In partnership with

Weekly Newsletter

📊 Key Takeaways From Earnings

🚀 Cerebras Pops 68% In $5.5B IPO Debut

🛰️ SpaceX Pulls IPO Forward To June 12

⚡ Ford Launched Ford Energy

💰 Banking Reserves Consistent Over $3 Trillion

QUOTE OF THE WEEK:

“You don't need the cooling in space. Number one, as long as you have giant radiators and then electricity, which is a huge cost, you don't need that either, because you're using the sun. So basically, you're getting free electricity and cooling once you're in space.” - Ron Baron, Baron Capital founder, CEO

KEY US ECONOMIC EVENTS NEXT WEEK:

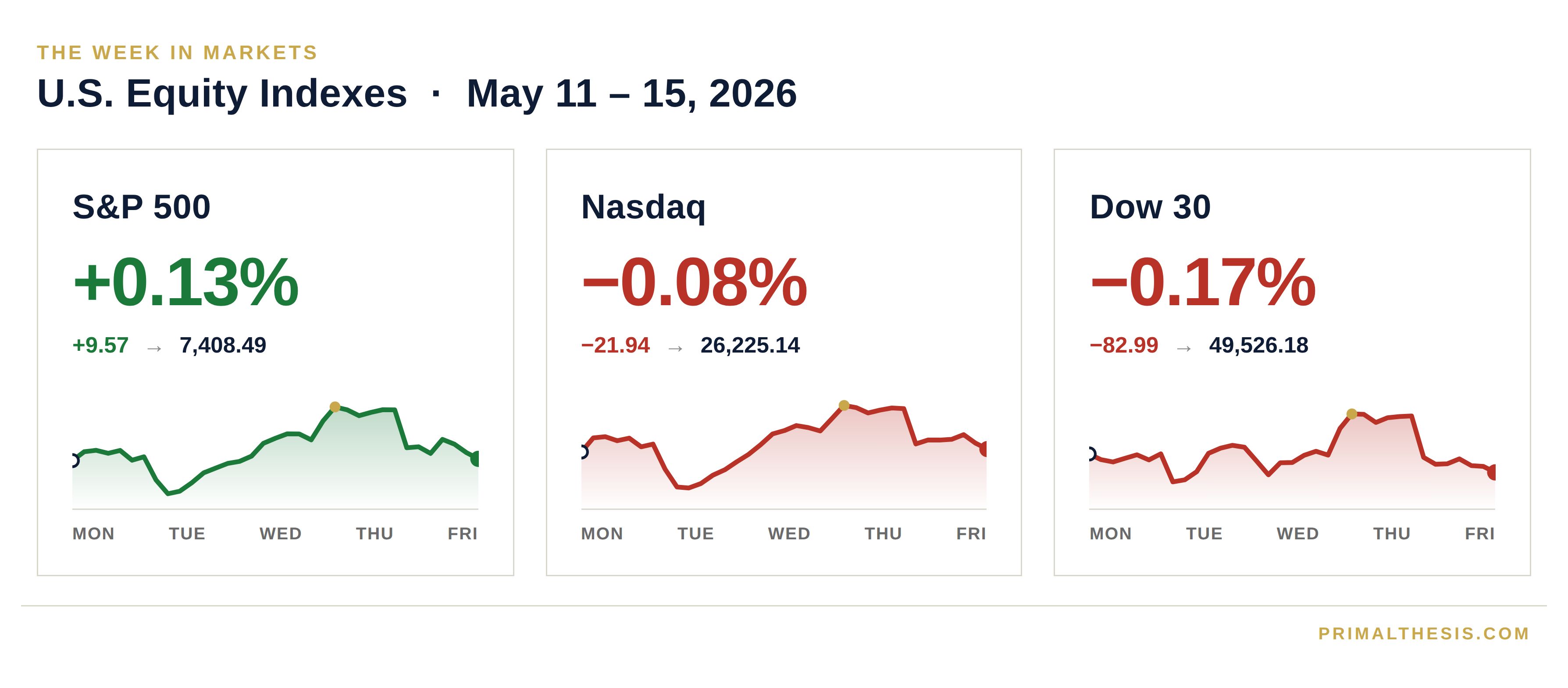

MARKET CLOSE:

WEEKLY MARKET WRAP:

Good Afternoon. Markets ended flat for the week. No surprise from the macro data released, and strong earnings continued into this week. Next week, NVIDIA is scheduled to report. NVIDIA stock recently resumed its uptrend after a prolonged sideways move, and I expect earnings to beat expectations as usual, which could drive its stock and the broader market higher.

