In partnership with

Weekly Newsletter

Strong Bank Earnings

In line CPI Inflation

Dollar Smile

TikTok Goes Dark In US

Potential New Tariff Levels and Impact On Inflation

Interesting Insights On Discount Window Stigma From The Fed

QUOTE OF THE WEEK:

“The economy in the U.S. is quite constructive still. But it's a complicated world. And I think we all should be on our toes and be prepared for the unexpected because I tell you every single year the consensus that people tell me in January, the year turns out to be different than the consensus. And I'm sure this year, there'll be some surprises to the ups, and there'll be some surprises to the downs as there always are.” David Soloman, CEO - Golman Sachs

KEY US ECONOMIC EVENTS NEXT WEEK:

MARKET CLOSE:

CNBC: EOD Jan 18th

Good Afternoon. It was a good week for markets, with all major indices ending positive following the stellar results from the largest US banks and in line with CPI inflation numbers. Below are the highlights of the week:

The six largest US banks posted $142 billion in profits last year, driven by high interest rates, a robust economy, and a revival in dealmaking and Wall Street activity. JPMorgan Chase, Bank of America, Citigroup, Wells Fargo, Goldman Sachs, and Morgan Stanley recorded a 20% increase in collective net profits from 2023, marking their second-best year since 2007.

Source: Appeconomyinsights.com

The earning season has started well, and it’s super important for the market rally to be revived, considering the valuations are high post-back-to-back 20%+ return years.

Summary of this week’s key economic releases:

The Consumer Price Index for All Urban Consumers (CPI-U) rose by 0.4% in December on a seasonally adjusted basis, following a 0.3% increase in November. Over the past 12 months, the all-items index recorded a 2.9% increase before seasonal adjustment. Core CPI, excluding volatile food and energy prices, increased by 0.2%, marking its smallest rise since July and falling short of economists' 0.3% forecast.

As usual, it is essential to remember that the CPI is not what the Fed uses for its inflation targeting. The PCE, the official measure of inflation for the Fed, will be released on Jan 31st. Looking at the CPI numbers, PCE is expected to continue to come down.

The labor market continues to cool as the unemployment claims are slightly higher than forecast (217k vs 210k).

In short, nothing surprising as such with the economic data.

For the week:

The S&P 500 is up 2.91%, the Nasdaq is up 2.45%, and the Dow 30 is up 3.69%.

Source: Barchart

CNN's Fear & Greed Index now stands at 38 (Fear) out of 100, up 11 points from last week. Details here

The top five trending stocks on Reddit are SPY, Trump Media, Tesla, Nvidia, and Intel. Read More

Target Rate Probabilities for Jan 29th FOMC Meeting:

CME Fed Watch

FRONT PAGES:

TikTok Goes Dark In US: Apple and Google removed TikTok from their app stores Saturday night, following a law mandating ByteDance, its Chinese owner, to divest the app or face a U.S. ban. As a result, TikTok is no longer available for download in the U.S., and the platform has ceased operations. Read

Hindenburg Research Closes Shop: A prominent investment firm known for its successful short-selling strategies is shutting down, founder Nate Anderson announced on Wednesday. Read

The Consumer Financial Protection Bureau Sues Capital One: CFPB has filed a lawsuit against Capital One, accusing the bank of misleading customers and depriving them of over $2 billion in interest. The agency alleges that deceptive marketing practices were used to obscure interest rate differences between two savings account options. Read

The Bank of England Delays Basel Rules: BoE announced a one-year delay in implementing stricter bank capital rules, pushing the timeline to January 2027 to await clarity on U.S. actions under Donald Trump’s presidency. Read

IMF Raises US Growth Forecast: The UN financial agency revised its 2025 U.S. growth forecast upward to 2.7% from 2.2% in its October projections while lowering growth estimates for major European economies, including Germany, France, and Italy, as well as Canada. Read

Bank CEOs Confident: Wall Street CEOs expressed optimism on Wednesday about the incoming U.S. administration's pro-business stance, citing a surge in profits driven by increased dealmaking and trading activity. Read

SEC Sues Musk: The SEC sued Elon Musk on Tuesday, alleging he violated securities laws in 2022 by failing to disclose his active stake in Twitter, enabling him to acquire shares at "artificially low prices." Read

EARNINGS UPDATE:

Goldman Sachs Beat: Goldman Sachs surpassed Wall Street expectations, reporting its highest quarterly profit over three years, driven by increased deal fees from the investment banking division and strong performance in trading. Read

