Weekly Newsletter

📉 Fear Of Tariff War Trigger Market Sell Off

⚠️ Significantly Higher Than Expected Reciprocal Tariffs

🔍 Loose Tariff Formula Ignores Key Factors

🐻 Nasdaq Enters Bear Market

📊 It’s Not All Doom & Gloom: Detailed Analysis Of Tariff Impact

🤝 Most Trading Partners Will Negotiate

QUOTE OF THE WEEK:

I really think the person who created that list, whoever vetted it, and whoever presented it to the U.S. public, has some questions to answer because that was unfair. The president needs better advice, and I think the American people deserve better as well. - Andrew Hale, Senior Policy Analyst for Trade Policy at the Heritage Foundation, on the flawed formula used to calculate tariffs.

KEY US ECONOMIC EVENTS NEXT WEEK:

MARKET CLOSE:

CNBC: EOD April 4th

Good Afternoon. Trade war fears marked the worst week for the stocks since the 2020 Covid crisis. Trump announced sweeping tariffs on April 2nd. Though many countries talked about negotiations, China retaliated within 48 hours, which escalated the sell-off.

Detailed coverage of the tariff situation in the curated insights and analysis section. Below are this week’s highlights:

The US announced an effective tariff rate of ~22.5%, the highest in 100+ years. Below is the sheet shown by President Trump during the announcement:

The S&P 500 dropped 9% this week, marking its sharpest two-day selloff since March 2020 and wiping out nearly $5 trillion in market value.

Source: Factset, WSJ

The Nasdaq 100 officially entered bear market territory, while European equities slid into correction.

Volatility surged, with the VIX spiking to 45 as risk-off sentiment took hold.

Investors rotated into havens — Treasuries and the yen rallied, pushing 10-year U.S. yields below 4%.

CDS spreads on investment-grade debt posted their sharpest jump since the March 2023 banking turmoil.

Oil prices collapsed to a four-year low.

For the week:

The S&P 500 is down 9.08%, the Nasdaq is down 10.02%, and the Dow 30 is down 7.86%.

CNN's Fear & Greed Index now stands at 4 (Extreme Fear) out of 100, down 16 points from last week. Details here

The top five trending stocks on Reddit are SPY, enCore Energy, MAGA, Tesla, and Nvidia. Read More

Here is a summary of this week’s key economic releases:

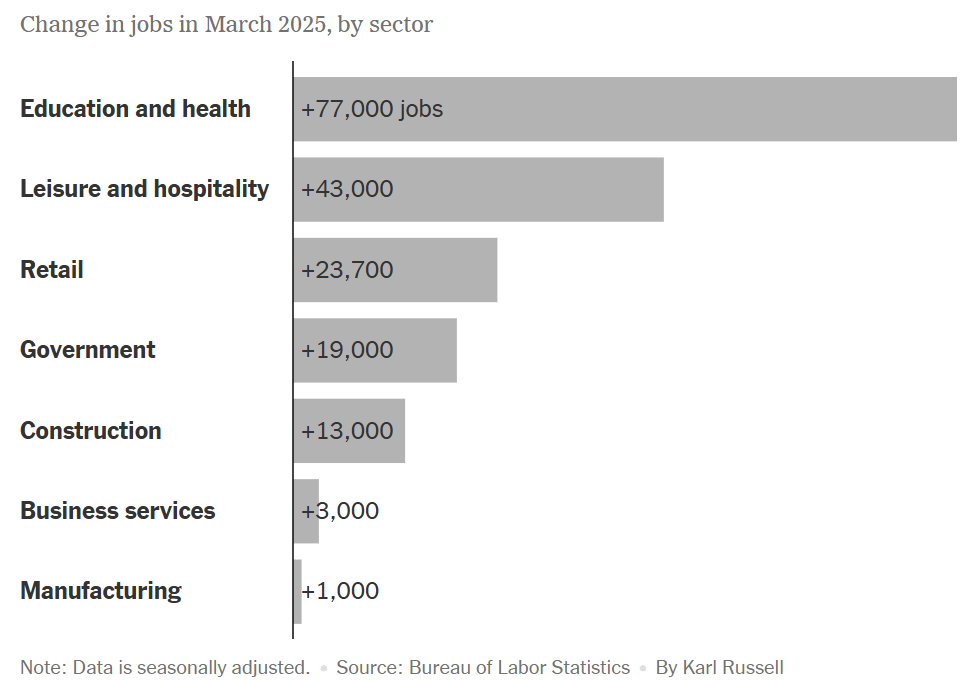

Overall, macro data this week was still decent. Non-farm payrolls came in much better than expected. Payroll employment rose by 228,000 in March, rebounding from weak January and February gains. The private sector drove the increase with 209,000 jobs, while the government added 19,000. Federal employment fell by 4,000, following an 11,000 drop in February.