Banking reserves have consistently been over $3 trillion and rising over the last couple of weeks, indicating banks have ample liquidity, which is positive for the markets.For the week:

CNN's Fear & Greed Index now stands at 73 (Greed) out of 100, up 6 points from last week. Details here

The top five trending stocks on Reddit are Micron, SPY, Microsoft, NVIDIA, and POET Tech. Read More

Liquidity:

Banking Reserves + ON RRP: Banking reserves remain at approximately $3.11 trillion. ON RRP balance remains immaterial.

Standing Repo Operations: The New York Fed’s standing repo operation (primarily reflecting SRF take-up) is zero.

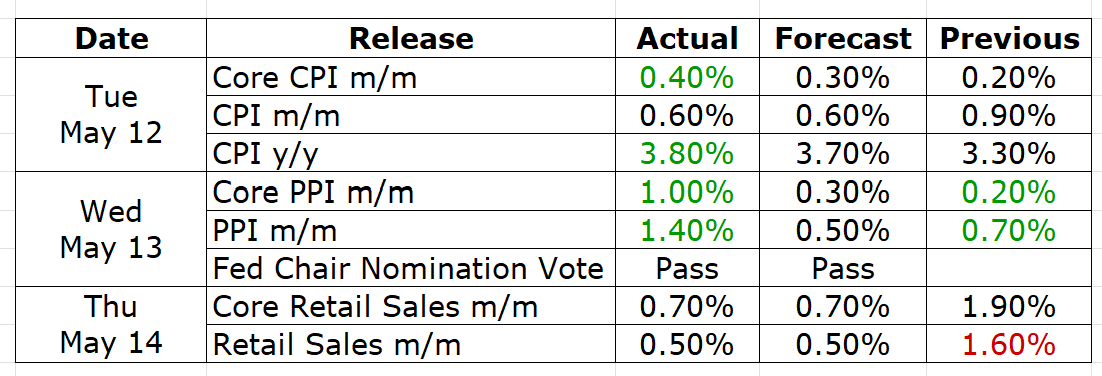

Here is a summary of this week’s key economic releases:

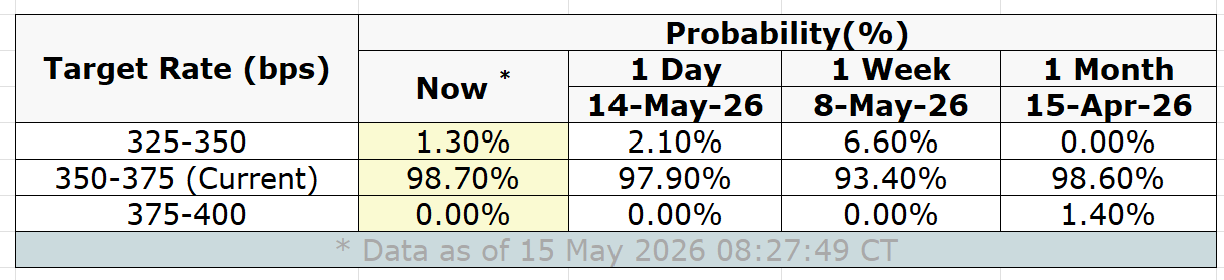

Target Rate Probabilities for June 17th FOMC Meeting:

CURATED INSIGHTS & ANALYSIS:

Takeaways from this week’s earnings:

The 2026 capex curve was lowballed in February. Last week, the framing was that AI capex is structural rather than cyclical. This week, the question shifted: were the 2026 numbers companies were guided to in February already too low? Nebius raised its 2026 capex range to $20–$25B from $16–$20B — a midpoint lift of $4.5B mid-cycle, not at the start. Applied Materials raised semiconductor equipment growth from ">20%" to ">30%" — a 50% increase in the growth rate itself, not the base. Cisco took FY26 AI infrastructure orders to $9B from a prior "$5B+" guide, with $5.3B already booked in nine months. Constellation's Dominguez cited hyperscaler 2026 spending running 75% above 2025. In short, the buildout is not just structural; it is steepening. The companies’ booking orders are not pacing themselves to extend the cycle — they are scrambling to add capacity because the pipeline keeps growing. The $4.5B Nebius mid-year capex increase is the clearest signal of the week.China's internet is being run with US-hyperscaler-style capex discipline — except margins are breaking instead of compressing. Alibaba's non-GAAP net profit fell 99.7% YoY to RMB 86M, while revenue increased 3%. JD's non-GAAP net profit dropped 42% on 4.9% revenue growth. Tencent looks better — operating profit +17% — but missed on the top line and explicitly contrasted its "controllable" AI spend against peers. The unifying feature is that all three are spending on AI infrastructure simultaneously, and BABA and JD are also subsidizing quick commerce and food delivery. I believe the right framing here is that the Chinese internet platform leaders are running the same playbook Mag 7 ran in 2023–2024 — investing through a margin trough — but the recovery curve is harder to underwrite because the cloud monetization isn't there yet at the same scale, and quick commerce subsidies have no analog at META or GOOGL. The revenue is fine. The path back to the margin is the question.

