Weekly Newsletter

📊 Key Points From Nvidia Results

📈 In Line PCE Inflation With Strong GDP Growth

💡 Q2 Earnings Recap – Small Cap Outperformance

🏦 Required Banking Reserve Level Estimates

🤖 Alibaba Enters AI Race

🪙 More Alt-Coin ETFs

QUOTE OF THE WEEK:

“They're (Hyperscalers) spending hundreds of billions of dollars a year in CapEx. And these companies are not idiots. They're not spending this money with no visibility for a return or profitability. I think we're already starting to see adoption and returns on AI. And you have to remember also for some of these guys, it's also existential, right? The idea is if we don't continue to invest in this, the world is going this way. Like, we may be out of business if we don't. And so I think they keep spending.” - Stacy Rasgon, Bernstein semiconductor analyst

KEY US ECONOMIC EVENTS NEXT WEEK:

MARKET CLOSE:

CNBC EOD 29th Aug

WEEKLY MARKET WRAP:

Good Afternoon. Markets ended the week flat this week with good news on inflation and tech earnings continue to support.

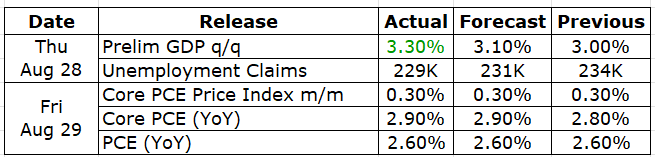

Below are the key things to note this week:Inflation: The most critical PCE inflation gauge, the Fed’s preferred measure, came exactly in line with the consensus estimates as I mentioned last week.

GDP:

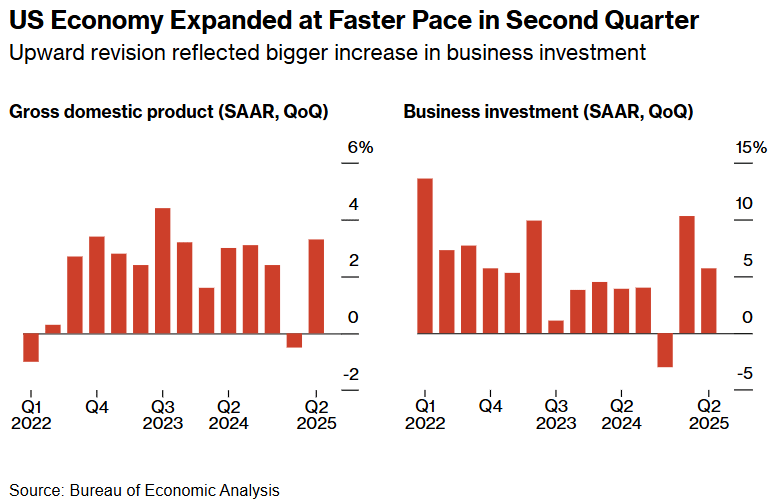

Us economy continues to do well. US GDP grew at a 3.3% annualized pace in Q2, driven by stronger business investment (5.7%) and trade, while consumer spending slowed to 1.6%. Core PCE rose 2.5%, with the Fed watching for tariff-driven inflation.Nvidia Results:

Nvidia reported good results with slight miss on data center revenue. Check the curated insights section for the key points from the earnings call.Governor Wallace Comments on Rate Cut:

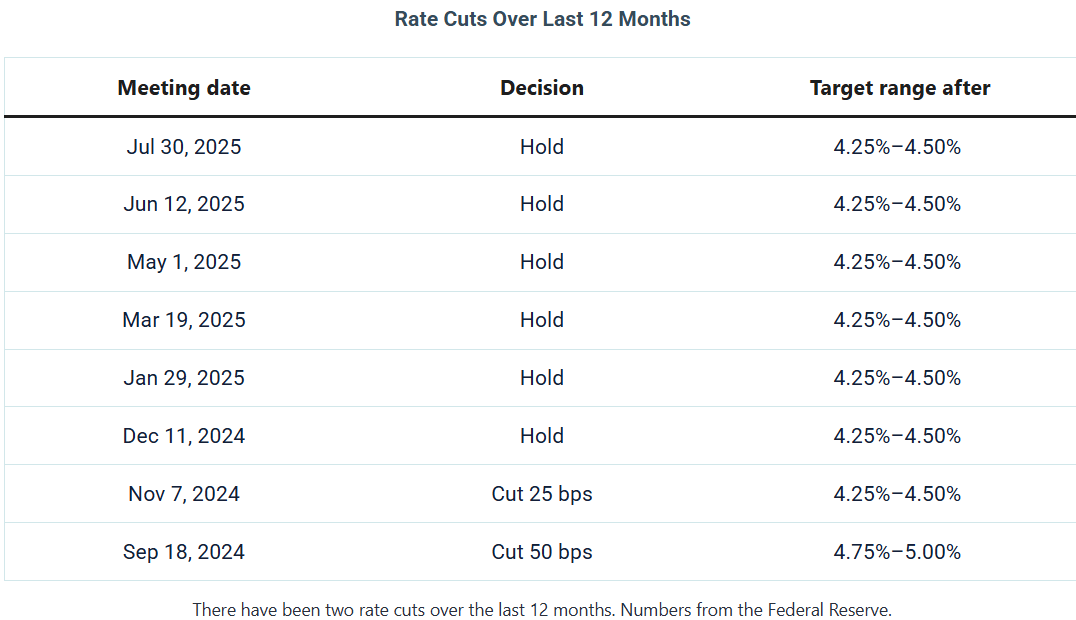

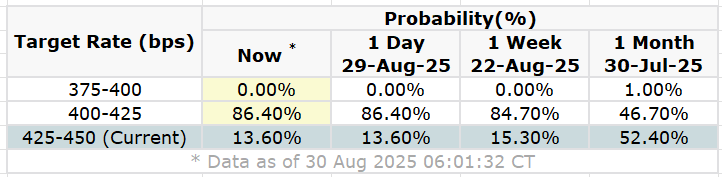

Fed Governor Christopher Waller said he supports rate cuts starting in September, with the pace guided by data. He had pushed for cuts in July and is now more confident it was the right call. September rate cut seems done deal now especially after recent comments from Powell as well as this week’s in line PCE data.

ValueWalk

For the week:

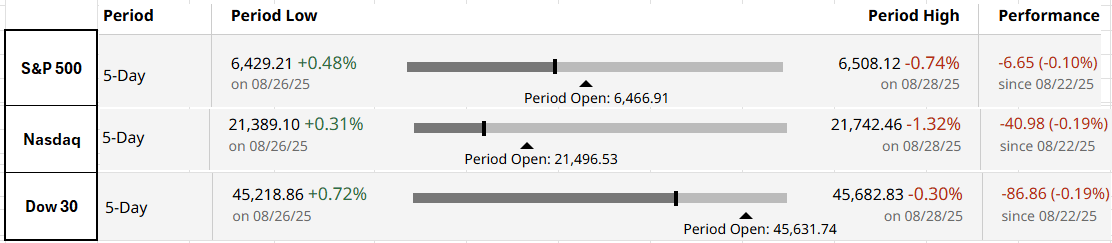

The S&P 500 is up 5.27%, the Nasdaq is up 7.15% %, and the Dow 30 is up 3.41%.