JPMorgan Chase Beat: JPM achieved a record annual profit, driven by a strong fourth-quarter performance from its dealmakers and traders benefiting from rebounding markets. Read

Citi Beat: Citigroup exceeded fourth-quarter profit expectations, driven by strong performance in trading and dealmaking. Read

Wells Fargo Beat: Wells Fargo exceeded profit expectations in the fourth quarter, driven by a recovery in dealmaking activity, and projected higher earnings from interest payments in the coming year. Read

Charles Schwab Beat: Charles Schwab reported a 25% rise in third-quarter net income, fueled by higher asset management fees and record client assets. These results, among the final under CEO Walt Bettinger before his retirement in late 2024, set the stage for incoming chief Rick Wurster. Read

Morgan Stanley Beat: Morgan Stanley surpassed fourth-quarter earnings and revenue estimates, driven by strong equities and fixed-income trading performance. Quarterly profit more than doubled, with a 26% revenue increase as all major business segments showed improvement. Read

Bank Of America Beat: BoA reported fourth-quarter results exceeding expectations, driven by stronger investment banking and interest income. Profit more than doubled, while revenue surged 15% due to higher fees from investment banking and asset management, along with improved trading performance. Read

Blackrock Beat: BlackRock’s assets reached a record $11.6 trillion in the fourth quarter, driven by a 21% profit increase as stronger equity markets boosted fee income for the world’s largest money manager. Read

EARNINGS PREVIEW:

Date | Symbol | Name | Time |

21-Jan | NFLX | Netflix Inc | After Close |

22-Jan | JNJ | Johnson & Johnson | Before Open |

22-Jan | PG | Procter & Gamble Company | Before Open |

23-Jan | ISRG | Intuitive Surg Inc | After Close |

24-Jan | AXP | American Express Company | Before Open |

CURATED INSIGHTS:

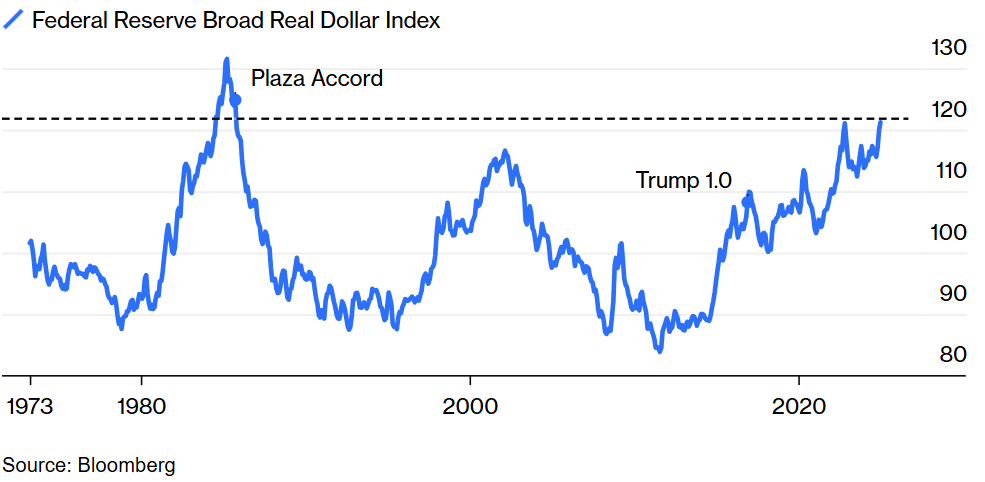

Dollar Smile:

Being a haven currency has its massive advantage for the US Dollar. It strengthens when we have a strong economy, or there is fear or stress in the market when the demand for safe assets increases. The below graphic perfectly depicts the dollar duel advantage.

Source: Daniel Dubrovsky

The US dollar has been on a roll recently and is trading at a 40-year high in real terms. This is in anticipation of the new Incoming administration, which is expected to be pro-economy. This is despite the fact that in recent years, especially since the US sanctions on Russia, many countries are trying to diversify and find alternatives for the dollar to diversify just in case they ever face similar impediments as Russia. That’s one of the major reasons why Gold rallied in the last couple of years, which I discussed in this newsletter in the past.