Figma's first earnings print broke the "AI eats Figma" thesis — at least this quarter. Coming into the print, Anthropic's Claude Design launched in April, Google's Stitch had been free since February, and the stock had dropped 88% from its post-IPO high. The bear case was that AI-native competitors would compress seat-based pricing and that Figma's hedge — Make, Draw, Sites, Buzz, Weave — was a defensive move that wouldn't show up in numbers. Revenue accelerated for the second consecutive quarter (38% → 40% → 46%), NDR climbed 300bps to 139%, AI-driven Pro plan conversions rose 150%, and over 75% of over-limit enterprise users kept buying credits after enforcement kicked in. Full-year guidance raised by $55M. Gross margin dipped to 82% due to AI inference costs, a figure management explicitly refused to defend as a floor. In short, Figma's seat-plus-consumption model is currently absorbing AI tooling as a tailwind, not a threat. Time will tell whether that holds through 2027, but the data this quarter pointed in the opposite direction from the narrative.

Brookfield is the financial plumbing for the same buildout. The connection between BN and CEG/AMAT/NBIS/CSCO isn't obvious until you stack the numbers. $67B raised year-to-date across Brookfield's asset management platform. $614B in fee-bearing capital, up 12%. A $40B Just Group mandate. $4B of annuity inflows into Wealth Solutions. Real estate leasing 2.6M square feet at rents 15% above expiring — and a flat "no software exposure, credit portfolio performing incredibly well" callout from CFO Goodman on the recent private credit and software stress. Brookfield isn't an AI play. But the same wall of capital that is funding 228GW of Eaton-led data-center backlog, Nebius's $25B 2026 capex, and Constellation's 5,000MW PJM submission has to be sourced somewhere — and increasingly that source is insurance-linked permanent capital and infrastructure-strategy fund commitments at scale. The asset-light fee model BN is running maps directly onto the asset-heavy infrastructure, spending the rest of this week's tape. The two are the same trade from different sides of the balance sheet.

FRONT PAGES:

Cerebras Pops 68% in $5.5B IPO Debut: Cerebras priced at $185 Wednesday night (above the $150–160 revised range) and closed Thursday at $311 — a $95B market cap and the largest US tech IPO since Uber in 2019. 2025 revenue was $510M (+76% YoY) with $238M net income, anchored by OpenAI's $20B+ multi-year deal and AWS distribution. Stock fell 10% Friday. Opens the door for SpaceX, OpenAI, and Anthropic listings later this year. Read

Trump-Xi Beijing Summit Underwhelms: The two-day summit produced a vague "strategic stability" framework for the next three years and one concrete deal — a 200-plane Boeing order, the first major China-Boeing purchase since 2017. No breakthrough on Taiwan, rare earths, or Iran mediation. The CEO delegation included Musk, Huang, and Tim Cook; Xi told them, "China's door will only open wider." Trump deferred a decision on a $11B Taiwan arms package after Xi's pushback. Read

SpaceX Pulls IPO Forward to June 12 on Nasdaq: Reuters reported Friday that SpaceX is now targeting a June 11 pricing and June 12 debut on Nasdaq under ticker SPCX, with the S-1 flipping public as early as next Wednesday and roadshow launching June 4 — weeks ahead of the original late-June plan, driven by a faster-than-expected SEC review. Target raised ~$75B at a ~$1.75T valuation, the largest flotation ever. Morgan Stanley, BofA, Citi, JPM, and Goldman are joint leads with 16 banks in smaller roles. Read

Powell Exits, Warsh Takes Over Fed Today: Powell's term as Chair ends Friday with Warsh sworn in; Powell remains on the Board indefinitely pending closure of the renovations probe, keeping Warsh in Miran's seat rather than Powell's chair. 10Y yield spiked 9 bps to 4.55% Friday — highest in a year — as the rate-hike-now camp grew louder. CME FedWatch now prices a 45% chance of a 2026 hike vs 1% a month ago. Empire Manufacturing leaped to 19.6 vs 6.2 expected, complicating the "slowdown will force cuts" thesis. Read

