Weekly Newsletter

📉 Bear Market vs. Correction

🔑 Key Catalysts for Markets in the Near Future

💰 Gold Surpass $3000

📜 Historical Analysis of Market Corrections

🎭 Unreliable Institutional Predictions

QUOTE OF THE WEEK:

No, we're not surprised by any of this. And in fact, I think investors are getting way too wrapped up in the daily headlines. It's like a daily herky-jerky motion thing, and they should just kind of let things ride out. There's a lot of information that still needs to come into play for a long-term investor. So we haven't been doing a lot, honestly, because our base case is still that there was going to be some hiccups in this transition from the new administration and the new economic policies, and that seems to be playing out. And what you do is you try to find opportunities when you have crazy days and take advantage of them. - Michael Cuggino, President and Portfolio Manager of the Permanent Portfolio Family of Funds

KEY US ECONOMIC EVENTS NEXT WEEK:

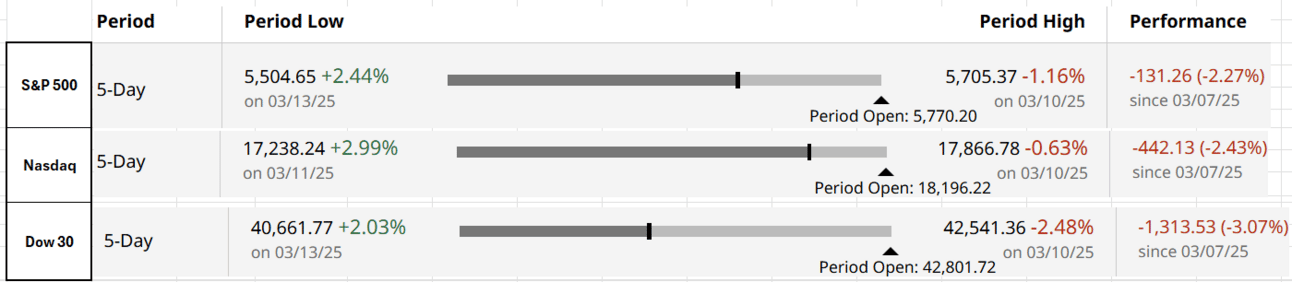

MARKET CLOSE:

CNBC - EOD March 14th

Good Afternoon. It was another bad week for the markets, with all major indices recording decent losses, with DOW being the most impacted, with a drop of 3.07%. Next week is extremely busy, with significant events lined up.

One of my friends texted me this week, saying, “Markets are gone.” I replied, “It’s ok — they will come up. It’s normal”. Volatility is part and parcel of investing. Check the curated insights section for the couple of visuals that are shown. I have followed markets for over two decades and am used to the volatility. However, many investors don't like this about stocks and are nervous about what’s next. However, below are the essential things to note and why I am not worried about fundamentals:Below are the key things to note:

Correction vs. Bear Market:

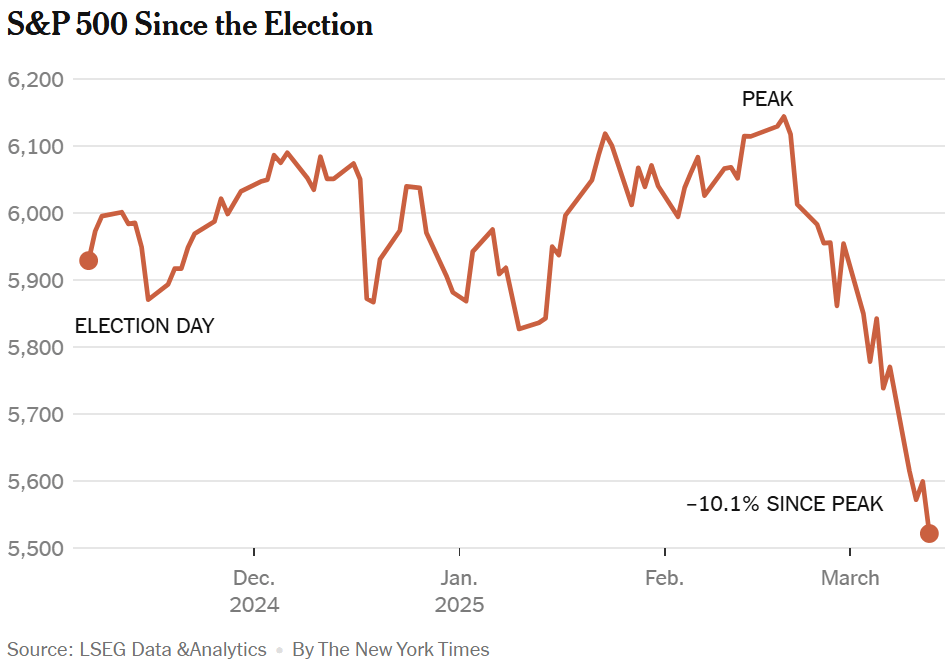

When markets are down >10%, it’s a correction, and if they are down >20%, then it’s called a bear market. By this definition, the S&P 500 entered a correction territory this week. Markets on average, pull back by 10% once a year, so this is not unusual, especially after great couple of years -

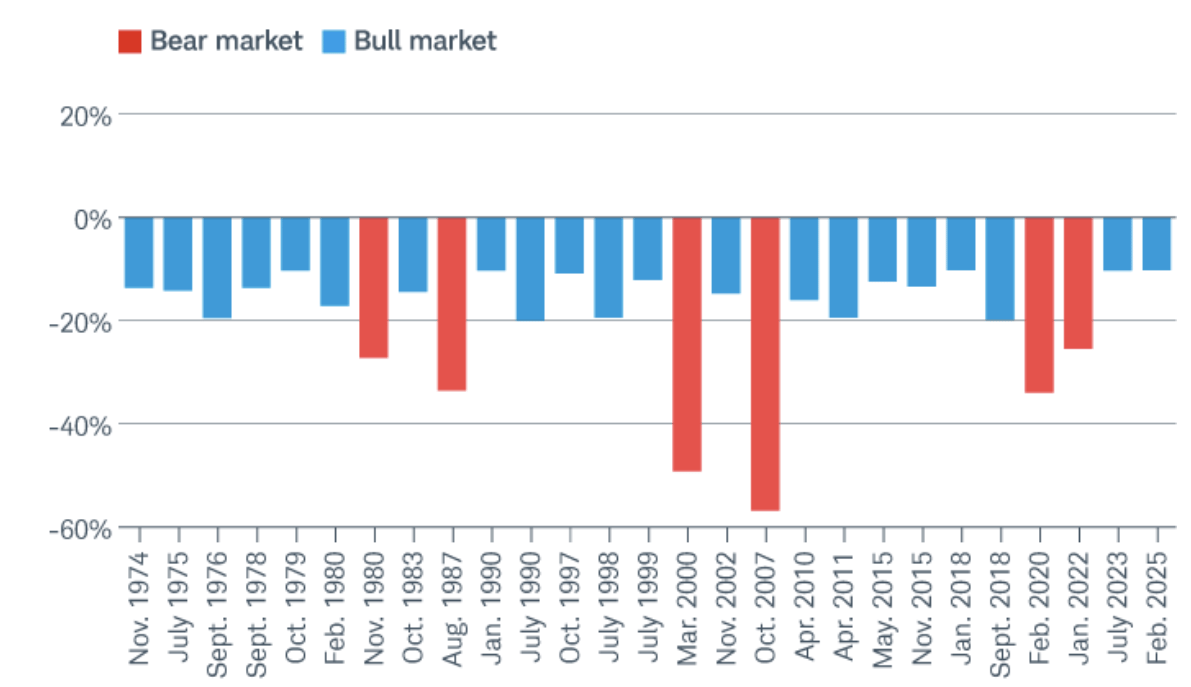

However, a graph from Charles Schwab shows 27 market corrections since November 1974—including the current one—and only six turned into bear markets.

Source - Charles Shwab

No Major Reason For Bear Market:

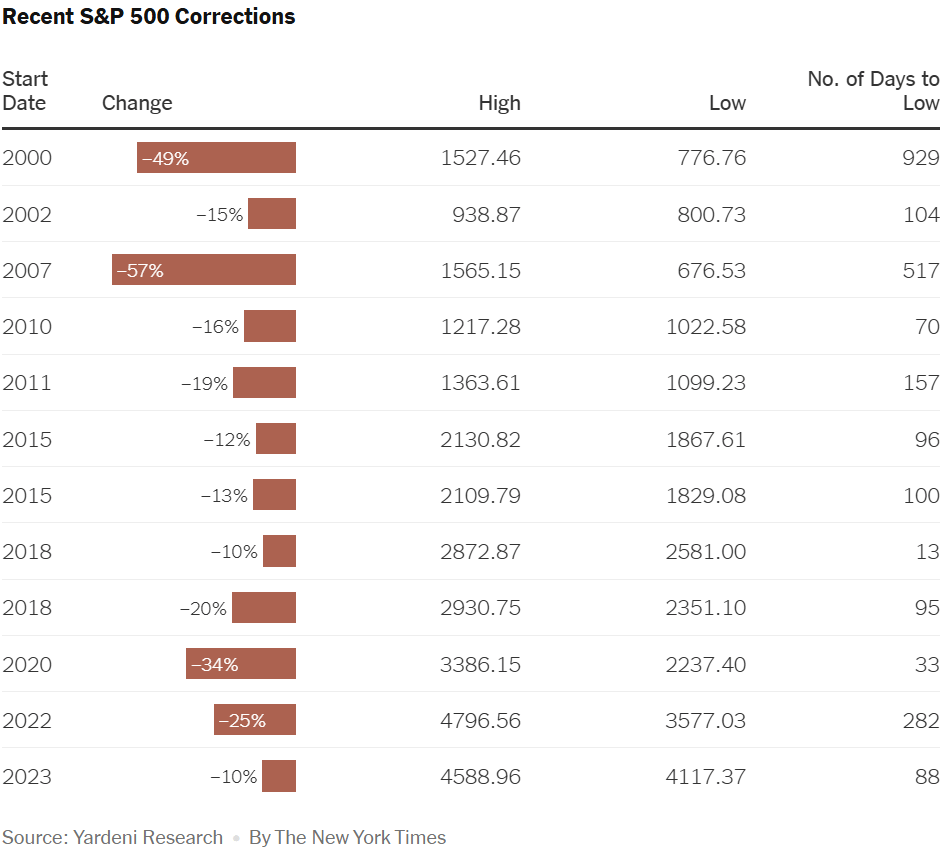

Going further, the data below from Yardeni Research shows that out of 12 corrections in this century, only four turned into bear markets, i.e., >20% drop.

Now, if you notice, in all these four cases, there was a significant issue with the economy that triggered such a reaction:

2000 - Dot Com Bubble Bust

2007 - Subprime Crisis/GFC2020 - COVID-19 Pandemic

2022 - Rapid Fed tightening due to inflation led to the highest nominal rate since the 2000s and the Russia-Ukraine War

Is there any such material issue in the economy today? I don’t think so. Most institutional forecasts predict an impact of ~0.5% on inflation, and Morningstarr predicted a commutative impact of ~0.3% through 2028 on the GDP if all proposed tariffs go in. This is nowhere close to the four bear market cause I listed above.

In addition, below are the positive catalysts for the markets:Inflation Improving:

This week, CPI came better than expected. I mentioned multiple times in this newsletter that the inflation will only come down from here. Check curated insights from the Sept. 22, 2024 letter for the details. CPI is generally higher than the PCE, the Fed's preferred inflation measure. As CPI came better than expected, PCE later this month is also expected to improve.Govt. Shutdown Averted:

President Trump signed the funding bill, which avoided the government shutdown till Sept. Thanks to this, there will be less negative news for the market in the near future.Nvidia GTC 2025:

GTC, Nvidia’s biggest conference of the year, begins Monday and runs till Friday in San Jose. This may resurrect the AI buzz and be a positive for Nvidia stock. If the Nvidia stock gets support or improves, that’s good for the overall market.Crew-10 Mission:

One of the main reasons for the recent market drop is the negative sentiment around Tesla and Elon Musk. As Tesla is a significant component of all major indices, its strength matters. One thing that can turn the negative sentiments around Mr. Musk is the Crew-10 mission from SpaceX, which is expected to bring home some of the stranded astronauts from space. This is also happening next week. I know, a lot for a week 😃FOMC Meeting:

The Fed chair Powell mentioned a week ago that he is not worried about the economy and tariff chaos. ReadI don’t expect him to change his opinion significantly (especially with mixed macro data since he last spoke) in a week, and you can expect what he will say at the FOMC press conference. If he re-iterates the same comments in the FOMC press conference, it will magnify the markets more.