CNN's Fear & Greed Index now stands at 64 (Greed) out of 100, up 3 points from last week. Details here

The top five trending stocks on Reddit are Nvidia, SPY, OpenDoor, Tesla, and Alibaba. Read More

Here is a summary of this week’s key economic releases:

Target Rate Probabilities for September 17th FOMC Meeting:

CME FedWatch

CURATED INSIGHTS & ANALYSIS:

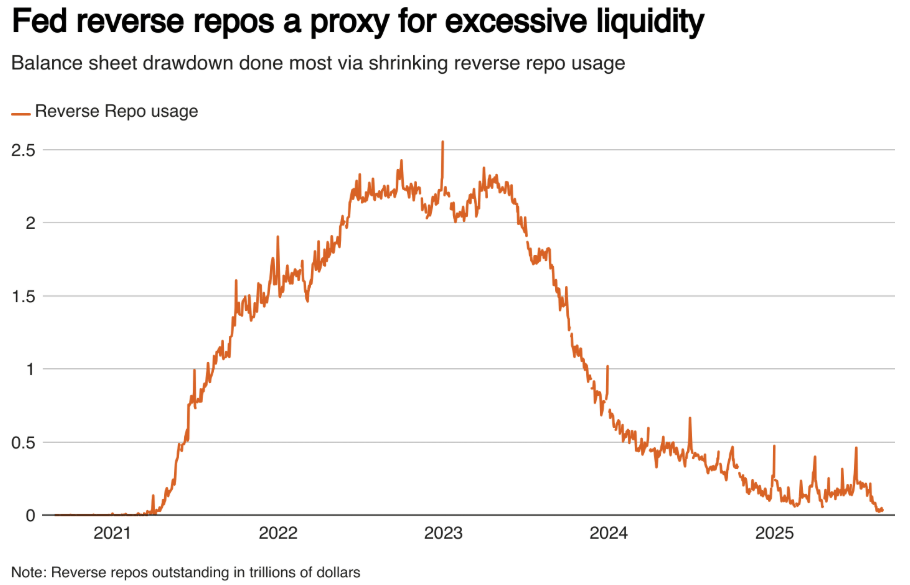

Fed’s ON RRP Facility Balance Near Zero:

The Fed’s overnight reverse repo facility, once absorbing more than $2 trillion a night, has now dropped to zero. That facility served as a pressure valve for excess cash in the system. Without it, every dollar of the Fed’s balance sheet reduction would flow directly from bank reserves, which currently stand at roughly $3.3 trillion.

Reserves are the cash balances that allow the financial system to function smoothly, and their decline matters far more than the headline size of the Fed’s $6.7 trillion balance sheet.Quantitative tightening is reducing the balance sheet by about $40 billion a month. At this pace, reserves could decline to around $2.9 trillion by early 2026. Importantly, this is still well above the approximately $1.4 trillion level at which stress emerged in 2019; however, we need to adjust this number to today’s terms.