SpaceX Pulls IPO Forward to June 12 , Pivots to AI Data Center Batteries: Ford launched Ford Energy on Monday as a subsidiary supplying battery-storage capacity for hyperscaler data centers, deploying tech licensed from China's CATL — a hard pivot from passenger EVs after the post-IRA demand softening. Joins a broader OEM repositioning toward grid/AI infrastructure; signals US-China industrial coupling is deepening on the energy side, even as the chip side decouples. Read

EARNINGS UPDATE:

Primal Thesis

Constellation Energy's Beat: Revenue $11.12B vs. $8.46B consensus — the gap is Calpine, which closed in early 2025 and added an estimated $2/share of full-year accretion. Adjusted operating EPS $2.74 vs. $2.54, with GAAP EPS swinging to $4.49 from $0.38 a year ago on PJM capacity prices and nuclear PTCs. Nuclear capacity factor 92.3% across the operated fleet. FY26 guidance affirmed at $11.00–$12.00. The data-center signal: CEO Joe Dominguez cited hyperscaler 2026 spending running ~75% higher than 2025, and Constellation submitted ~5,000 MW of new capacity into PJM's interconnection queue. $335M deployed on buybacks since the prior call at ~$285/share.

JD.com's Beat: Revenue RMB 315.7B (US$45.8B), up 4.9% YoY, vs. RMB 311.4B Bloomberg consensus; non-GAAP EPS US$0.74 vs. US$0.57 (RMB 5.12 vs. RMB 8.41 a year ago, -42%). The mix shift is the story: electronics and home appliances -8.4% YoY, but general merchandise +14.9% and marketplace/advertising revenue +18.8%. General merchandise now 46% of product revenue, an all-time high. JD Retail operating income RMB 15.0B (up from RMB 12.8B), retail operating margin 5.6% (up from 4.9%). JD Logistics revenue +29%, non-GAAP operating income +600% YoY on AI/robotics leverage. Food-delivery losses narrowed; management said total food-delivery investment in 2026 will decline from 2025. R&D up 48.6% to RMB 6.9B.

Alibaba's Miss: Revenue $35.28B, up 3% in constant currency (+11% ex-disposals), slightly light vs. the $35.76B Street; non-GAAP EPS $0.09 vs. $1.22 consensus — non-GAAP net profit collapsed 99.7% to RMB 86M from RMB 23B a year ago. The margin print, not the top line, is the story. Adjusted EBITA -84% YoY on simultaneous spend across AI infrastructure (Qwen integration into Taobao/Tmall, Alipay, Amap, Fliggy) and quick-commerce subsidies. Customer Management Revenue +8% on a like-for-like basis. 88VIP members crossed 62M. Cloud Intelligence growth carried the strategic case but did not show up in the margin. Annual dividend of $1.05 per ADS ($2.5B aggregate) announced. Management did not provide forward EBITA guidance and did not characterize when the spend curve normalizes.

Cisco's Beat: Revenue $15.84B, up 12% YoY — a company record — vs. $15.56B Street and the top end of management's own $15.4–15.6B guide. Non-GAAP EPS $1.06 vs. $1.03 consensus; GAAP EPS $0.85, up 37%. Product revenue $12.1B (+17%), led by networking +25%. Hyperscaler AI infrastructure orders were $1.9B in Q3 alone, vs. $600M a year ago — YTD total $5.3B already exceeds the prior full-year target. FY26 AI infrastructure orders guidance raised to ~$9B (4.5x FY25); FY26 AI revenue raised to ~$4B; FY27 hyperscale AI revenue projected at $6B+. Total product orders +35% (ex-hyperscalers +19%). Restructuring announced — up to $1B in charges through FY27, ~4,000 roles cut — to redirect spend toward silicon, optics, security, and AI. Q4 revenue guided $16.7–$16.9B.

Nebius's Beat: Revenue $399M, up 684% YoY, vs. $375M Street; non-GAAP loss $0.23 per share, far narrower than the $0.77 loss expected. The AI cloud business alone grew 841% YoY with adjusted EBITDA margin expanding to 45% (from 24% in Q4). Group adjusted EBITDA flipped to a $130M profit. Annualized run-rate revenue $1.9B, up over 50% sequentially. The headline: 2026 capex raised to $20–$25B from $16–$20B, citing pre-committed 2027 demand, including the $27B 5-year Meta contract; pipeline up 3.5x sequentially. Over $6B in fresh capital raised in the quarter — $4.3B in convertible notes plus $2B in NVIDIA equity. FY26 ARR target reaffirmed at $7–$9B with ~40% group adjusted EBITDA margin. Power contracted exceeds 3.5 GW, on track for 4 GW+ by year-end.