The CME Fed Watch shows almost no probability of a rate cut (unless the Fed surprises to stay ahead of the curve). There is some room for lower rates, i.e., the Fed Put is somewhat in place, which can support further downsides.Possible Ceasefire:

Russia came to the table last week and is ready to discuss a ceasefire with Ukraine. If something works out in the near future, which is a strong possibility considering the push from President Trump, it’s another positive catalyst for the market with one less Geopolitical thing to worry about.Earnings Revision:

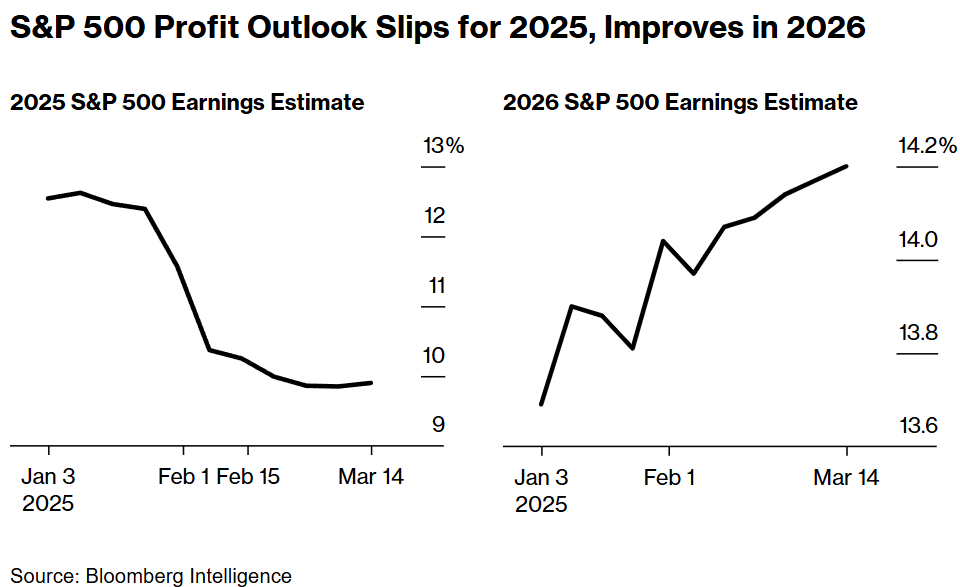

Below are the earning revisions this year. US analytics still predict ~% earnings growth for the S&P 500 ( drop from ~12% earlier). Does that sound like a recession? Absolutely not. Also, it is very important to note that we already established that the US analysts are accurate with their predictions, and it was one of the top three charts from the Yahoo Chartbook I highlighted recently in this newsletter (check here).

Useless Institutional Forecast:

As always, many institutions rushed to change their S&P year-end end targets. So what’s the use of the year-end targets if they need to be changed within 3 months? GS lowered its forecast from 6500 to 6200, as did Yardeni Research and others. I previously mentioned how poor some of these forecasts are or they are outright wrong in one case (here)

Despite all this, markets can continue to fall in the short term, but in the medium to long term, it comes back to the fundamentals. The ~10% earnings growth for 2025 and all the other fundamentals I listed indicate that most of the pain should be behind us. In addition, the 2026 earnings forecasts are 14+%, and markets try to factor in future good news in advance, which can happen closer to the end of the year.

For the week:

The S&P 500 is down 2.27%, the Nasdaq is down 2.43%, and the Dow 30 is down 3.07%.

CNN's Fear & Greed Index now stands at 21 (Extreme Fear) out of 100, up by 1 point from last week. Details here

The top five trending stocks on Reddit are SPY, Tesla, Nvidia, enCore Energy, and Micro Strategy. Read More

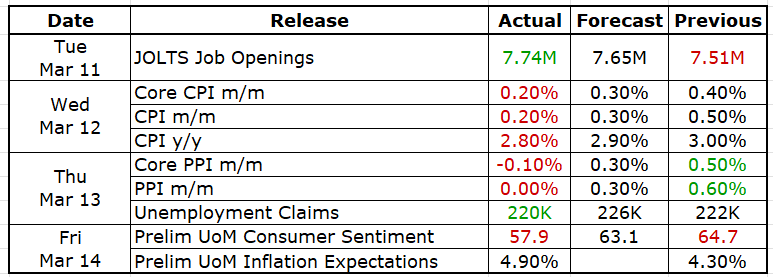

Here is a summary of this week’s key economic releases:

In addition to the CPI, UoM Consumer Sentiment was another key macro data. Lower than expected reading spooked the market. However, I don’t consider this as important as the one-year inflation forecast if 4.9% from this survey doesn’t make sense. This clearly contrasts with institutional inflation forecasts based on analysis of actual trade data.

