In partnership with

Weekly Newsletter

📦 Takeaways from Retail Earnings

💬 Powell Hints at September Rate Cut

📅 Next Week: Nvidia and PCE

🏛️ Changes to the Fed’s Goals and Strategy

🏭 Strong Manufacturing and Services PMI

💵 The US Dollar and International Stock Returns

📑 Key Points from FOMC Meeting Minutes

QUOTE OF THE WEEK:

“But they have to be careful because they can't give up the fight on inflation. Inflation is going to be moving up higher. Yes, their interpretation is that those are one-offs, but they're one-offs only if the Fed does the right thing with monetary policy. Those one-off changes in higher prices—a price level change—can become inflationary if the Fed allows it to happen. So again, they're going to have to be balancing both sides of the mandate. And that's why they're going to have to be very careful”. Fmr. Cleveland Fed President Loretta Mester

KEY US ECONOMIC EVENTS NEXT WEEK:

MARKET CLOSE:

CNBC EOD 22nd Aug

WEEKLY MARKET WRAP:

Good Afternoon. A volatile week for the markets, but it ended positively for major indices (except the Nasdaq), thanks to Jerome Powell's speech at Jackson Hole, which provided a clear indication of a September rate cut.

Below are the key things to note this week:

Jackson Hole: As expected, the Fed chair used his Jackson Hole address to give a hint of what to expect in the September FOMC meeting. He clearly shifted his focus to the weakening labor market, mentioning that inflation is essentially under control and the balance of risk has shifted more to the labor market — more on this in the curated insights section.Retail Earnings: Three key takeaways from the retail earnings are:

Walmart met revenue estimates but missed EPS. This indicates that the company is absorbing the tariff cost and incurring a loss on already low margins, rather than passing the burden to the consumer. However, Walmart noted that as its pre-tariff inventory depletes, its costs are increasing every week, and eventually, some of these costs will be passed on to the consumer.

Low-cost retailer TJX reached an all-time high due to its strong results. This highlights that consumers are seeking bargains and spending money at discount stores to mitigate the impact of consistently higher-than-expected inflation, which exceeds the 2% Fed target.

Home Depot reported that consumers are avoiding large projects due to the uncertain economic environment and higher rates.

PMI Data:

US business activity accelerated in August, with flash PMI showing the fastest growth this year, signaling a strong Q3. Both manufacturing and services expanded, while hiring rose sharply. Job creation hit one of the highest levels in three years, alongside the most considerable backlog of uncompleted work since May 2022.

Source: S&P

Next Week:Nvidia Earnings:

NVIDIA is set to report earnings on Wednesday after the close. As usual, won’t be surprised if it beats consensus estimates, especially after clearing some of its H-20 inventory, which got sold to Chinese clients. Recently, the Chinese Government has cracked down on the sale of H20 chips, but I don’t expect it to impact last quarter's results. The options market expects 6% move in Nvidia's stock price in either direction post earnings.

Reuters

PCE Inflation: The Fed’s official inflation gauge, the PCE, is set to be released next week. The Cleveland Fed forecasts the headline PCE at 2.6% and the core at 2.9%. In my opinion, the PCE should not exceed this level, and markets won’t be surprised if the actual numbers come within ±0.1 % of these projections.

For the week:

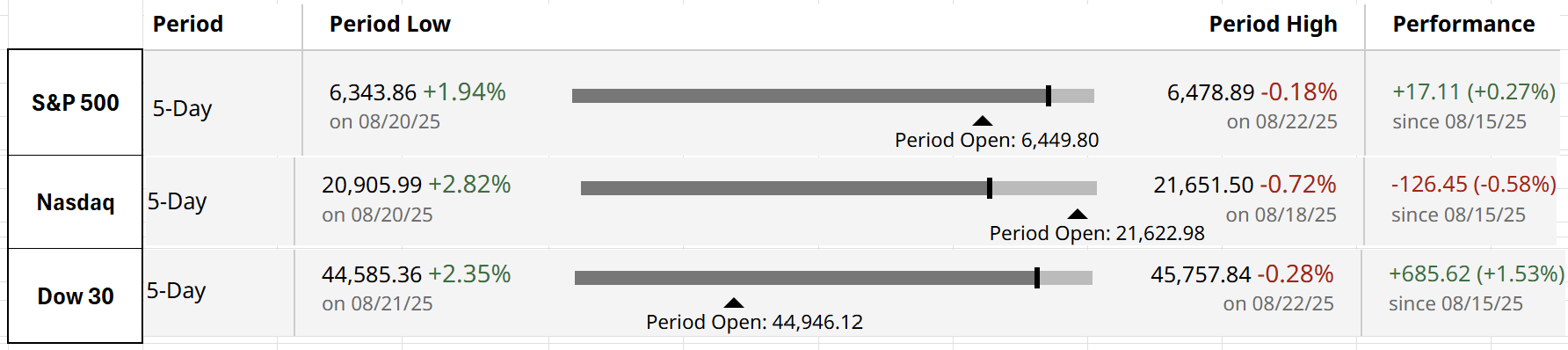

The S&P 500 is up 0.27%, the Nasdaq is down 0.58%, and the Dow 30 is up 1.53%.