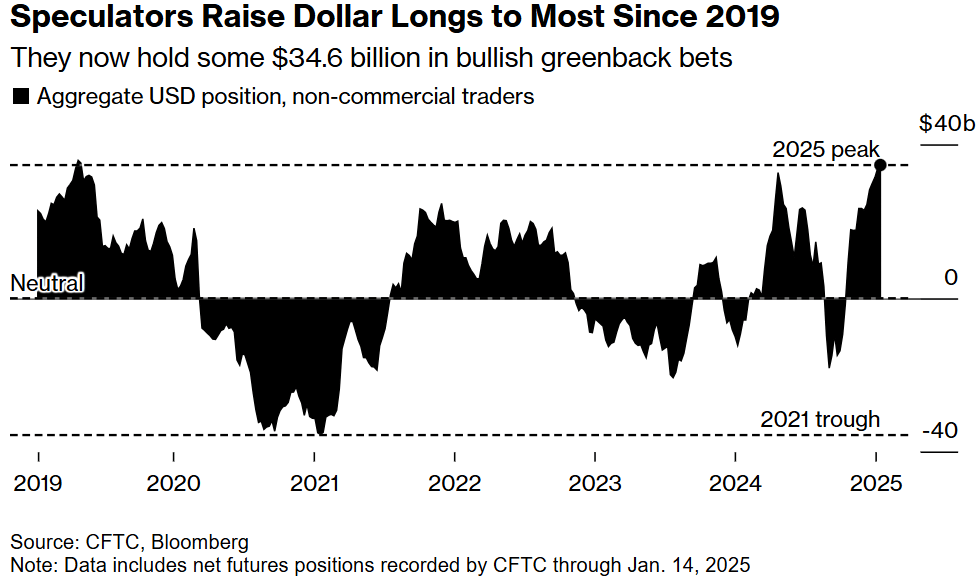

As of January 14, derivative traders had amassed total bets equivalent to $34.6 billion, anticipating further gains in the dollar—a nearly $1 billion increase from the previous week, marking the highest level since 2019, according to Commodity Futures Trading Commission data aggregated by Bloomberg. This indicates that the dollar is expected to continue its rally in the near term.

Analysis Of Trump Tariff Proposal:

An analysis from the Tax Foundation estimates that the new Trump tariff proposal will increase the US tariff rate to 17%, the highest since the great depression.

Intriguing Insights On Discount Window Stigma:

The Fed blog, published this week, analyzes the discount window stigma since the financial crisis. The analysis provides fascinating insights and explains the concept of realized stigma, which is how much more a bank actually pays above the primary credit rate to borrow. The realized stigma is the lower bound estimate as it just shows how much banks paid during the stress, but they may be willing to pay more that time, which can not be gauged as no such data will be available.

The most important observation is that having operational readiness to borrow from the discount window had less significance for the bank to avoid stigma. This is important as SVB’s (Other smaller banks) lack of operational readiness to borrow from the discount window during the 2023 banking stress was considered one of the crucial reasons for its collapse. Check below specific para, which shows how banks with operational readiness were also not willing to borrow from the discount window (for sure due to fear of negative publicity):

I will say that having operational readiness to borrow from the discount window is a must, but it's still not the most critical issue. The most important thing for the banks is to hold high-quality assets in their liquidity buffer/HQLA, which they can monetize easily during stress via multiple private channels if, in the worst case, the bank does not have operational readiness. I believe only US LCR Level 1 securities fit the bill in terms of quality and liquidity.

I talked about this in my detailed analysis of SVB’s collapse. The agencies are taking steps to reduce the stigma, and last year, Reg YY FAQ tried to address this issue, and I covered it in my blog here. I highlighted in this blog that the Fed uses external vendor data for pricing. So, even if a bank is operationally ready to borrow from the discount window, it needs HQLA securities to pledge at a discovered price. Off the run, illiquid securities with no price discovery will get zero value, as per the Fed website.

VIDEO’s OF THE WEEK:

From Wall Street to Your Portfolio: Master Value Investing

The Applied Value Investing Certificate Program from Wharton Online and Wall Street Prep is an 8-week, online, self-paced program that teaches participants how to identify undervalued stocks with the process-driven approach used by the world’s top investors.

Program benefits also include:

Guest Speaker Series with top industry professionals

Exclusive access to networking and recruitment events

Invitation-Only LinkedIn Groups and Slack Channels

Certificate issued by Wharton Online and Wall Street Prep

Please Share This Newsletter With Your Friends.

Also, check my blog here.

This newsletter's content is for informational and educational purposes only and should not be considered trading or investment recommendations. All the opinions in this newsletter are personal and do not belong to any organization.