Source: NY Times

Target Rate Probabilities for May 7th FOMC Meeting:

CME FedWatch

CURATED INSIGHTS & ANALYSIS:

My Analysis of Tariff Situation:

There is a lot of uncertainty due to tariffs, and markets are trying to price in the impact. Below is my analysis of the tariffs announced this week and how they will play out in the coming months. All is not doomed, and I think there is still a strong probability that this saga will have a positive outcome for the US:

Are The Announced Tariffs Good?: Economists generally agree that the answer is no, especially given how the US calculated the reciprocal tariff rates announced on April 2nd. More on this later. Also, tariffs are not announced only against serious offenders but against countries with which the US has a trade surplus, e.g., the UK.

The Surprise: Institutions were expecting 10-15% effective tariff rates coming into this week. However, to everyone’s surprise, the tariff announced on April 2nd puts the effective tariff rate at ~22.5%, which is the highest tariff rate charged by the US in 100+ years.

Source: Financial Times

Loose Formula: Why did everyone get their estimates wrong? The main culprit is this administration's loose formula for calculating reciprocal tariffs. Two main criticisms of the formula:

The formula assumes that a bilateral trade deficit solely indicates unfair trade practices by the other country. However, trade deficits can result from various factors, including differences in savings rates, investment flows, and currency valuations, not necessarily unfair practices.

It does not consider the trade-weighted tariffs imposed by other countries, which are much lower than the White House calculation shows. Critics argue that the effective tax rate will not exceed 14% if trade weighting were considered as per the WTO data. Read

Considering all this, below are a few of the positives that I believe will prevent the trade war or the dire economic consequences:Silver Lining—The Exemptions: The Silver lining is that the US's main trading partners, Mexico and Canada, are exempted from additional reciprocal tariffs. The Trump administration issued carve-outs covering $644bn in imports— $185bn from Canada and Mexico and $459bn globally. This accounts for roughly 20% of the total U.S. imports.

Most Countries Will Negotiate:

The US is the largest market in the world, and the world needs it to sell its products. According to recent news from the White House, more than 50 countries have contacted the US to initiate trade negotiations this week after the Liberation Day announcement. Except for China, no other major trading partner has announced retaliatory tariffs. India, the UK, Taiwan, Vietnam, and many other countries have openly expressed interest in working with the US on trade deals. Below are the key reasons why it will be wiser for most countries to negotiate rather than retaliate:No One Can Replace US Consumer: The World depends on US consumers to sell its products. I remember when I was doing my MBA in 2007-08, my macroeconomics professor gave us a project to analyze China’s currency manipulation. He was clearly of the opinion that China manipulates its currency, and it’s not good for the US. Most of the students came to the same conclusion, agreeing with the stand that China is a currency manipulator. I remember my analysis was slightly different. I agreed that China manipulates its currency, but it does so to promote its exports and, most importantly, the US is allowing China to do this as it benefits from the Cheaper goods. So it’s not all China’s fault. One way the US can stop China is by imposing tariffs. One student asked during my presentation if the US may not impose tariffs on China, as it will stop exporting to the US and hurt the US. I remember replying that it’s not possible for China to replace the US market. Back then (2007-08), US consumer spending was over $9T and China’s was under a trillion. So who will China sell to if not US consumers? (as China, despite being the second largest economy, was nowhere close in consumer spending). The reason for this long story is that, fast forward today, China has made significant progress, but its consumer spending is still at $6.5T, and US consumers spent over $20T last year. There is no bigger market than the US. US consumer spending is ~70% of US GDP; that ratio for China is ~36%.

The world will come to the table to negotiate, as all have negative consequences. Economists largely agree that the 10-14% flat tariffs make sense. The White House may not publicly accept the issues with its formula, but it can be more conciliatory in private negotiations.

Tariff Revenue vs. GDP Loss: The expected GDP loss per most institutional forecasts is around 1-1.5%, which is a loss of $280bn to $400bn.

Source: Apollo

However, suppose all the reciprocal tariffs stay as they are (which is highly unlikely). In that case, the most conservative estimate of tariff collections for the U.S. government is $290 billion, according to the Tax Foundation. For simplicity, let’s round it to ~$300 billion.