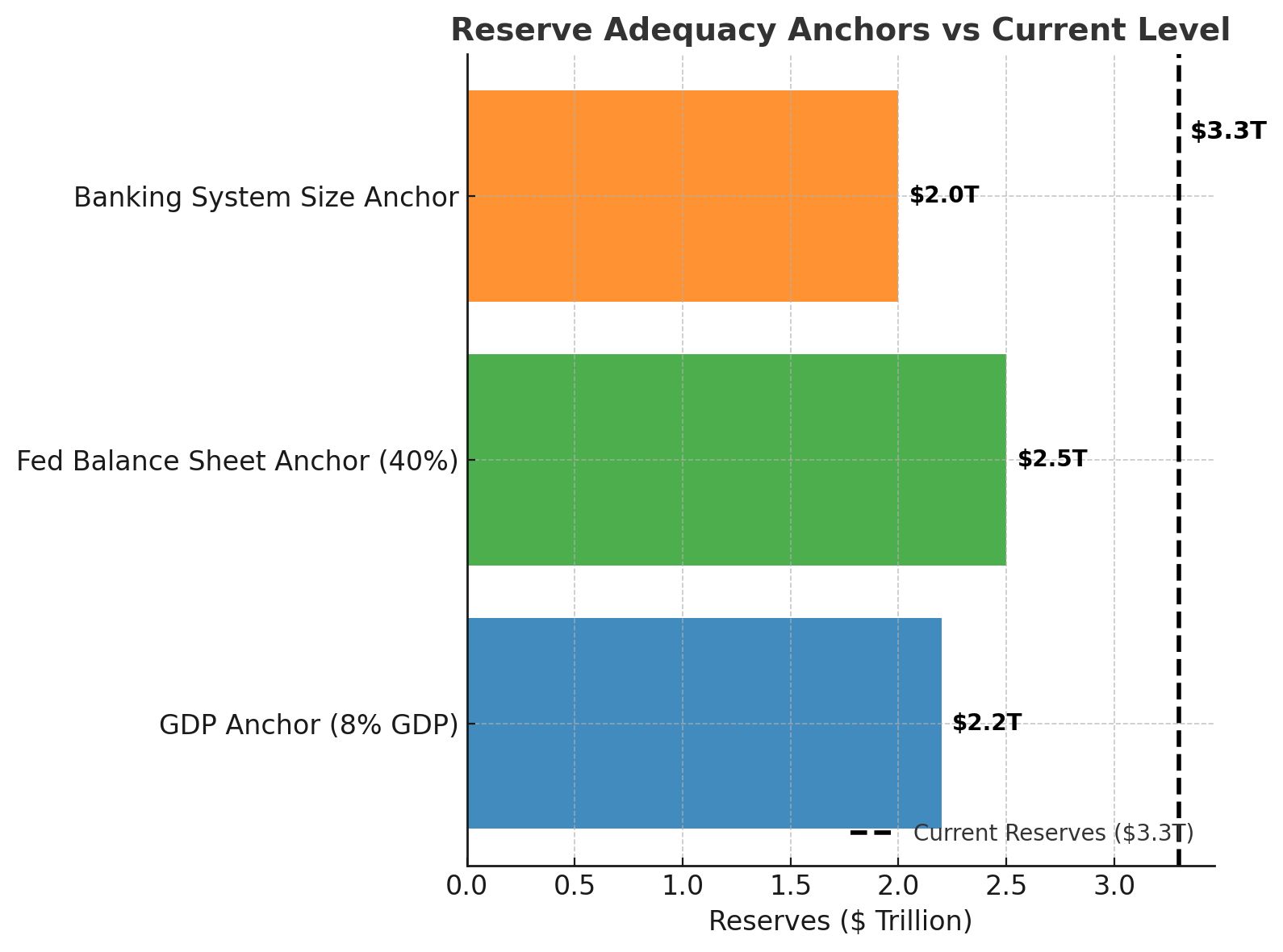

Let’s estimate what the reserve level should be to avoid a 2019-like panic when the overnight repo rate spikes to 8-10%. Below are the three possible estimates -

GDP Anchor: As suggested by Fed Governor Christopher Waller, who noted that reserves below roughly 8% of GDP — about $2.2 trillion in today’s economy — could be problematic. By that measure, the current system still has a cushion of more than $1 trillion. The Fed also has stronger tools today, including the Standing Repo Facility, to smooth temporary strains.

Fed Balance Sheet Comparison: If we compare it to the Fed’s balance sheet in 2019, the $1.4 trillion reserve amount, plus the ON RRP balance, was ~40% of the Fed's balance sheet. With the Fed’s balance sheet ≈ $6.7T, the 2019-equivalent reserve floor (ON RRP is ~0 today) is: 0.40 × $6.7T ≈ $2.7 T. If the Fed’s balance sheet edges down to ~$6.2T (a common 2026 waypoint), the 40% floor becomes ~$2.5T.

Banking System Size Anchor: Reserves fell to approximately $1.4 trillion, against a banking system with roughly $17 trillion in assets. With assets now closer to $25 trillion, the equivalent reserve floor would be nearer to $2 trillion. Beyond scaling for the size of the banking system, it is prudent to allow a wider buffer today. Treasury issuance is larger, and the Treasury General Account is more volatile, resulting in greater swings in reserves.

Primal Thesis

Conclusion: Based on these estimates, it appears that reserves remain ample for now; however, repo spreads, SOFR relative to IORB, and usage of the Standing Repo Facility will indicate whether conditions are shifting from ample to scarce. I think it will be close to accurate to say that banking reserves falling below the ~$2.5 trillion will be problematic. Currently, reserves are at $3.3 trillion, providing a cushion of approximately $800 billion, which can allow the Fed to continue tightening for some time into 2026.