Source: Barchart

CNN's Fear & Greed Index now stands at 61 (Greed) out of 100, down 3 points from last week. Details here

The top five trending stocks on Reddit are OpenDoor, SPY, Nvidia, Intel, and Tesla. Read More

Here is a summary of this week’s key economic releases:

Target Rate Probabilities for September 17th FOMC Meeting:

CME FedWatch

CURATED INSIGHTS & ANALYSIS:

Key Points from Jerome Powell's Speech:

Economy:GDP growth slowed to 1.2% in H1 2025, compared to 2.5% in 2024, primarily due to weaker consumption.

Tariffs, immigration curbs, and policy shifts are reshaping supply and demand.

The policy rate is 100 bps closer to neutral, allowing for cautious adjustments.

Inflation:

Headline PCE 2.6%, core PCE 2.9% as of July, lifted by tariffs.

Goods prices rose 1.1% YoY after 2024 declines; housing inflation is easing.

Tariff impact is seen as a one-time level shift; expectations remain anchored.

Labor Market:

Payroll growth slowed to 35k/month vs. 168k/month in 2024 after revisions.

Unemployment is 4.2%, a historically low rate, with softer quit rates, vacancies, and wage growth.

Immigration slowdown cut labor supply; participation has edged down—Labor Market is in a “curious balance”—stable but fragile.

Changes to the Fed Strategy:

ELB De-emphasized: No longer treated as a defining constraint, though still monitored.

No More Average Inflation Targeting: The 2020 “makeup” strategy is dropped; the framework reverts to flexible inflation targeting with anchored expectations at its core.

Employment Language Revised: “Shortfalls” replaced with “deviations,” clarifying that employment can run above real-time estimates of maximum employment if consistent with price stability, while still allowing preemptive action when risks arise.

US Dollar & International Stocks:

I have previously discussed the impact of foreign exchange movements on investments, but primarily in the context of gold’s historical performance in emerging markets. Recently, a Johnson Financial Group article talked about the US vs. international stock performance in relation to the U.S. dollar.

Dark blue above 0% indicates that US equities are outperforming international stocks, while light blue above 0% signifies dollar strength versus other currencies. A dark blue below 0% indicates that international equities outperformed. Notice that both series typically move together—either above or below the 0% line. Read the full article for YTD analysis of all major markets. For example, for US investors, Japanese stock market returns are 10 times those of the local investors (10% vs 1%).

Key Points From FOMC Meeting Minutes:

The most important thing to note from the FOMC meeting minutes is the staff’s economic projections, which clearly show why Jerome Powell’s speech this week emphasized the labor market more.

GDP Growth: Projection broadly unchanged from June; weaker spending data and smaller immigration boost offset slightly more supportive financial conditions. Growth expected to remain subdued through 2027.

Labor Market: Unemployment rate projected to rise above its natural rate by year-end and stay above through 2027, reflecting expected labor market weakening.

Inflation: The forecast has been revised slightly lower due to smaller tariff effects. Tariffs are expected to raise inflation in 2025–26, but are projected to decline to 2% by 2027.

FRONT PAGES:

US Buys Intel: The U.S. government will invest $8.9B in Intel common stock, giving the Trump administration about a 10% stake in the struggling chipmaker, Intel, and the president announced Friday Read

Fed Changes Strategy: The Fed ended its policy of letting inflation run above the 2% target after periods of low price growth, revising its long-run strategy Friday. Read

New products from Meta: New Smart Meta will unveil two new smart glasses at its Connect conference in September, including its first consumer-ready model with a display and wristband for hand gesture control. Codenamed Hypernova, the glasses feature a right-lens display and will sell for approximately $800, according to EssilorLuxottica. Read

Powell hinted at a rate Cut: Powell gave a cautious signal on potential rate cuts, citing uncertainty that complicates the implementation of monetary policy. With policy still restrictive, he said shifting risks may justify adjusting the stance. He also emphasized Fed independence while sidestepping White House pressure for cuts. Read

JPMorgan Chase Fined: JPM will pay $330M to settle claims it aided transactions tied to Malaysia’s 1MDB scandal, one of the century’s most significant financial crimes. Malaysia had sued the bank’s Swiss unit over $800M in 1MDB payments to a fraudulent JV. Two PetroSaudi businessmen were later convicted of fraud, mismanagement, and money laundering in a Swiss court. Read

EARNINGS UPDATE:

Primal Thesis

Palo Alto Beat: Palo Alto Networks reported Q4 results with adjusted EPS of $0.95 on $2.5B revenue, up 16% YoY. Product revenue rose 19% to $573.9M, while subscription and support grew 15% to $1.96B. Next-gen security ARR reached $5.6B, above estimates. Deferred revenue stood at $6.3B, and remaining performance obligations totaled $15.8B. Analysts had expected EPS of $0.89 on $2.5B revenue.