📉 Note: This estimate already accounts for reduced import volumes due to higher tariffs. Optimistic forecasts place the potential revenue above $600 billion.Now let’s compare this with the GDP impact:

Assumed GDP loss due to tariffs = $400 billion

Average corporate profit margin (S&P 500) ≈ 12%

→ Corporate profit lost = 12% of $400 billion = $48 billion (~$50 billion for simplicity)

Effective corporate tax rate = 21%

→ Tax revenue lost = 21% of $50 billion = $10.5 billion (~$10 billion)

Summary:

Tariff revenue (conservative): ~$300 billion

Tax revenue lost from GDP impact: ~$10 billion

➡️ Net revenue gain for the U.S. government = $300B – $10B = ~$290B

Even under conservative assumptions, tariff-related revenues far exceed the government’s tax revenue loss from reduced GDP. Therefore, the fiscal impact of tariffs is strongly positive from a pure fiscal perspective for the Government. Economic momentum could persist if much of the revenue supports growth-friendly areas like tax cuts. But if it's mainly used to narrow the fiscal deficit, the U.S. economy may slow more noticeably. So, even though the GDP loss is terrible, the overall impact can be dampened with other effective policies and efficient use of additional tariff revenue.Inflation Impact & Mid-Term Elections: Due to reciprocal tariffs, PCE inflation is expected to increase by 1 to 1.5%. This and the GDP loss will hurt the middle and lower income groups. There are mid-term elections in 2026, and the Republican Party won’t like to lose control and can’t afford to ignore its voters. Hence, I am sure there will be a lot of pressure on the President in the coming months to correct the course as necessary.

Possible Fed Response: There is no Fed put as such now, as inflation expectations are higher. However, I discussed a couple of times in this newsletter that average inflation targeting may allow the Fed to cut rates even if inflation is slightly higher than target if the economy slows down significantly.

Conclusion:

Markets hate uncertainty, and hence, the recent sell-off is understandable. However, it’s too soon to conclude that the trade war will undoubtedly escalate due to the abovementioned reasons. I think markets are overreacting as expected and may continue to go down for some time. However, recovery will be faster once more clarity comes in the coming months. I hope good sense prevails.

FRONT PAGES:

Countries Ready for Tariff Negotiations: Over 50 countries have approached the White House to initiate trade talks, according to a top economic adviser to President Trump, as U.S. officials defended broad new tariffs, sparking global disruption. Read

Meta’s Debut New AI Model: Meta unveiled initial models from its open-source Llama 4 AI software, aiming to gain ground in the generative AI race. The most advanced version, which surpasses peers and acts as a “teacher,” remains unreleased. Two models live via Meta AI on WhatsApp, Messenger, Instagram Direct, or the Meta AI site. Read

Powell’s Reaction: Fed Chair Jerome Powell said Trump’s tariffs are likely to push inflation higher and dampen growth. The Fed will hold off on rate changes until the full effects are clearer. Read

One More Good News On Crypto: The SEC clarified Friday that it does not consider certain stablecoins to be securities. The move follows growing optimism that Congress will pass its first crypto bill this year, focused on stablecoins. Trump has urged lawmakers to send the legislation to his desk before the August recess. Read

Discover-Cap One Merger: The New York Times reported that Capital One moved closer to acquiring Discover after the DOJ told regulators it found no significant competition concerns to justify blocking the deal. Read

Visa Bid For Apple Card: Visa has reportedly offered Apple $100 million to move Apple Card to its network, highlighting intensifying competition among payment giants. Amex is also pursuing the card as both issuer and network, following Goldman’s 2023 outreach. Apple Card is currently on Mastercard’s network. Read

Preferential Treatment To Neighbours: Mexico’s economic minister Marcelo Ebrard welcomed the “preferential treatment” after President Trump announced new global tariffs. While the 10% baseline applies broadly, Mexico and Canada were spared from the latest reciprocal measures, though prior tariffs remain. Read

China Retaliates: China said it will impose a 34% tax on all U.S. imports next week, escalating its response to President Trump’s latest tariffs. Read

EARNINGS UPDATE:

Conagra Miss: Conagra missed Q3 sales and profit estimates, hit by weakening snack demand and supply chain issues in its frozen and refrigerated segments. The company is grappling with slowing growth as consumers shift to cheaper private labels, alongside production setbacks at a key facility. Read

EARNINGS PREVIEW:

Date | Symbol | Name | Time |

11-Apr | BLK | Blackrock Inc | Before Open |

11-Apr | JPM | JP Morgan Chase & Company | Before Open |

11-Apr | PGR | Progressive Corp | -- |

11-Apr | WFC | Wells Fargo & Company | Before Open |

VIDEOs OF THE WEEK:

Please Share This Newsletter With Your Friends.

Also, check my blog here.

This newsletter's content is for informational and educational purposes only and should not be considered trading or investment recommendations. All the opinions in this newsletter are personal and do not belong to any organization.