut.

The only two cycles with negative returns were after the dot-com bust in 2001 and the housing market crash in 2007. In both cases, the first-rate cut was 50bp. So, if the Fed feels the need to cut rates by 50bp on September 18th, it may be bad news for the economy and markets.

Source: Charles Schwab, Bloomberg, and the Federal Reserve.

VIDEO’s OF THE WEEK:

Subscribe to my Newsletter here.

Also, check my blog here.

This newsletter's content is for informational and educational purposes only and should not be considered trading or investment recommendations. All the opinions in this newsletter are personal and do not belong to any organization.