Home Depot Miss: Home Depot reported Q2 revenue up 4.8% YoY to $45.3B, with comps rising 1.0% vs. 1.4% expected, including a 40 bps FX drag. Comparable transactions fell 0.4%, while average ticket rose 1.4%; total transactions declined 0.9% to 446.8M, and total average ticket rose 1.2% to $90.01. Adjusted operating income was $6.69B with a 14.8% margin vs. 15.3% last year. The cost of sales rose 4.8% to $ 30.1 billion. Adjusted EPS came in at $4.68 vs. $4.67 last year. CFO noted consumers favor smaller projects amid higher rates.

Medtronic Beat: MDT raised its FY25 earnings outlook after stronger Q1 results and a lower tariff hit. It now guides diluted non-GAAP EPS to $5.60–$5.66, up from $5.50–$5.60, versus $5.55 consensus. The tariff impact is reduced to $185M from $200M to $350M. The company reiterated its FY26 organic revenue growth of ~5% and announced two new independent directors, alongside strategic changes, as Elliott Investment Management became a major shareholder.

TJX Beat: TJX reported Q2 revenue of $14.4B, up 6.9% YoY, with comparable sales rising 4% vs. 3.1% expected. Marmaxx comps rose 3%, HomeGoods 5%, Canada 9%, and International 5%. The company raised guidance, now expecting FY comparable sales growth of 2–3% and EPS of $4.52–$4.57 (midpoint $4.545) vs. $4.34–$4.43 prior and $4.49 consensus. Forward P/E stands at 29.88, rising to 31.68 in 2025.

Lowe’s Beat: Lowe’s raised full-year guidance and closed its $1.3B ADG acquisition. Q2 comparable sales rose 1.1% vs. 1.3% expected, with revenue up 1.6% to $23.96B. Gross margin improved 30 bps to 33.8%, while operating income was 14.5% of sales vs. 14.6% last year. Non-GAAP EPS came in at $4.33 vs. $4.24 consensus and $4.10 a year ago. The company also paid $645M in dividends.

Analog Devices Beat: Analog Devices reported Q3 earnings of $2.05 per share, topping the $1.95 estimate, with revenue up 24.6% to $2.88B, above forecasts. Management cited strong demand, backlog growth, and robust industrial bookings despite geopolitical uncertainty. Q4 guidance of $2.12–$2.32 EPS and $2.9B–$3.1B revenue exceeds estimates. The board declared a $0.99 dividend, payable on September 16 to holders of record as of September 2.

Intuit Beat: Intuit reported Q4 non-GAAP EPS of $2.75 on revenue of $3.83B, up 20% Y/Y. For FY26, it guided revenue of $21.0–$21.2B (12–13% growth), GAAP operating income of $5.8–$5.9B (17–19%), non-GAAP operating income of $8.6–$8.7B (14–15%), GAAP EPS of $15.49–$15.69 (13–15%), and non-GAAP EPS of $22.98–$23.18 (14–15%).

Workday Beat: Workday reported Q2 results above expectations, with adjusted EPS of $2.21 vs. $2.11 expected and revenue up 13% YoY to $2.35B, including $2.17B from subscriptions and $179M from services. The subscription backlog rose 18% to $ 25.37 billion. FY subscription revenue is guided to $8.82B, slightly above estimates, supported by the Paradox acquisition. The adjusted operating margin forecast was raised to 29% from 28%.

Walmart Mixed: Walmart reported Q2 revenue of $177.4B, up 4.8% Y/Y, with non-GAAP EPS of $0.68. The company raised its FY26 outlook for net sales growth to 3.75–4.75% and EPS to $2.52–$ 2.62, while maintaining its operating income guidance unchanged at 3.5–5.5%. Global eCommerce sales rose 25%, advertising 46%, and membership income 15.3%. Gross margin improved 4 bps, led by Walmart U.S.

EARNINGS PREVIEW:

Date | Symbol | Name | Time |

25-Aug | BHP | Bhp Billiton Ltd ADR | -- |

25-Aug | PDD | Pdd Holdings Inc | -- |

26-Aug | BMO | Bank of Montreal | Before Open |

26-Aug | BNS | Bank of Nova Scotia | Before Open |

27-Aug | CRWD | Crowdstrike Holdings Inc | After Close |

27-Aug | NVDA | Nvidia Corp | After Close |

27-Aug | RY | Royal Bank of Canada | Before Open |

28-Aug | TD | Toronto Dominion Bank | Before Open |

29-Aug | BABA | Alibaba Group Holding ADR | Before Open |

3-Sep | CRM | Salesforce Inc | After Close |

VIDEO’s OF THE WEEK:

6 free tools to communicate better at work

Smart Brevity is built to fix inbox — and information — overload. Its science-backed methodology can take any communication from confusing to clear.

Unlock our free resources on the communication…

Method that makes work more efficient

Tactic that hooks busy readers

Format that structures sharper updates

Start making every word work harder so your readers don’t have to.

Please Share This Newsletter With Your Friends.

Also, check my blog here.

This newsletter's content is for informational and educational purposes only and should not be considered trading or investment recommendations. All the opinions in this newsletter are personal and do not belong to any organization.