Nvidia Results:

Below are the essential points from the Nvidia conference call. I am not including actual results, which I covered in the earnings update.AI infrastructure spending is projected to reach $3–4 trillion by the end of the decade.

Cloud and enterprise CapEx on data centers and compute set to reach $600 billion this year, nearly doubling in 2 years.

The top 4 hyperscalers alone have doubled their CapEx to $600 billion annually; broader enterprise and global CSP buildouts add further upside.

The U.S. accounts for ~60% of global computing; in the long term, AI adoption is expected to scale with GDP.

NVIDIA software advances and the developer ecosystem have doubled Blackwell performance since launch.

China's AI market is estimated to be worth $50 billion this year, with a potential annual growth rate of ~50%.

China hosts ~50% of global AI researchers and leads in open-source models, making market access strategically important.

Q3 outlook excludes H20 amid geopolitical issues; potential $2–5 billion revenue if resolved.

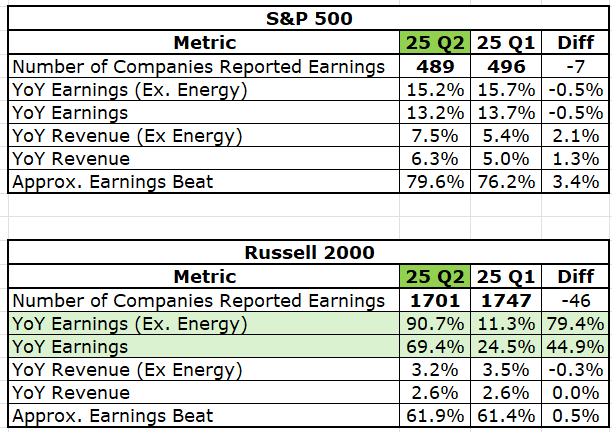

Small Cap Outperformance:

As I do every quarter, check below the quarter-over-quarter comparison of the earnings. This comparison illustrates how this quarter's earnings compare to those of the previous quarter, when a similar number of companies reported in both the S&P 500 and the Russell 2000 index during the earnings season. The most notable development this quarter is the sharp growth reported by small caps compared to the previous quarter. In fact, this is the first time I have noted such growth by small caps since I am writing this newsletter. This explains why the Russell 2000 surged 7.5% in August—more than twice the Dow’s gain and nearly triple the S&P 500’s.

Primal Thesis

FRONT PAGES:

Alt-Coin ETFs: Grayscale filed S-1s with the SEC for spot Polkadot and Cardano ETFs. The Grayscale Cardano Trust ETF (GADA) and Grayscale Polkadot Trust ETF add to 92 pending crypto ETF applications under review. Read

US GDP Continues to Grow: The US economy grew at a 3.3% annualized pace in Q2, up from the initial 3% estimate, driven by stronger business investment and trade. Business investment rose 5.7%, revised sharply higher from 1.9%, led by transportation equipment and the most substantial gain in intellectual property products in four years. Read

Bloomberg

Musk vs. Sam Battle Continues: Elon Musk’s AI startup xAI has sued former engineer Xuechen Li for allegedly stealing Grok chatbot trade secrets and taking them to OpenAI. The complaint filed in California federal court claims Li misappropriated confidential “cutting-edge AI technologies with features superior to ChatGPT” before joining OpenAI this month. Read

Alibaba Enters AI Race: Chinese chipmakers and AI developers are ramping up their homegrown tech as Beijing pushes to win the AI race against the U.S. Alibaba, once a major customer of Nvidia, has unveiled a more versatile chip. Read

Nvidia’s Concentration: Two customers accounted for 39% of Nvidia’s July-quarter revenue, the company disclosed in its SEC filing. Customer A contributed 23% and Customer B 16%. Nvidia said demand for its AI systems remains strong across cloud providers, enterprises, “neoclouds,” and foreign governments. Read

EARNINGS UPDATE:

PDD Beat: PDD Holdings reported Q2 revenue of $14.5B, up 8.7% and $160M above consensus, driven by online marketing and transaction services. Costs rose sharply: revenue costs jumped 36% on higher fulfillment, server, and processing fees, while operating expenses increased 5% from sales and marketing. Non-GAAP operating profit fell 21%. EPADS of $3.08 beat estimates by $1.02 and exceeded last year’s $2.90.

