Weekly Newsletter

Santa Clause Rally Struggles

Banks Sues The Fed

Open AI Announces Restructuring Plan

IRS Special Reimbursement Plans

QUOTE OF THE WEEK:

“It’s not lost on me that we are facing scrutiny across the world,” It comes with our size and success. It’s part of a broader trend where tech is now impacting society at scale. So, more than ever, through this moment, we have to make sure we don’t get distracted.” Sundar Pichai, CEO - Google

KEY US ECONOMIC EVENTS NEXT WEEK:

MARKET CLOSE:

CNBC: EOD 27th Dec

Good Afternoon. Last week, I wrote about why I think we will have a positive holiday week for the market. The market sold off on Friday but still managed to close to positive for all indices. I was hoping that this would help S&P close positive for the month, but that did not happen due to Friday’s ~1% sell-off. Still, there are a couple more days left in this month, and the odds favor gains to push the month into positive territory for the S&P 500.

Next week is also fairly quiet. Manufacturing PMI data, expected next Friday, will show if manufacturing remains a weak sector.For the week:

The S&P 500 is up 0.70%, the Nasdaq is up 0.80%, and the Dow 30 is up 0.40%.

CNN's Fear & Greed Index now stands at 34 (Fear) out of 100, down 19 points from last week. Details here

The top five trending stocks on Reddit are SPY, Tesla, AMD, KULR Technology, and Comstock Mining . Read More

Here is a summary of this week’s key economic releases:

Target Rate Probabilities for Jan 29th FOMC Meeting:

CME FedWatch: Data as of 27 Dec 2024 10:08:11 CT

FRONT PAGES:

Banks Sue The Federal Reserve: Banks and business groups have filed a lawsuit against the Federal Reserve, challenging the legality of its annual stress tests. Led by the Bank Policy Institute and supported by organizations like the U.S. Chamber of Commerce, the suit seeks to address "longstanding legal violations" by demanding public input in the stress test process, as mandated by federal law. While not opposing stress testing, the groups argue that the current approach lacks transparency and imposes inconsistent capital requirements. Read

Honda and Nissan Explore Merger: Japanese automakers Nissan and Honda have initiated formal talks to merge, aiming to become the world’s third-largest automaker by sales. If successful, the merger could generate annual revenue of 30 trillion yen ($191.4 billion) and operating profit exceeding 3 trillion yen, according to Honda CEO Toshihiro Mibe. The discussions are expected to conclude by June 2025, with Nissan's partner, Mitsubishi, deciding on its participation by January 2025. Read

Saks Neiman Marcus Merger Complete: Saks Global finalized its $2.7 billion acquisition of Neiman Marcus Group, as announced on Monday. This strategic move consolidates several high-end retail brands under the Saks Global umbrella, including Saks Fifth Avenue, Saks Off Fifth, Neiman Marcus, and Bergdorf Goodman. Read

IRS Refunds: The IRS is set to deposit $2.4 billion in pandemic-era stimulus payments directly into the bank accounts of 1 million taxpayers as a "special" year-end disbursement. Read

Open AI’s Restructuring Plan: OpenAI announced plans on Friday to restructure its corporate governance, transitioning away from nonprofit control. Read

EARNINGS UPDATE:

No significant earnings were reported this week. I covered a detailed analysis of this earnings season on Dec 15th, when more than 99% of S&P 500 companies had reported earnings.

EARNINGS PREVIEW:

Date | Symbol | Name | Time |

1/8/2025 | JEF | Jefferies Financial Group Inc | After Close |

1/7/2025 | RPM | RPM International Inc | Before Open |

12/30/2024 | BHP | Bhp Billiton Ltd ADR | -- |

1/8/2025 | ACI | Albertsons Companies Inc Cl A | Before Open |

CURATED INSIGHTS:

Important Facts: As Of the Last Weekend of 2024:

The US Economy is the most resilient among the developed markets. The US outperformance is mainly driven by productivity growth.

10-Year Treasury Yield Rose 100 Basis Points Since September As The Fed Cut 100 Basis Points. This historic divergence is due to increased term premiums. I discussed this in detail in a few posts earlier, but in short, the Fed is cutting rates in a growing economy. There is also a fear that the new administration may drive inflation high with its policies around tariffs. The combination of these factors led to a rise in US Treasury yields.

The mortgage rates closed at 6.85%, just around where they started the year. The treasury yields are the mortgage rates are co-related as the MBS trades at a premium to the US treasuries. Please check the Oct 27th post for the details.

The S&P 500 is concentrated on tech stocks.