Tencent's Miss: Revenue RMB 196.5B (US$28.95B), up 9% YoY, light vs. the RMB 199B Street; non-IFRS EPS RMB 7.36 (~US$1.06) vs. US$1.07 consensus. The miss is narrow, but the operating story is healthy. Operating profit +17%, gross margin to 57% (up 100bps), non-IFRS net profit +11% to RMB 67.9B. Domestic games RMB 45.4B (+6%, decelerating from +24% a year prior); international games RMB 18.8B (+13%). Marketing services +20% to RMB 38.2B, the standout segment, on AI-driven targeting. FinTech and business services +9% on payment volume and cloud demand; Tencent Cloud international +40%. Free cash flow RMB 56.7B (+20%). Hunyuan 3 preview ranked top in China for reasoning models; WorkBuddy and CodeBuddy are gaining traction. Management framed AI investment as "controllable" — a distinction from BABA's run-rate.

Applied Materials' Beat: Revenue $7.91B, up 11% YoY and 13% sequentially — a quarterly record — vs. $7.68B Street and management's $7.65B guide midpoint. Non-GAAP EPS $2.86 vs. $2.68 consensus, up 20% YoY. Non-GAAP gross margin 50%, up 80bps, and the highest in 25 years. Semiconductor Systems $5.97B (+10%) with DRAM $1.7B (+18%); Applied Global Services $1.67B (+17%). Q3 guided to $8.95B ±$500M with EPS $3.36 ±$0.20 — both well above Street. The strategic update: 2026 semiconductor equipment business growth raised to ">30%" from ">20%" three months ago. Advanced packaging is expected to grow over 50% in calendar 2026. Leading-edge foundry/logic, DRAM, and advanced packaging together are expected to drive over 80% of WFE spending growth in 2026 and 2027.

Brookfield's Beat: Distributable earnings $1.6B for the quarter ($0.66/share) vs. $0.65 consensus; DE before realizations $1.39B ($0.59/share, +7% YoY) on 11% growth in fee-related earnings to $772M. Fee-bearing capital reached a record $614B (+12% YoY). $67B raised YTD across the asset management business, including $21B in Q1 and the $40B Just Group mandate in the UK. Wealth Solutions DE $430M for the quarter, $1.7B trailing twelve months (+11%), with $4B of annuity inflows and Wealth Solutions AUM now ~$180B; management expects $25B of new policies in 2026. Real estate signed 2.6M sq. ft. of leases at rents 15% above expiring. $598M returned via dividends and buybacks. CEO Bruce Flatt told investors the firm is "well positioned for a record year of fundraising."

Figma's Beat: Revenue $333M, up 46% YoY, vs. $316M Street and management's $315–$317M guide — second consecutive quarter of growth acceleration (from 40% in Q4 and 38% in Q3). Non-GAAP EPS $0.10 vs. $0.06. Net dollar retention 139%, up 300bps sequentially, and the highest in over two years. Paid customers ~690,000 (+54% YoY); customers above $10K ARR +37%; customers above $100K ARR growing strongly. AI-driven Pro plan conversions +150% YoY. AI credit monetization launched on March 18; over 75% of enterprise users with over-limit balances continued to consume credits in April. Non-GAAP operating margin 16%, FCF margin 27% (depressed 17 percentage points by annual bonus payout). FY26 revenue guidance raised to $1.422–$1.428B (35% growth, +$55M vs. prior); Q2 guided to $348–$350M (40% growth). Gross margin dipped to 82% due to AI inference costs, with management explicitly stating the focus is gross profit dollars, not a margin floor.

EARNINGS PREVIEW:

Date | Symbol | Name | Time |

19-May | HD | Home Depot | Before Open |

20-May | ADI | Analog Devices | Before Open |

20-May | LOW | Lowe's | Before Open |

20-May | NVDA | Nvidia Corp | After Close |

20-May | TJX | TJX Companies | Before Open |

21-May | DE | Deere & Co | Before Open |

21-May | WMT | Walmart Inc | Before Open |

VIDEO’s OF THE WEEK:

Trade Real-World Events. Get $10 Free.

Start trading real-world events. With Kalshi, you can trade on things you already follow: inflation, elections, sports, and more. It’s simple: buy “Yes” or “No” shares on what you think will happen, and earn returns if you’re right.

To get you started, we’re giving you a free $10. Use it to explore the platform, test your instincts, and see how prediction markets work in real time.

Join thousands already trading the news and putting their knowledge to work.

Claim your $10 and start trading now.

Trade responsibly.

Please Share This Newsletter With Your Friends.

Also, check my blog here.

This newsletter's content is for informational and educational purposes only and should not be considered trading or investment recommendations. All the opinions in this newsletter are personal and do not belong to any organization.