MangoDB Beat: MongoDB posted Q2 results with EPS of $1.08 vs. $0.65 estimate and revenue of $591.4M, up 24% YoY vs. $554.5M estimate. Q3 guidance: EPS $0.76–$0.79 vs. $0.73 estimate; revenue $587M–$592M vs. $583.7M estimate. Full-year outlook raised: EPS $3.64–$3.73 (prior $2.94–$3.12; est. $3.20) and revenue $2.34B–$2.36B (prior $2.25B–$2.29B; est. $2.29B).

CrowdStrike Beat: CrowdStrike posted Q2 results with EPS of $0.93 vs $0.83 expected and revenue of $1.17B vs $1.15B. ARR rose 20% to $4.66B. It acquired Onum to strengthen Falcon Next-Gen SIEM. For Q3, EPS is guided at $0.93–$0.95 vs $0.91 expected, with revenue of $1.21–$1.22B vs $1.23B expected. Full-year EPS is now $3.60–$3.72 (midpoint $3.66 vs $3.51 prior), while revenue is $4.75–$4.81B (midpoint $4.78B, unchanged).

Nvidia Beat: Nvidia posted Q2 revenue of $46.7bn, up 56% year-on-year and above estimates. It guided $54bn for the current quarter, ±2%, versus $53.8bn expected. Growth momentum faces risk as the company flagged uncertainty around China sales amid U.S.-China tensions, with no guidance provided on AI chip revenue from the region.

Dell Beat: Dell reported Q2 results ahead of expectations, with adjusted EPS of $2.32 on $29.78B revenue, up 13% YoY. Client Solutions Group posted $12.5B, up 1%, while Infrastructure Solutions Group rose 44% to $16.8B, driven by a 69% jump in servers and networking to $12.9B. Analysts had expected $2.11 EPS on $25.33B revenue.

Alibaba Miss: Alibaba’s Q2 revenue rose 2% to RMB247,652 million ($34.6B), missing expectations. Adjusted for disposals, revenue grew 10%. Customer management gained 10%, while Cloud Intelligence surged 26%, with AI products posting triple-digit growth for the eighth straight quarter. Local e-commerce lagged amid fierce competition and deflation. Operating income fell 3%, and non-GAAP net income dropped 18% on investments in rapid commerce and AI.

EARNINGS PREVIEW:

Date | Symbol | Name | Time |

29-Aug | BABA | Alibaba Group Holding ADR | Before Open |

2-Sep | ZS | Zscaler Inc | After Close |

3-Sep | CRDO | Credo Technology Group Holding | After Close |

3-Sep | CRM | Salesforce Inc | After Close |

3-Sep | DLTR | Dollar Tree Inc | Before Open |

3-Sep | FIG | Figma Inc Cl A | After Close |

3-Sep | HPE | Hewlett-Packard Enterprise Comp | After Close |

4-Sep | AVGO | Broadcom Ltd | After Close |

4-Sep | CPRT | Copart Inc | After Close |

4-Sep | IOT | Samsara Inc Cl A | After Close |

4-Sep | LULU | Lululemon Athletica | After Close |

8-Sep | ORCL | Oracle Corp | -- |

9-Sep | SNPS | Synopsys Inc | After Close |

VIDEO’s OF THE WEEK:

Please Share This Newsletter With Your Friends.

Also, check my blog here.

This newsletter's content is for informational and educational purposes only and should not be considered trading or investment recommendations. All the opinions in this newsletter are personal and do not belong to any organization.