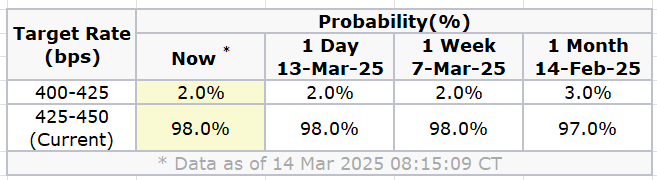

Target Rate Probabilities for Mar 19th FOMC Meeting:

CME FedWatch

CURATED INSIGHTS & ANALYSIS:

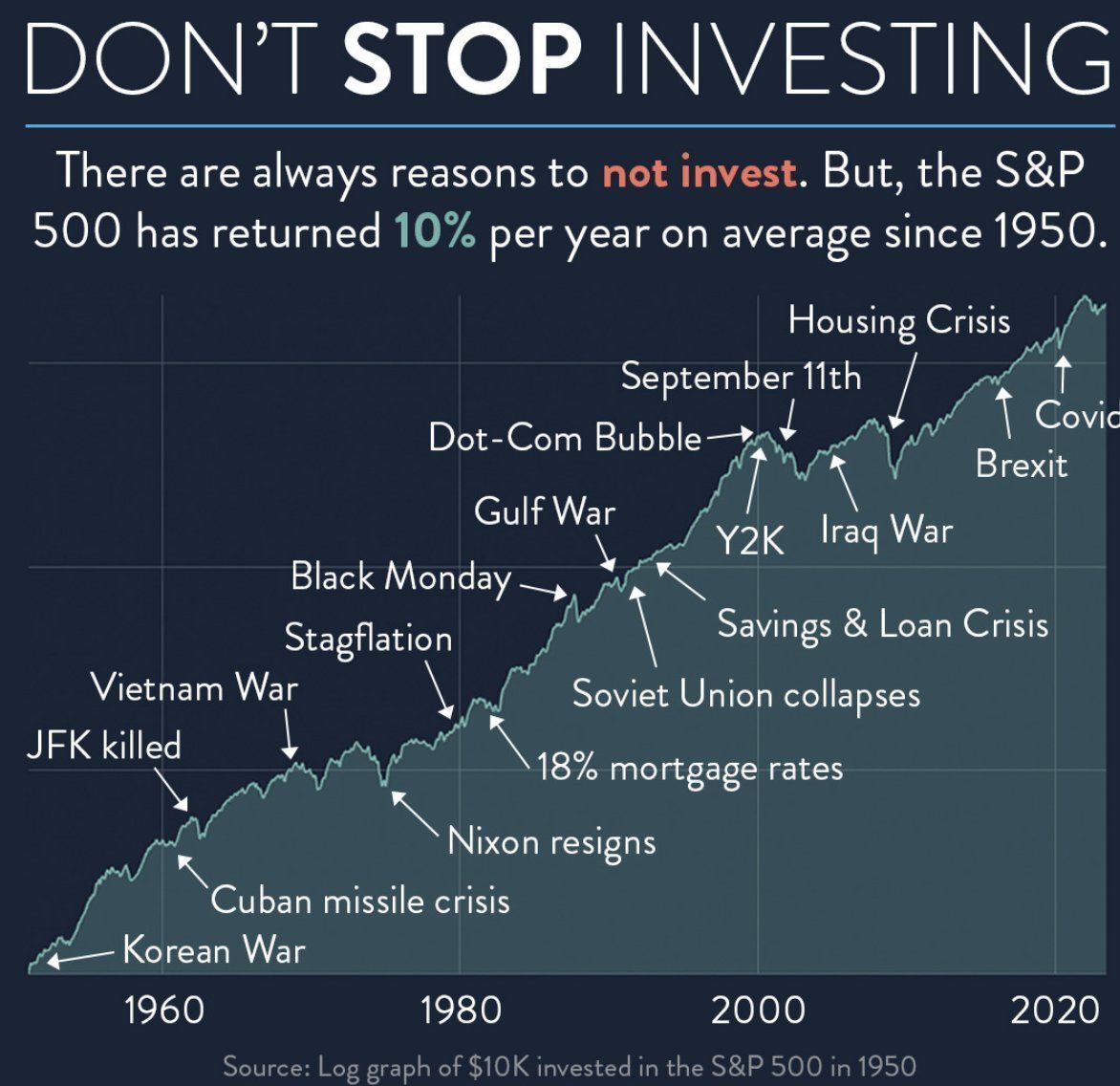

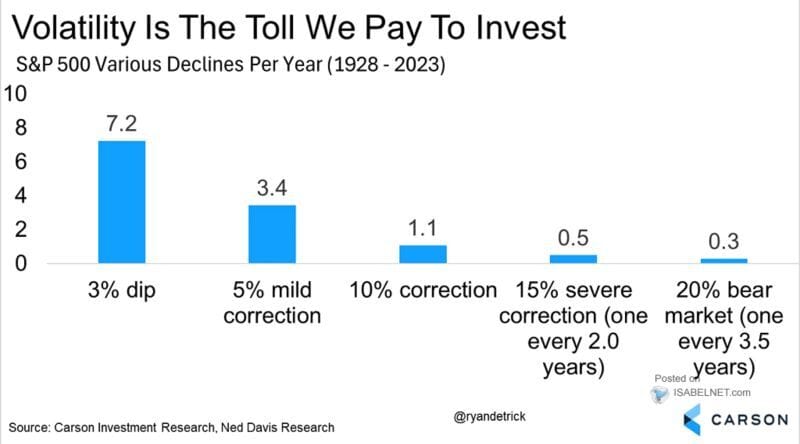

Volatility Is The Toll We Pay For Investing:

Considering the recent market volatility, I thought of sharing the two visuals below, perfect for understanding that stocks will always have these drawdowns. Long-term stocks have the best chance to beat inflation than any other asset class:

FRONT PAGES:

Supplemental Leverage Ratio: Five House Republicans pressed Fed Chair Jerome Powell to enhance Treasury market liquidity, suggesting “targeted” adjustments to bank capital requirements. The $29 trillion Treasury market has faced liquidity strains, notably in early 2020 when the COVID-19 panic nearly halted trading, forcing the Fed to intervene with massive Treasury purchases. Read

Gold Surge: Gold surged past $3,000 an ounce for the first time, fueled by aggressive central bank purchases and global economic instability. Read

OpenAI vs. DeepSeek: OpenAI has proposed to the Office of Science and Technology Policy that the U.S. government ban DeepSeek in government, military, and intelligence sectors. Citing the Chinese AI by name, the proposal labels DeepSeek as "state-subsidized" and "state-controlled." Read