Source: The Compound

This concentration is justified. I don’t see any material reasons why this dominance will be affected in 2025. The tech stocks are richly valued but not overvalued.

Source: Syz Private Banking

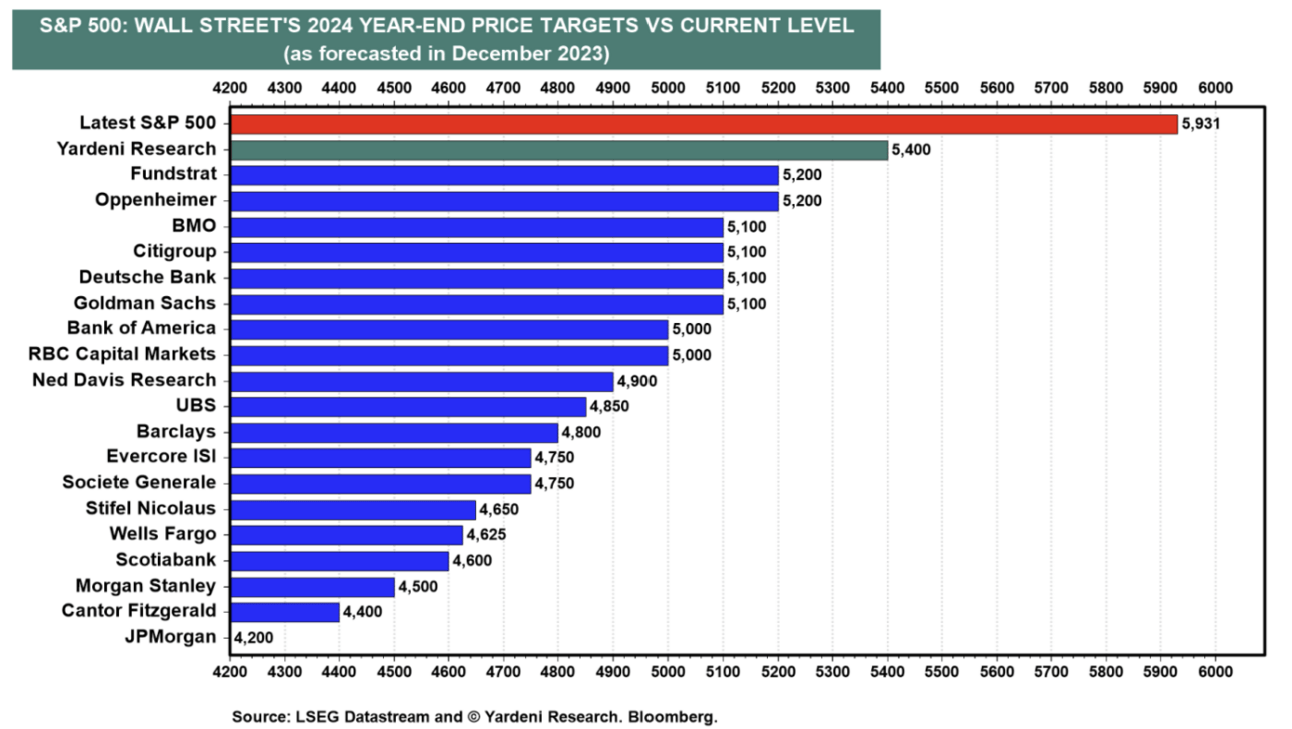

The most important. Wall Street firms will have many index predictions for the end of 2025. You can safely ignore them. No one can predict the future. Companies can't predict their earnings for more than two quarters, so I'm not sure how these firms come up with these predictions, which is beyond me. Their performance is pathetic, and I covered one such case about GS predictions in detail in this newsletter:

DEO’s OF THE WEEK:

Private Market Access for Accredited Investors

All investments have the risk of loss. UpMarket is not associated with or endorsed by the above-listed companies. Only available to eligible accredited investors. View important disclosures at www.upmarket.co

UpMarket brings accredited investors closer to the potential tech giants of tomorrow. Trusted by over 500 investors, our platform has facilitated over $175M in investments in private companies like OpenAI, ByteDance, and SpaceX. UpMarket simplifies access to exclusive deals that could help you redefine your investment portfolio. Embrace the future of investing with UpMarket and gain a foothold in nascent industries and sectors that are changing the world.

Please Share This Newsletter With Your Friends.

Also, check my blog here.

This newsletter's content is for informational and educational purposes only and should not be considered trading or investment recommendations. All the opinions in this newsletter are personal and do not belong to any organization.