Falling Eggflation: Egg prices dropped sharply in March as supply constraints eased, offering consumers relief on a key grocery staple. The result: The average cost of a dozen large white eggs is now $4.90, compared with an all-time high of $8.64 on March 5, the United States Department of Agriculture said. Read

Shutdown Averted: President Trump signed the Republican-led spending bill to prevent a government shutdown, the White House announced Saturday. Read

Consumer Sentiment Fall: The University of Michigan's March Consumer Sentiment Index fell to 57.9, down 10.5% from February and missing the Dow Jones estimate of 63.2. Read

EARNINGS UPDATE:

Oracle Miss: Oracle’s fiscal Q3 results fell short of analyst expectations. However, its cloud infrastructure segment continues to surge, driven by strong demand for AI-capable computing power. Read

Adobe Beat: Adobe exceeded Wall Street’s expectations and reaffirmed its guidance. However, concerns persist that it is losing ground to competitors and falling behind in AI innovation. Read

EARNINGS PREVIEW:

Date | Symbol | Name | Time |

20-Mar | PDD | Pdd Holdings Inc | Before Open |

20-Mar | MU | Micron Technology | After Close |

20-Mar | NKE | Nike Inc | After Close |

20-Mar | FDX | Fedex Corp | After Close |

20-Mar | ACN | Accenture Plc | Before Open |

VIDEO’s OF THE WEEK:

Please Share This Newsletter With Your Friends.

Also, check my blog here.

This newsletter's content is for informational and educational purposes only and should not be considered trading or investment recommendations. All the opinions in this newsletter are personal and do not belong to any organization.